The distinctions between loan agreements and promissory notes can be subtle but significant.

In this article, we help you choose the correct loan document for your lending situation by clearly guiding their appropriate usage and addressing commonly held misconceptions.

Promissory Note vs. Loan Agreement

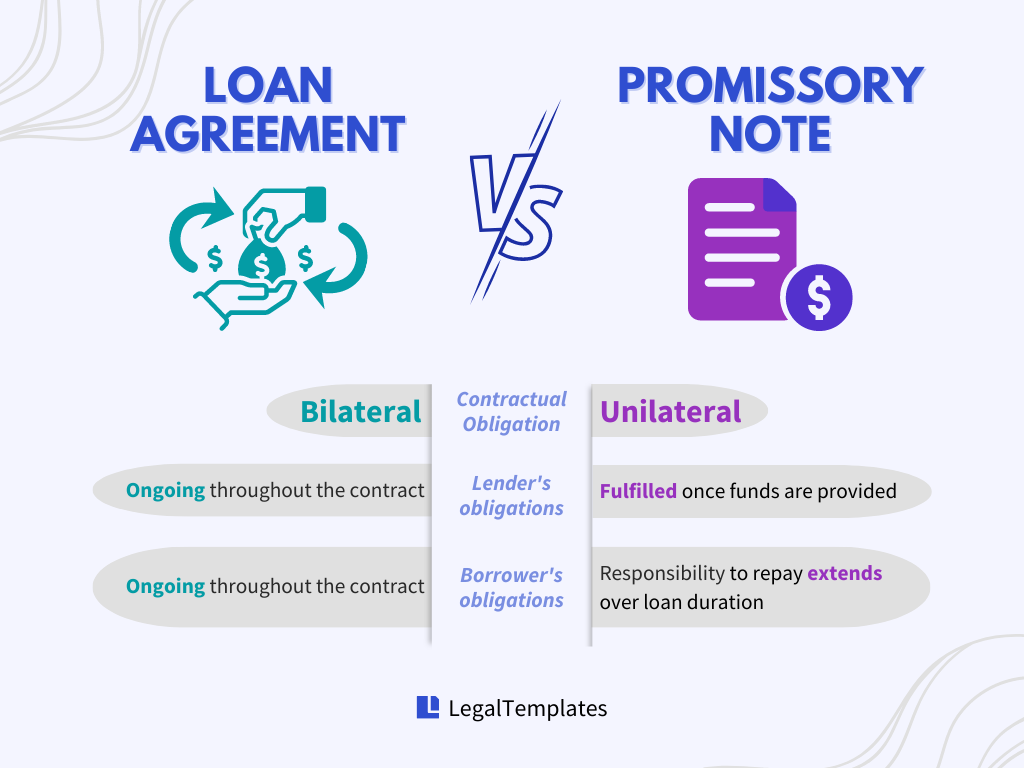

A promissory note is a unilateral contract. The lender fulfills their obligation when they provide the funds to the borrower, while the borrower’s responsibility to repay the loan is extended throughout the repayment period.

On the other hand, a loan agreement is a bilateral contract, meaning that obligations are concurrent and mutual throughout the contract, and both parties have ongoing responsibilities.

The lender must provide the loan, and the borrower must repay it, often with interest.

In short, both promissory notes and loan agreements are legally enforceable documents that contain the specifics of a loan’s terms and conditions.

However, the borrower has an ongoing responsibility to fulfill in a promissory note, while both parties share obligations in a loan agreement.

Now that you understand the essential distinction let’s take a look at how this distinction significantly influences how and when these loan documents are used in lending scenarios.

4 Key Differences

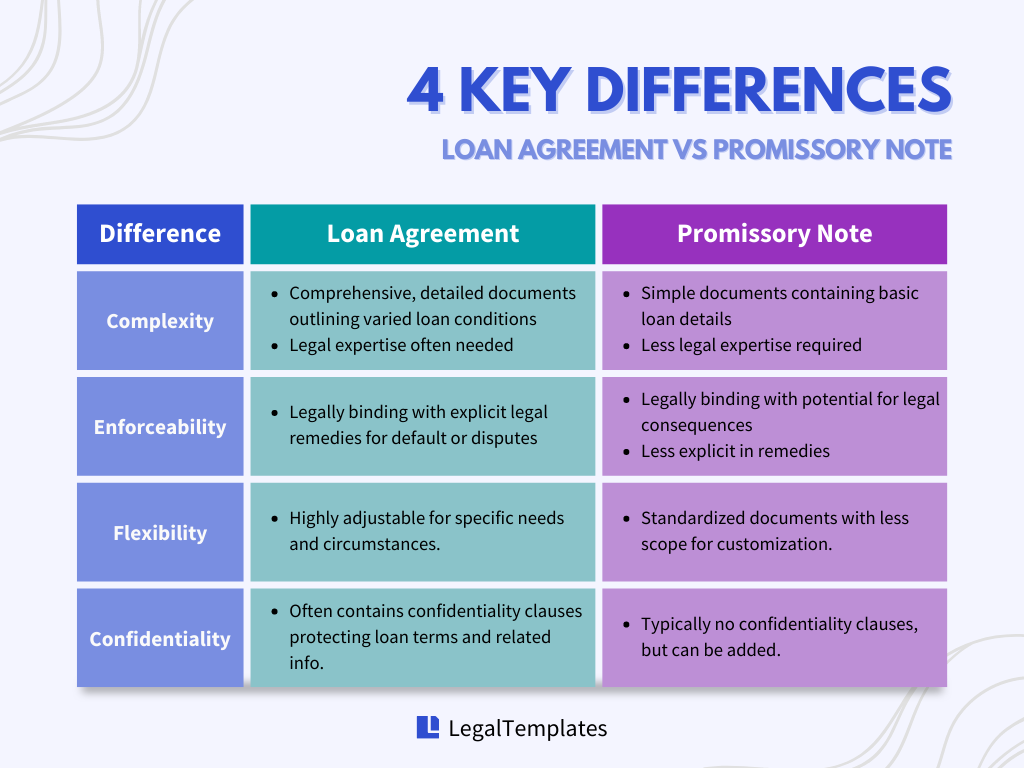

1. Complexity

Promissory notes, like many unilateral contracts, are usually more straightforward documents. They contain fundamental details like the loan amount, interest rate, repayment schedule, and maturity date.

While variations or additional agreed-upon terms may exist, the format is relatively standardized. Its simplicity makes it easy for individuals to use without requiring extensive legal expertise.

In contrast, loan agreements are more comprehensive and detailed documents. They outline not just the loan amount and repayment terms but also specify various conditions, such as representations and warranties, restrictive covenants, and events of default.

Because of this complexity, drafting a loan agreement often requires legal expertise to cover all potential scenarios and protect parties’ rights.

2. Enforceability

Both promissory notes and loan agreements are legally binding documents, and failing to adhere to their terms can lead to legal consequences for the borrower.

However, with its detailed provisions, the loan agreement may offer the lender more explicit legal remedies in case of default or disputes.

For instance, the loan agreement might specify a process for handling late payments or defaults, including timelines for issuing default notices, rights to accelerate the loan, and actions to enforce security.

While a promissory note can also provide for these, the detail level and specificity are usually more significant in a loan agreement.

3. Flexibility

Loan agreements can be tailored to cater to the specific needs and circumstances of the parties involved. They can be custom-built to fit various lending situations, such as syndicated loans, revolving credit facilities, or term loans.

The terms can be adjusted to account for the borrower’s financial condition, market conditions, or regulatory environment.

Promissory notes, while flexible in their own right, are generally more standardized. They typically specify the loan amount, interest rates, and repayment schedule, with less flexibility to accommodate unique or complex lending scenarios.

4. Confidentiality

Loan agreements sometimes contain confidentiality clauses, which bind the parties to keep the loan terms and any related information confidential.

This can be crucial in commercial lending situations, where disclosing the loan’s details might impact the borrower’s business operations or the lender’s competitive position.

Promissory notes, on the other hand, typically do not include such clauses. However, confidentiality provisions can be added to a promissory note depending on the situation and the parties involved.

Common Misconceptions

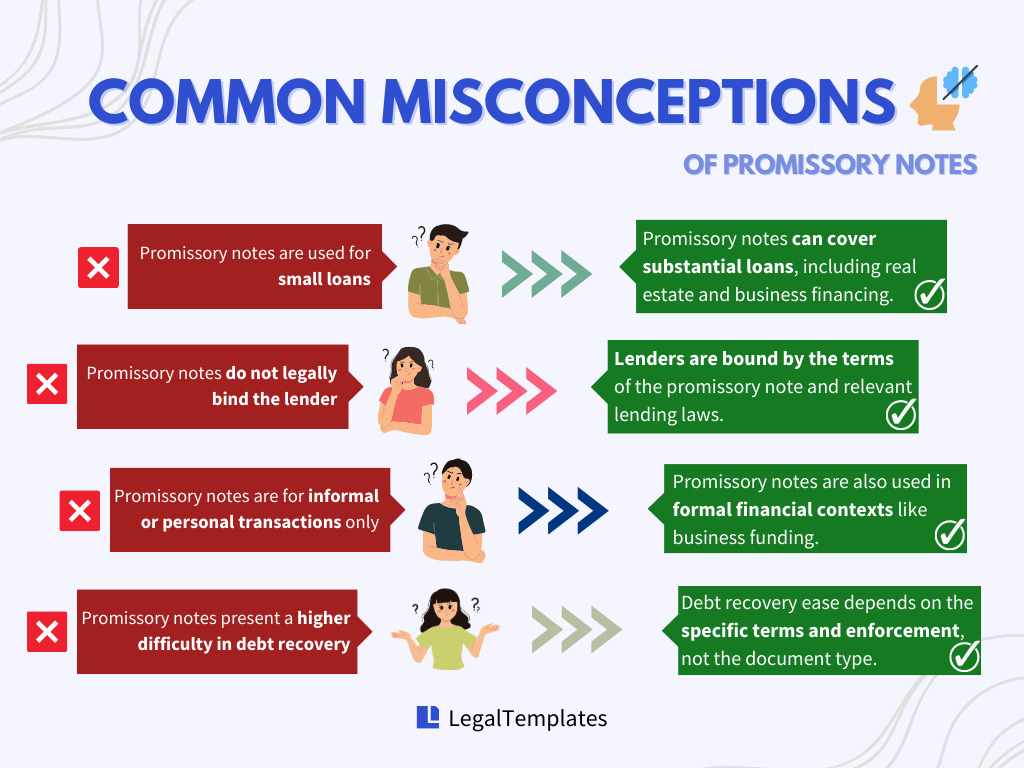

MISCONCEPTION: Promissory notes are used for small loans

In reality, promissory notes are used in various scenarios, and the amount of money they cover can be substantial.

For example, they’re widely employed in real estate, where transactions often involve significant sums of money. They’re also a standard tool in business financing, often facilitating large-scale investments in financial institutions.

Furthermore, federal student loans in the United States are usually accompanied by a promissory note – again, these loans can be substantial, potentially reaching tens of thousands of dollars.

To summarize, a promissory note’s simplicity and unilateral obligation make it versatile for various lending situations, irrespective of the loan size.

MISCONCEPTION: Promissory notes do not legally bind the lender

Just because promissory notes are unilateral contracts doesn’t mean the lender lacks legal obligations or accountability.

From the onset, the lender must provide the loan to the borrower, which forms the very foundation of the promissory note. Should the lender fail to fulfill this obligation, the borrower may have legal recourse against them.

Moreover, the lender is legally bound to adhere to the terms stipulated in the promissory note. For instance, they can’t unreasonably accelerate the loan repayment or change the interest rate midway unless the document explicitly outlines such provisions.

Lenders are also bound by federal and state laws that regulate lending practices. These laws cover fair lending, usury laws (which prevent charging exorbitant interest rates), and debt collection practices.

In conclusion, while the obligations of a lender in a promissory note differ from those in a bilateral contract like a loan agreement, it’s a misconception to say that they’re not legally bound.

MISCONCEPTION: Promissory notes are used on informal occasions or between acquaintances only

As previously stated, promissory notes are versatile instruments and can be found in more formal financial contexts.

In business, startups or smaller companies may use promissory notes to secure short-term funding. They offer a simpler alternative to more complex business loan agreements. Additionally, they are the foundation of many complex securities and financial instruments like mortgage-backed securities.

Therefore, while promissory notes can be used for informal lending between known individuals, they are not restricted to such situations. They are equally prevalent in formal financial contexts, reflecting flexibility and utility.

MISCONCEPTION: Promissory notes present a greater difficulty in debt recovery

The ease of debt recovery largely depends on the precise terms within the document and how well they are enforced, not the instrument itself.

Legally, a promissory note is an enforceable obligation, just like a loan agreement. If a borrower defaults, the lender can take legal action to recover the loan amount, including pursuing a court judgment or attaching a lien to the borrower’s property, depending on the jurisdiction and the terms of the note.

If the note is “secured” — linked to a specific asset as collateral — recovery may be even more straightforward as the lender has the right to claim the collateral.

A detailed loan agreement may indeed contain more detailed terms about what happens in case of default, potentially making recovery more predictable.

However, with a well-drafted promissory note, lenders should not face a significantly higher difficulty in debt recovery. The key is understanding the obligations and protections of each instrument to ensure proper use and enforcement.

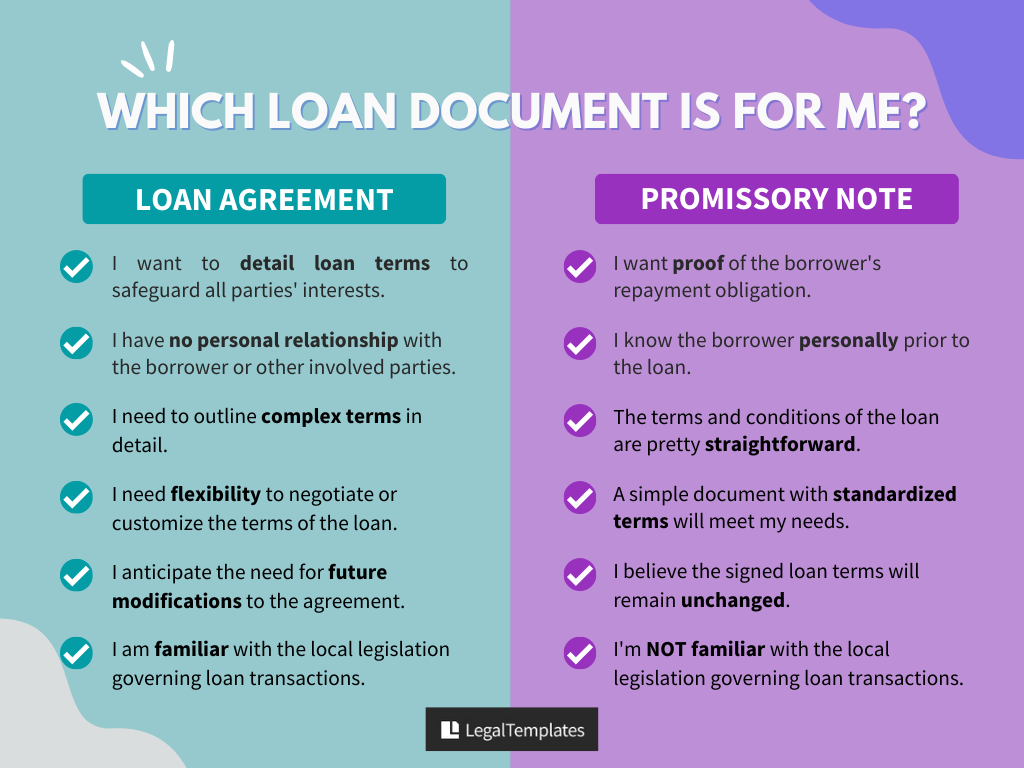

Which Loan Document Is for Me?

We’ve created a simple test to help you determine which document better suits your lending situation.

Below are multiple descriptions labeled ‘A’ and ‘B,’ representing different loan aspects. Read the descriptions and choose the best fits your situation for each pair.

Purpose

(A) I want proof of the borrower’s repayment obligation.

(B) I want to detail loan terms to safeguard all parties’ interests.

Relationship

(A) I know the borrower personally prior to the loan.

(B) I have no personal relationship with the borrower or other involved parties.

Terms

(A) The terms and conditions of the loan are pretty straightforward.

(B) I need to outline complex terms and conditions in detail (i.e., multiple parties, specific repayment methods).

Flexibility

(A) A simple document with standardized terms will suffice.

(B) I need flexibility to negotiate or customize the loan terms.

Amendment

(A) I believe the signed loan terms will remain unchanged.

(B) I anticipate the need for future modifications to the agreement.

Familiarity with Legislation

(A) I am NOT familiar with the local laws and regulations that govern loan transactions.

(B) I am familiar with the local laws and regulations that govern loan transactions.

RESULT

If you end up with more As: A promissory note can probably suffice.

If you end up with more Bs: Going with a loan agreement may be ideal.

It’s crucial to remember that the choice between a promissory note and a loan agreement often hinges more on the specific requirements of the lending situation rather than simply the size of the loan or the relationship the parties share.

Consult with a legal professional when making these decisions to ensure that your rights and interests are adequately protected.

Conclusion

Both loan agreements and promissory notes have their place in financial transactions. The key is understanding their differences, benefits, and limitations and choosing the correct document for your situation.

Join the 135,000 users who created their loan documents with us now.