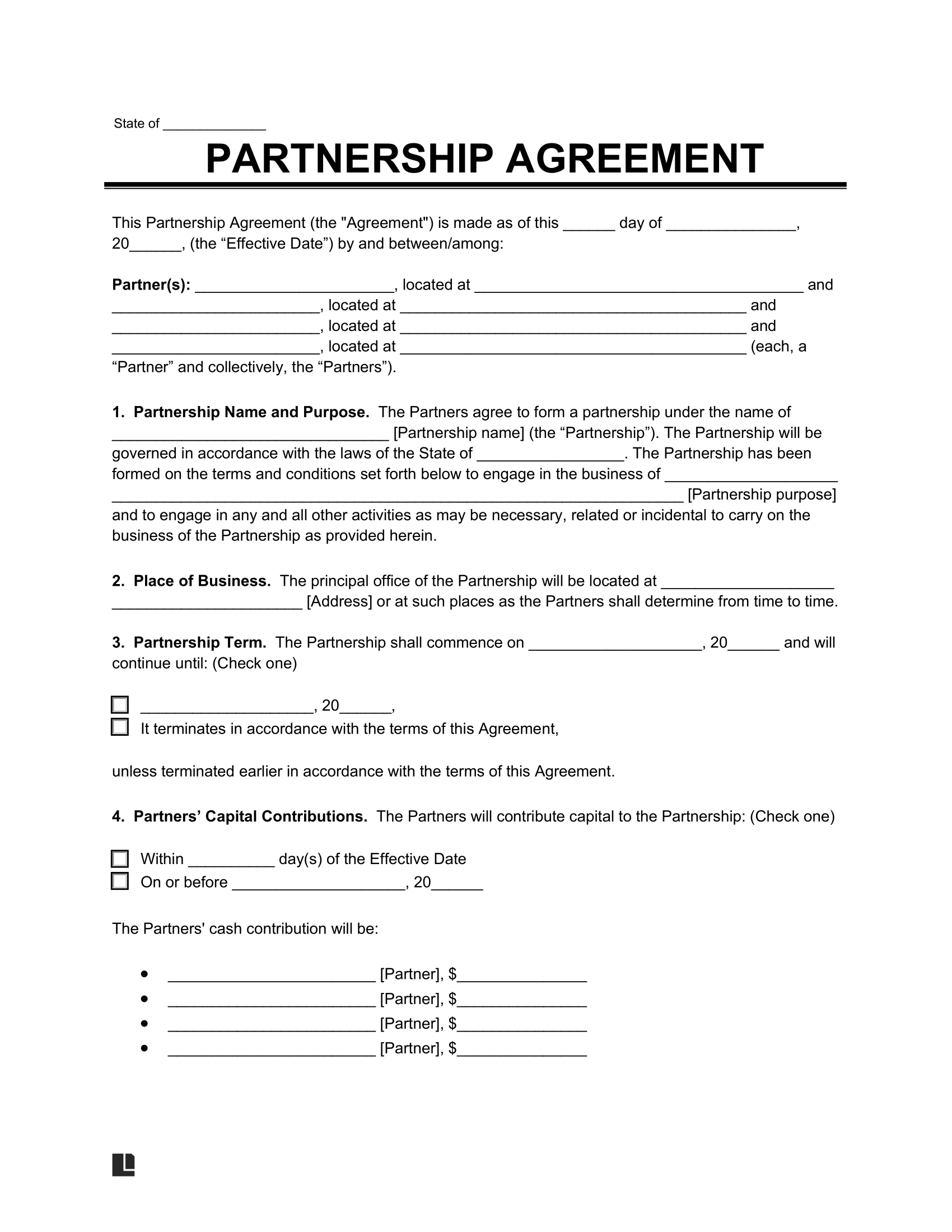

What Is a Partnership Agreement?

A partnership agreement is a written contract between two or more people who run a business together. It explains each partner’s roles, responsibilities, ownership shares, and how profits and losses will be divided.

Having an agreement prevents misunderstandings and protects each partner’s interests if problems arise.

What Should Be Included in a Partnership Agreement?

A well-drafted agreement covers the key details of how your partnership will run. At minimum, it should include:

- Partner information: Names and addresses of each partner.

- Business name: The official name of your partnership.

- Purpose: What products or services you’ll provide.

- Location: Where your business operates.

- Start date and duration: When your partnership begins and if it has an end date.

- Contributions: What each partner is investing (cash, property, services).

- Ownership shares: How much of the business each partner owns.

- Profit and loss distribution: How you’ll split profits and cover losses.

- Management roles: Who makes decisions and handles daily operations.

- Bank accounts and bookkeeping: Where funds are kept and how records are maintained.

- Partner changes: What happens if someone withdraws, retires, dies, or is removed.

- Buyout terms: How a partner’s interest will be valued and bought out.

- Dispute resolution: How disagreements will be settled (for example, arbitration).

- Governing law: Which state’s laws will apply.

How to Write a Partnership Agreement

Drafting your partnership agreement is easier when you break it into clear sections. Each part ensures your business runs smoothly and that all partners understand their rights and responsibilities.

1. Basic Partnership Information

Start by clearly identifying the partnership. This section should include:

- The full names and addresses of each partner.

- The date your agreement becomes effective.

- The state laws that will govern your partnership.

This helps avoid confusion about when your partnership officially begins and under which legal rules it will operate.

2. Partnership Name, Purpose, and Location

Next, outline the:

- Official business name (if registered with the state).

- Business description and products/services.

- Physical address of the partnership.

3. Duration of the Partnership

How long will the partnership last? Many partnerships continue until partners agree to end them, but yours might have a specific end date tied to a project or investment.

4. Capital Contributions

Outline what each partner is bringing to the business. This could be cash, property, or valuable services. Also, state when these contributions are due and whether you expect additional contributions in the future.

5. Capital and Income Accounts

Explain how you’ll handle partners’ capital accounts and income accounts. For example, you might note:

- Whether contributions earn interest.

- How profits and losses are allocated: equally, based on contributions, or using another ratio.

6. Profit, Loss, and Distributions

When can profits be withdrawn and how will losses be shared? Some partnerships allow withdrawals anytime, others require partners to wait until year-end or get consent.

7. Partnership Banking

Identify where your partnership funds will be kept by naming your financial institution. Also, list who has the authority to sign checks or make withdrawals, so there’s no confusion over who controls business funds.

8. Books, Records, and Accounting

State where you’ll keep financial records and who can inspect them. Define your fiscal year and how often financial statements will be prepared. You might also decide whether to allow audits on a regular schedule or only if requested by a partner. You may designate an accountant to handle the finances of the partnership and prepare tax forms.

9. Management and Major Decisions

Explain how your partnership will be managed day-to-day and how significant decisions will be made. For example, partners might be able to make ordinary decisions individually but require a majority or unanimous vote for large contracts or new loans.

10. Partner Withdrawal and Removal

What if a partner wants to leave? This might include:

- Giving a set amount of notice.

- Waiting until after a certain period.

- Needing unanimous consent to exit.

Also, how can partners be removed if they harm the business.

11. Retirement and Death of a Partner

Address what happens if a partner retires or passes away. Your agreement could allow remaining partners to buy out the departing partner’s share, or it might automatically end the partnership.

12. Buyout Terms

To avoid future disputes, outline how you’ll value a partner’s interest if they withdraw, retire, or pass away and how the buyout will be paid.

13. Restrictions, New Partners, and Arbitration

Note any restrictions on transferring partnership interests. Decide if and how new partners can be admitted. Finally, clearly state how disputes will be resolved (such as through arbitration) and specify which state’s courts will have jurisdiction over any legal proceedings.

14. Additional Legal Provisions and Signatures

Add any extra clauses you need, such as confidentiality rules or insurance requirements. Then have each partner sign and date the document to make it official.