A trust is a helpful estate planning tool that works alongside your last will and testament to manage your assets. Beyond mere asset distribution, a trust offers flexibility, discretion, and potentially favorable tax implications.

This guide aims to shed light on the importance of trusts, the setup process, associated costs, and the measures to undertake once established. Equip yourself with the knowledge to make informed decisions for your financial legacy.

Why Set up a Trust?

A trust is a legal arrangement created by the grantor that allows a third party, known as the trustee, to hold and manage assets on behalf of a beneficiary. The types of assets that can be placed in a trust range extensively from money and stocks to real estate properties.

Anyone who wants to ensure their assets are well-managed and distributed according to their wishes can benefit from setting up a trust. More specifically, benefits of a trust can include:

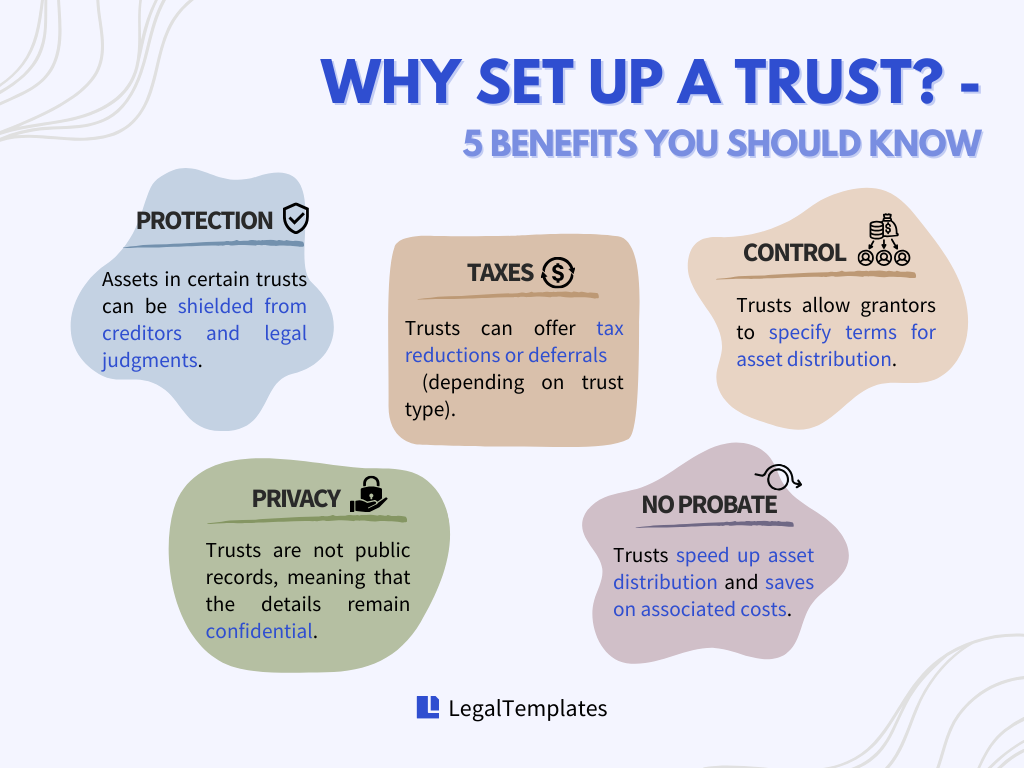

- Avoiding Probate: Speeds up asset distribution and saves on associated costs.

- Privacy: Trusts are not public records, ensuring the details remain confidential.

- Tax Advantages: Depending on its type, a trust can offer tax reductions or deferrals.

- Control: Allows grantors to specify terms for asset distribution.

- Protection: Assets in certain trusts can be shielded from creditors and legal judgments.

How to Set up a Trust: 5 Steps

Setting up a trust is fairly straightforward, but carrying out the steps will take some time. You should also plan to review your assets and create a plan for how you want your assets distributed.

Note

The steps in this article to setting up a living trust. Other types of trusts may have different requirements for establishment.

Step 1: Determine Purpose

The purpose of your trust sets the foundation for everything that follows. To ensure that your trust aligns with your objectives and values, begin by asking yourself these three pivotal questions:

What purpose(s) do you want the trust to serve?

A trust can serve many purposes, and identifying its primary goal is crucial. Some commonly seen purposes include:

- Estate Tax Reduction: Minimizing potential estate taxes upon passing.

- Asset Protection: Shielding assets from potential creditors or legal judgments.

- Charitable Giving: Allocating funds or assets to support philanthropic causes.

- Special Needs Care: Providing for a family member with unique care requirements without jeopardizing government benefits.

- Education: Setting aside funds specifically for the educational expenses of beneficiaries.

- Succession Planning: Ensuring continuity and smooth transition of business or property ownership.

What asset(s) do you want to put in the trust?

When deciding what assets to include, think about whether it will otherwise go through probate.

In addition, consider including instructions for how assets will be distributed when the time comes. For example, you could set up your trust so that your child receives funds from your trust after they reach a certain age or receives monthly payments of a certain amount rather than a lump sum.

Common trust assets include:

- Cash and bank accounts;

- Certificates of deposit;

- Business interests;

- Real estate;

- Personal property;

- Investments, stocks, and bonds;

- Life insurance policies;

- Intellectual property.

Some assets, such as your retirement funds, can’t be placed in a trust. Other assets, like healthcare savings plans, already bypass probate and don’t need to be included in a trust.

If you need guidance on which assets to transfer to your trust, be sure to seek legal advice.

Should I put my car into a trust?

Everyday vehicles may not be an ideal trust asset due to potential retitling taxes. They either bypass probate or are transferred directily by designating transfer-on-death beneficiaries. However, a high-value collectible car might benefit from being placed in a trust. Always check your state’s regulations regarding vehicle transfers after death.

When do you want the trust to take effect?

Depending on the type of trust you set up, a trust can take effect:

- Immediately: Often seen with living or revocable trusts, which are active during the grantor’s lifetime.

- Upon Your Death: Typical for testamentary trusts that are set up after death as part of a last will and testament.

- At a Specific Event or Milestone: For example, when a beneficiary reaches a certain age or graduates from college.

- Under Certain Conditions: Such as the onset of a disability or the birth of a child.

These choices can determine how fluid or rigid your trust is, ensuring it aligns with your broader estate and life goals.

After you have clear answers to the three questions above, you should have no problem picking the type of trust that satisfies your exact needs.

Step 2: Identify Trustees and Beneficiaries

Once you’ve determined the purpose of your trust, the next step involves selecting the key players — trustees and beneficiaries. These decisions are vital as they determine who manages the assets and who benefits from them.

Choosing a Trustee

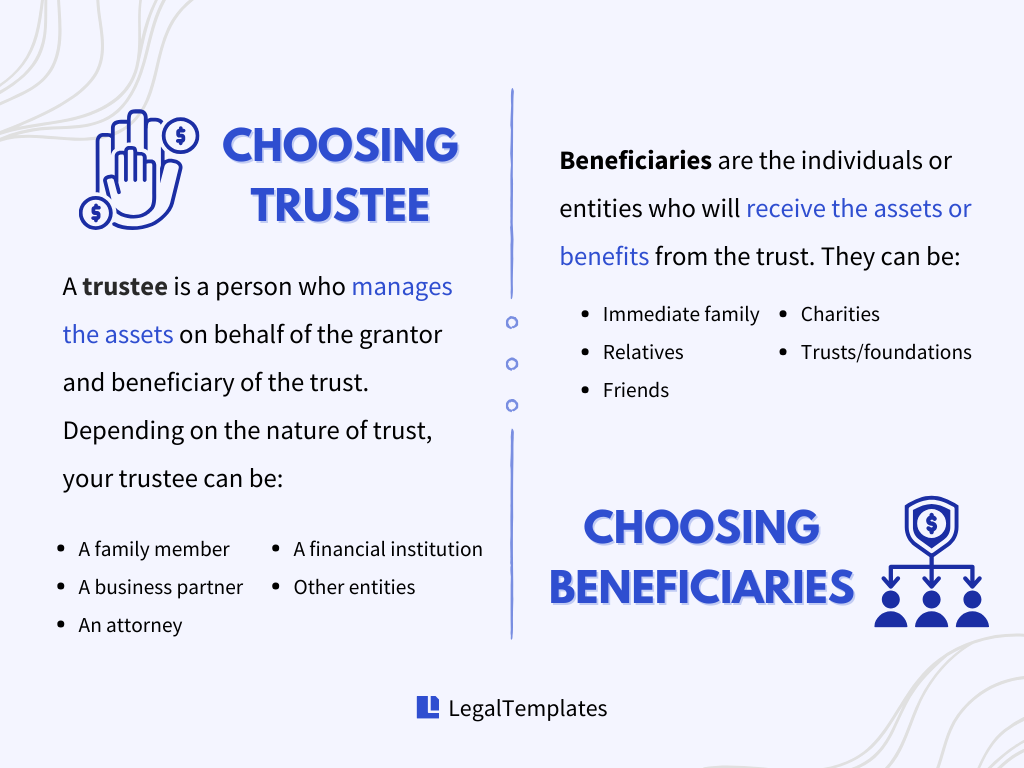

A trustee is a person who manages the assets and trust funds on behalf of the grantor and beneficiary of the trust.

For a living trust, it’s commonplace for grantors to appoint themselves as the trustee, thereby retaining complete control over the trust assets. However, it’s perfectly acceptable to appoint another individual as a trustee or even co-trustee to administer the trust alongside you.

Whoever you choose as a trustee, they are bound by a fiduciary duty, which mandates them to act in your best interest and strictly follow your stipulated wishes.

In addition to selecting a primary trustee, it’s a good idea to designate a successor trustee. The successor trustee steps into the role if the primary trustee passes, resigns, or is unable to serve.

When choosing a trustee or successor trustee, various candidates could fit the bill:

- Dependable Family Member: Someone familiar with the family dynamics and invested in upholding your wishes.

- Business Partner: Especially relevant if the trust involves business assets or interests.

- Attorney: Their legal expertise can be beneficial for more complex trusts.

- Financial Institution: They bring a wealth of experience and can act impartially, free from potential emotional attachments.

- Other Entities: Depending on the trust’s nature, other professional organizations or entities might be apt.

Keep in mind that some third-party trustees may be eligible to receive trustee fees (compensation for managing your trust). The exact amount you should pay your trustee varies depending on the trust’s complexity and the trustee’s tasks, but the compensation is typically paid from the trust assets.

While family members or friends often serve without compensation for simpler trusts, professional trustees typically charge between 1% to 2% of the trust’s assets annually or the estate value. On the other hand, non-professional trustees might charge around 0.5% to 1% or even hourly rates.

State law typically requires trustee compensation to be “reasonable,” but check your local area for the most accurate information.

Choosing Beneficiaries

The beneficiaries are the individuals or entities who will receive the assets or benefits from the trust. When selecting beneficiaries, consider:

- Immediate Family: Spouses, children, or grandchildren often top the list.

- Extended Relatives: Nieces, nephews, or even distant relatives.

- Friends: Especially if they have played a significant role in your life.

- Charitable Organizations: If philanthropy is a goal of your trust.

- Trusts or Foundations: You can name another trust or foundation as a beneficiary for strategic purposes.

Always ensure your choices align with your broader estate planning goals and reflect your desires.

Step 3: Create Your Trust Document

The trust document serves as the backbone of your trust, laying out its structure and governing its operation.

Although trust laws vary from one state to another, here are the general key provisions of a trust:

- Grantor’s Details: This should include your full name and other relevant information, establishing you as the person creating and setting up the trust.

- Assets and Property of the Trust: Incorporate the assets you decided on earlier, such as your home, business, and any other significant assets. These should be explicitly listed in the trust document to ensure clarity.

- Beneficiaries’ Details: Include all beneficiaries’ names and pertinent information to ensure there’s no ambiguity regarding who stands to benefit from the trust.

- Distribution Mechanism: Specify what, when, and how the beneficiaries will receive the assets. This could be certain assets or a percentage of the trust, upon reaching a certain age, achieving a particular milestone, or any other conditions you deem fit.

- Trustee’s Details: Clearly state the name and information of the initial trustee, the person or entity responsible for managing the trust. This individual or organization will ensure the trust operates according to your wishes.

- Successor Trustee’s Details: Just as crucial as the initial trustee’s details.

Once you have all these provisions laid out in your trust document, notarize your trust. Not all jurisdictions require notarization, but acknowledging the trust document before a notary public adds a layer of authenticity, credibility, and protection against potential disputes or challenges in the future.

Familiarize yourself with your state’s specific trust laws while you draft the document. Consult with an estate planning attorney if necessary.

Step 4: Comply with IRS

Depending on the type of trust, the trust may need an Employer Identification Number (EIN), a number assigned by the IRS to identify an entity for tax-related purposes.

The grantor’s Social Security Number (SSN) can typically be used for tax purposes for revocable living trusts where the grantor is the trustee. However, in cases where the trust is irrevocable or the grantor is not the trustee, or if the grantor passes away, an EIN becomes essential.

There are three common ways to obtain an EIN for your trust:

- Online: The IRS’s official website offers an online EIN application process, which is straightforward and provides the EIN immediately upon completion.

- By Mail: Alternatively, you can download Form SS-4 from the IRS website, complete it, and mail it to the appropriate address for your state.

- By Fax: Complete Form SS-4 and fax it to the designated number for your state. The EIN is typically sent back within a few days.

Once your trust has its EIN, it’s imperative to file any necessary tax returns and maintain compliance with all tax obligations. Doing so ensures the trust remains in good standing and avoids potential legal or financial complications.

Step 5: Transfer Assets into Trust

You can now start transferring your assets into the trust. Doing so ensures that the trust holds legal ownership of these assets, which is essential for it to function as intended. The process varies depending on the type of asset you’re transferring.

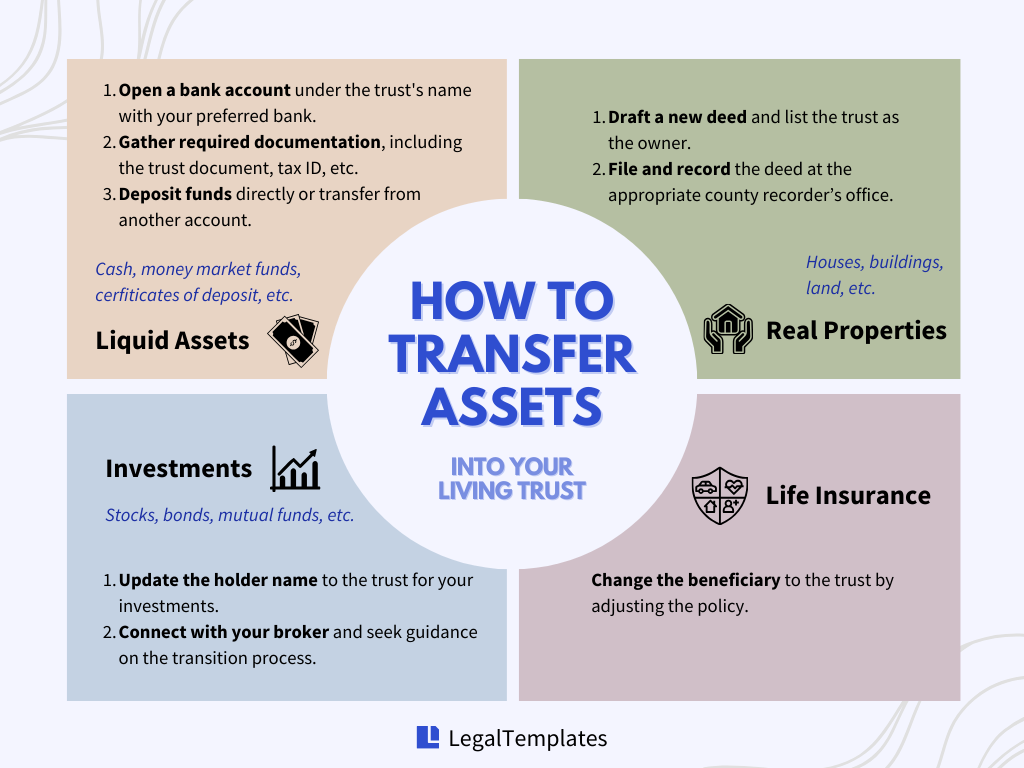

For Liquid Assets

- Open a Trust Bank Account: Approach your chosen bank with the necessary trust details. Establish an account under the trust’s name.

- Required Documentation: Equip yourself with all the details from Step 3, along with a tax ID you acquired from Step 4. Your bank will guide you regarding any additional requirements and the process of collecting signatures from the concerned parties.

- Direct Deposit or Transfer: To fund the trust’s bank account, either deposit money directly or execute a transfer from another account into the trust’s bank account.

For Real Properties

- Change Property Owner Name: Create a new deed reflecting the trust’s name as the property owner.

- File and Record the Deed: Typically, this is done at the county recorder’s office where the property is located.

For Investments (Stocks, Bonds, etc.)

Modify the registration of stocks, bonds, or other similar investments to indicate the trust as the holder. Depending on your broker or investment firm, this might be an online process or necessitate an in-person visit.

For Life Insurance

Adjust your life insurance policy to pay out to your trust upon the triggering event.

How Much Does a Trust Cost?

Setting up a trust through an estate planning attorney typically costs at least $1,500-$2,500, depending on the complexity of your estate. Larger estates, more beneficiaries, and complex business arrangements will drive up the cost even more.

Alternatively, you can create a trust yourself for much less if you’re willing to put in the extra time. If you decide to set up a trust yourself, you should plan to spend at least $150 as any trust will have setup costs, filing fees, fees for name and title changes, as well as ongoing administrative costs.

After Setting up Your Trust

Once you’ve created your trust, the work doesn’t end there. Here’s what to keep in mind after your trust is established:

- Continuous Management: This includes anything from paying property taxes for real estate to reinvesting stock dividends.

- Periodic Review: Life changes, such as births, deaths, marriages, or even changes in your financial status, might necessitate adjustments to the trust.

- Tax Implications: Familiarize yourself with any tax filings the trust might require and stay updated on changing tax laws that could affect it.

- Communication: Make sure that beneficiaries and successor trustees are aware of the trust, its terms, and any responsibilities they might have in the future.

- Professional Consultation: Don’t hesitate to consult with a financial advisor, lawyer, or tax professional if you have questions or concerns about your trust.

- Trustee Compensation: If you’ve appointed an external trustee, ensure they’re compensated appropriately for their work. Remember that trustee fees can have tax implications.

- Document Storage: Store all trust-related documents safely and ensure that key stakeholders, such as successor trustees, know where to find them.

Trusts — especially living trusts — require regular attention and management to ensure your current needs and wishes are properly addressed.

Conclusion

Trusts are a key element in a comprehensive estate plan, allowing you to manage and distribute assets according to your wishes. While the process might seem daunting, with careful planning and regular oversight, a trust can be an invaluable tool in securing your legacy and providing peace of mind for you and your beneficiaries.

Join over 500,000 users and create your estate plan with us now.

Frequently Asked Questions

How much does a trust cost to maintain?

The cost of maintaining a trust can vary widely depending on its complexity, the assets involved, and the fees of the professionals employed to manage it. Here’s a breakdown of some of the common maintenance costs:

- Trustee fees (ranges from 0.5% to 2% of the trust’s assets per year);

- Investment management fees (if the trust assets are invested);

- Accounting fees (varies depending on the complexity of the trust’s finances);

- Taxes (can cost several hundred dollars).

Remember, the actual costs will depend on many factors, including the complexity of the trust, the types of assets it holds, and the professionals you choose to work with.

How does a trust work after someone dies?

After someone dies, the trust operates as per the instructions laid out in its documents. The trustee steps in to manage and distribute the assets to the beneficiaries as specified.

The process is typically more streamlined and private compared to the probate process that a will goes through, thus ensuring a quicker and smoother transition of assets to the beneficiaries.