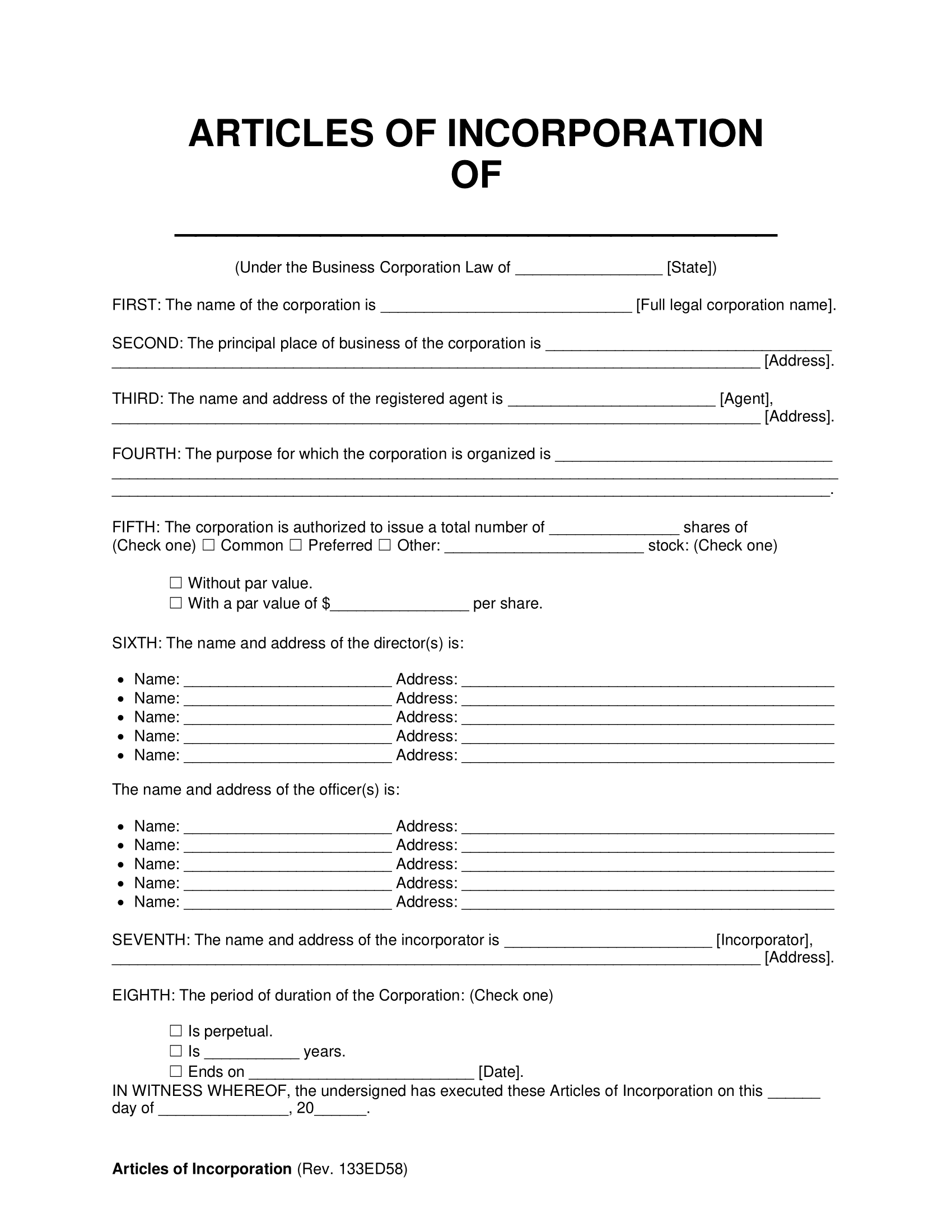

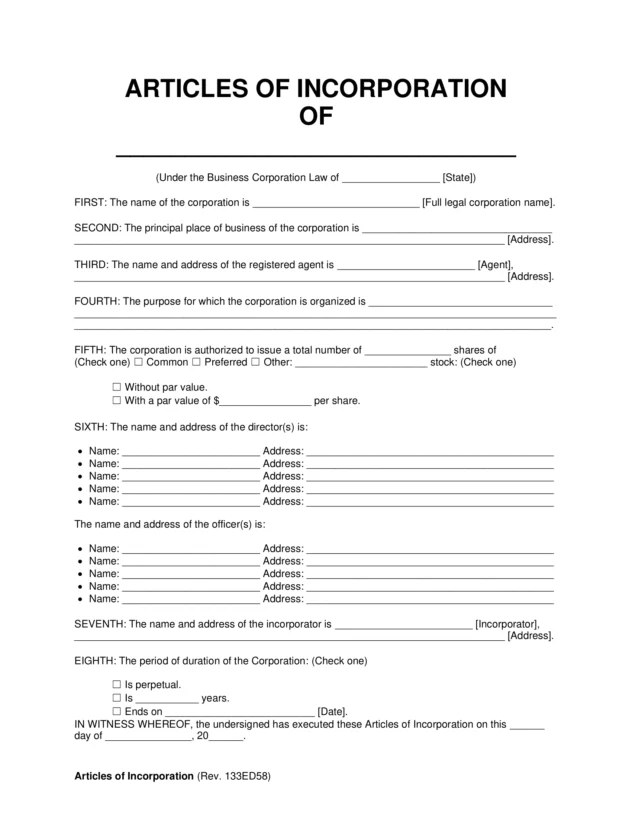

What Are Articles of Incorporation?

Articles of incorporation are formal documents you submit to your state to legally form a corporation. They establish the business as a separate legal entity from its owners. This structure protects the owners from personal liability for the company’s debts.

Articles of incorporation contain details like the business’s name, address, and registered agents. They also describe the business’s purpose and organizational structure, like whether it’s an S corporation or a C corporation. Once filed with the Secretary of State, the articles become part of the public record.

Start writing your articles today with Legal Templates. Our guided form walks you through the process. Include all essential details to meet legal standards and seek approval as an incorporated entity.

How to Write Articles of Incorporation

When you write your articles of incorporation, you must include key information to ensure the state approves your incorporated entity. Follow these steps to get started with the writing process.

1. List Corporation Details

Start by choosing the state where you will start your business. You can easily do so within our guided form, and we fill in the relevant laws for easy reference.

Then, list your corporation’s name, address, and mailing address. When choosing a name, make sure it’s available by researching your desired name in your state’s Secretary of State database. If your desired name is already used, choose a different one.

You should also include a statement of your business’s purpose. Consider keeping it general so that you can expand operations later.

If your business is known by a trade name different from its legal name, you may also want to include it here.

2. Name the Involved Parties

Once you provide the initial information, you can name the involved parties:

- Registered agent: A registered agent receives legal documents on the corporation’s behalf. Typically, they must have a physical address in the corporation’s state.

- Incorporator: You are the incorporator, the author of the articles. You are also responsible for filing the articles with the state.

- Directors: Directors are in charge of the corporation’s broader affairs. Some states require you to list the directors in your articles, while others make it optional. Check your state’s requirements to ensure compliance.

- Officers: Officers manage your corporation’s daily affairs. They include the corporation’s president, secretary, and treasurer. You don’t have to name them in your articles, but you can if desired.

Legal Templates’ form offers convenient spaces to fill in all required parties. Highlight everyone involved to complete a cohesive final document.

3. Describe the Authorized Capital

Authorized capital is the amount of stock the company will issue. It signifies its monetary value when it’s first incorporated. Our form lets you fill in information for the number of shares issued and the type of stock (common, preferred, etc.).

You can also indicate whether the stocks will come with or without par value. Par value is a nominal dollar amount assigned to each share in your articles. It’s the legal minimum, not the true market value. If you write your articles and don’t include par value for your shares, the board of directors can decide the value of the shares when they’re issued.

Issuing Stock

Once you issue stock, distribute a stock certificate to provide the holder with proof of ownership.

4. Provide Final Details

State the effective date and the duration of the agreement. Our questionnaire lets you select from the following options for your flexibility:

- No end date

- Ends after a certain number of years

- Ends on a certain date

You can also include supplemental provisions about meeting procedures, voting rights, indemnity statements, and other matters you want to cover. You may also choose to leave these out of the articles and include them in another company document, such as its bylaws.

5. Obtain Signatures

As the incorporator, be sure to sign the completed document. Also, acquire your registered agent’s signature to have them accept their duties. Articles of incorporation typically don’t need notary acknowledgment, as the state’s review is sufficient.

How to File Articles of Incorporation

Most states require the incorporator to file their articles with the state’s Secretary of State. However, some states have different state departments or agencies that handle business filings. For example, Arizona has the Arizona Corporation Commission. Check your state’s requirements to ensure you follow the proper steps.

Once you know where to file, you can prepare to submit your documents. Prepare to pay a filing fee, as it can range between $50 and several hundred dollars, depending on your state. Articles become part of the public record after filing, so they’re searchable online if you misplace them.

Your business doesn’t need to only operate in the state where you formed it. But many states require businesses to fill out “foreign registration” forms if the company was started in a different state and wants to do business there. These forms allow the company to legally transact business in another state.

After Filing Articles of Incorporation

After filing, you can implement these steps for success:

- Drafting corporate bylaws: Outline how your business will be governed.

- Hold an initial board of directors meeting: Use this meeting to adopt bylaws, appoint officers, and issue shares.

- Obtain an Employer Identification Number (EIN): Get an EIN from the IRS for tax and banking purposes.

- Apply for business licenses or permits: The required licenses or permits will depend on your location and industry.

- File for a Certificate of Good Standing: It may be needed for banking, contracts, or registering in other states.

- Open a business bank account: This account keeps finances separate and supports limited liability.

- Remain compliant: File annual reports, pay required state fees, and maintain a registered agent.