A debt collector cease and desist letter is a correspondence you can send to a debt collection agency to ask them to stop repeatedly calling you, harassing you with messages, or trying to intimidate you in any way. The letter warns the debt collection agencies that you’ll take legal action unless the agencies respect your rights under the Fair Debt Collection Practices Act (FDCPA). [1]

How Often Can a Debt Collector Call Me?

Although federal law prohibits debt collectors from harassing you, the number of times they can call you is not specifically restricted. However, a debt collector is not permitted to harass or annoy you by calling or contacting you on a consistent basis.

You should send a cease and desist letter to a debt collector when the debt collector violates the FDCPA by harassing you illegally or committing other violations. Reasons for sending a cease and desist letter to a debt collector include:

- You don’t owe the debt.

- The debt collector is unable to verify the debt after receiving a request for validation.

- You did owe the debt, but the statute of limitations has expired (the time has passed when the collector can sue you).

- You don’t want to deal with debt collectors anymore (the debt collector can then only attempt to collect the debt by suing you in court).

Is a Cease and Desist Debt Collection Letter Legally Enforceable?

No, a debt collector cease and desist letter isn’t legally enforceable. It only warns that you’ll take legal action unless their violating behavior stops. Ideally, the agencies will stop contacting you as soon as they receive the letter, but you may need further action if they don’t.

Sending a cease and desist letter won’t forgive your debt, but it should stop the debt collection agency from unlawfully calling you. However, the debt collector can still sue you to collect the money owed.

Ways to Stop Debt Collection Calls

Here are some ways to stop debt collection calls:

Add Your Phone Number to the Do Not Call Registry

Consider adding your phone number to the Do Not Call Registry. When your phone number is on this registry, you may experience fewer unwanted calls.

File a Complaint with the Federal Trade Commission (FTC)

You can file a complaint with the FTC if an organization is engaging in bad practices, like harassing you about a debt.

Confirm the Debt is Yours

You can confirm the debt is yours with a debt validation letter. If the debt collector isn’t able to verify the debt is yours, they may stop contacting you about payment.

How to Write a Debt Collector Cease and Desist Letter

Follow these steps to write your cease and desist letter:

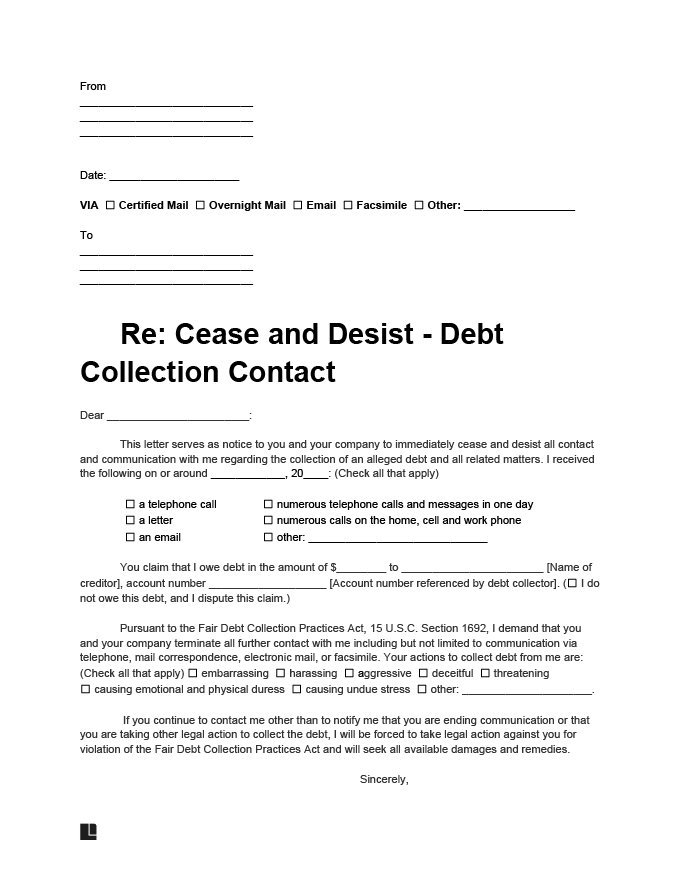

Step 1 – Fill Out the Header

Fill out the header with your and the debt collector’s names and mailing addresses. Specify the delivery method, whether it’s overnight mail, facsimile, or something else.

Step 2 – Address the Recipient and Explain the Situation

Address the name of the company/collection agency that’s trying to collect payment from you. Explain that they’ve been repeatedly contacting you, ensuring to provide the date(s) of the correspondence and the medium(s) through which they contacted you.

Step 3 – Specify the Amount Owed

Clarify the amount they’re seeking from you, and specify whether you’re disputing the claim.

Step 4 – State the Effect of the Debt Collection Process

State whether the debt collection process is causing you embarrassment, undue stress, or physical duress. You can specify how the process is affecting you personally to make a stronger case for the debt collector to stop their efforts.

Debt Collector Cease and Desist Letter Sample

Below, you can review our debt collector cease and desist letter template and download it as a PDF or Word file:

Frequently Asked Questions

What happens if I don’t pay an outstanding debt?

Refusing to pay a legitimate outstanding debt may affect your credit score. The creditor may also bring you to court to sue you for the amount owed.

How to send a cease and desist letter to debt collectors?

To send your cease and desist letter to a debt collector, you must send the letter by certified mail and the requested return receipt. Although this costs more, you will receive an official notification when the debt collector receives the letter, giving you documentation if you need to file a further complaint or sue the collection agency in court.

Is it legal for debt collectors to call me?

Yes, in general, it is legal for debt collectors to call you if they are attempting to collect a debt. However, some restrictions are in place to prevent debt collectors from stepping over the line and becoming abusive. The FDCPA limits what debt collectors can do when collecting specific types of debt.

Violations of FDCPA include:

- Calling more than seven times over the course of seven consecutive days

- After having a telephone conversation about the debt in question, you are called again within seven days about the same debt.

- Calling before 8 AM or after 9 PM.