What Is a Payment Agreement?

A payment agreement (also called a payment plan agreement or installment agreement) is a legal contract between a lender and a borrower that outlines how and when a debt will be repaid.

This document is often used when:

- A business sells goods or services, but the buyer needs to pay over time.

- Two individuals want to create a private loan repayment plan.

- Someone wants to restructure existing debt into scheduled payments.

A written payment agreement helps avoid disputes by clearly stating the terms. It also serves as evidence if you ever have to enforce payment in court. Even though verbal contracts can sometimes be legally binding, they’re much harder to prove.

How to Write a Payment Agreement

A solid payment agreement lays out all the details so both parties know exactly what to expect. Here are the essential points you’ll want to cover in your document:

If you don’t yet have a formal contract for the original debt, consider first creating a loan agreement. This document lays out the borrowing terms in detail before structuring a payment plan.

1. Names and Addresses of the Parties

Start by listing the full names and addresses of the lender (the person or business owed money) and the borrower (the person paying back the debt).

2. Amount of Debt and Reason

Spell out the total amount that needs to be repaid. It’s also important to explain where this debt came from, whether it’s tied to a service you performed, products that were delivered, or an unpaid invoice that’s been sitting too long.

3. Payment Schedule

Specify if the borrower will:

- Pay a lump sum by a certain date, or

- Pay in installments, detailing:

- How much each payment will be

- How often payments are due (weekly, biweekly, monthly, etc.)

- When the first and last payments are expected

This is often laid out in a simple schedule or attached as Exhibit A.

4. Payment Method

Explain how payments will be made. Common options include:

- Cash

- Personal check or cashier’s check

- Money order

- Electronic transfer

- PayPal or another online service

Also note if payments will be mailed, delivered by hand, or sent electronically.

If you wish, you can include a discount to encourage faster repayment. For example: “Borrower will receive a $200 discount if the full amount is paid by October 1, 2025,” or “A 5% discount applies to each installment paid at least 7 days early.” Clearly spell out the discount amount and conditions to avoid misunderstandings.

5. Default and Acceleration Clause

Add a section explaining what happens if the borrower falls behind. For example, you might say that if a payment is more than a certain number of days late, the full unpaid balance will come due right away. Consider whether a notice is required before the borrower may be held in default. This protects the lender by allowing them to demand all remaining payments at once if the borrower stops paying.

6. Indemnification and Release of Prior Claims

Make sure your agreement says the lender won’t pursue any old penalties or fees related to this debt. This keeps the focus on the new plan and what’s expected going forward, helping both parties start fresh under these updated terms.

7. Governing Law and Severability

Indicate which state’s laws will govern the agreement. Also include a clause that says if one part of the contract is invalidated by a court, the rest still stands.

8. Signatures

Both the lender and the borrower should sign and date the agreement. Typed or printed names under the signatures help avoid confusion. While a payment agreement probably doesn’t have to be notarized, adding a notarization can legitimize the document.

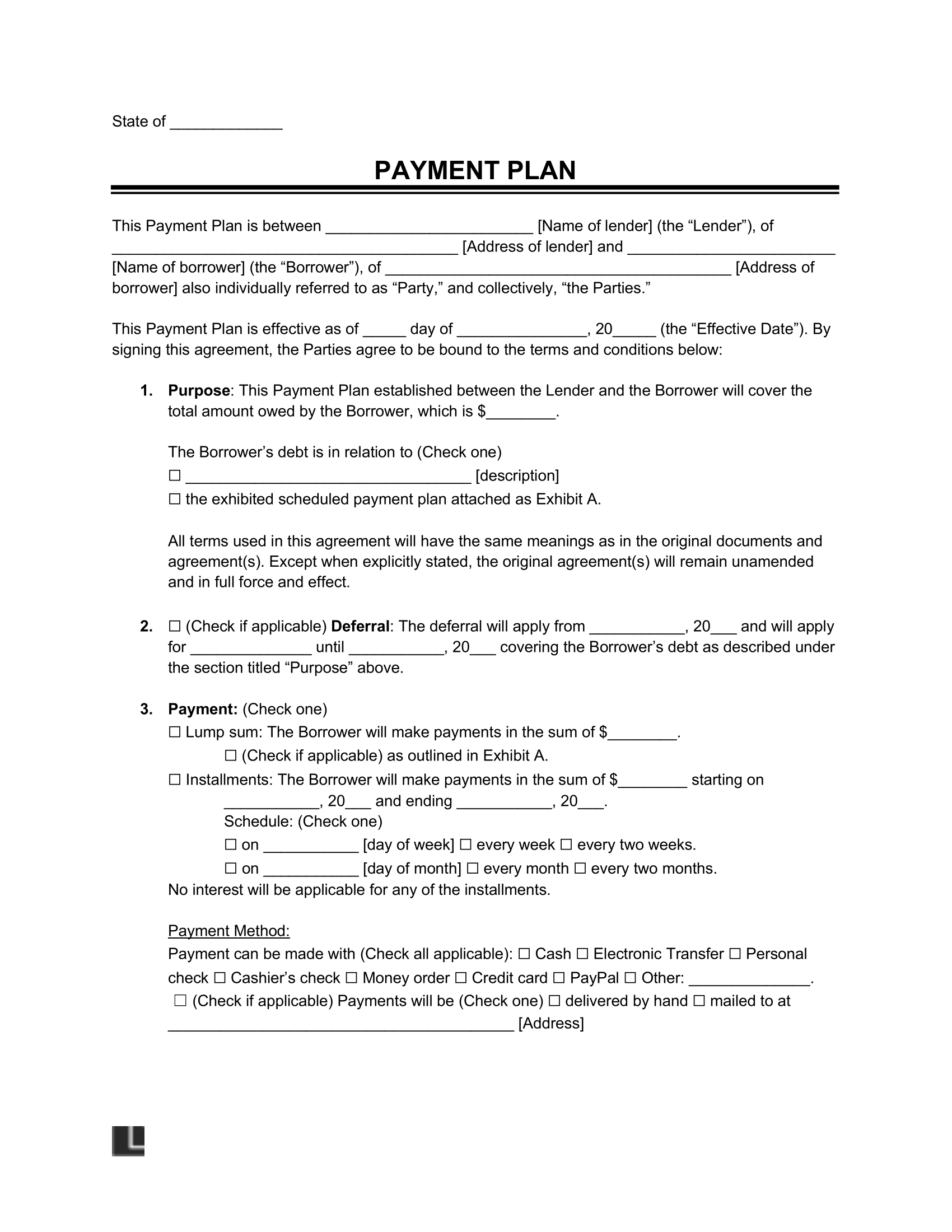

Payment Agreement Sample

Below, you can view a sample payment plan. You can customize this template with Legal Templates and then download the completed agreement in PDF or Word format.