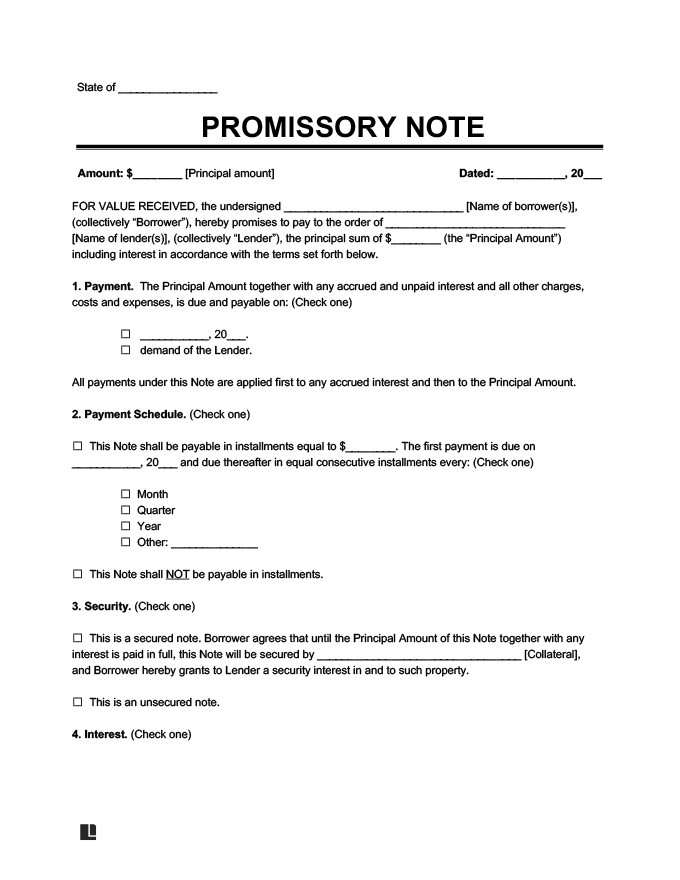

What Is a Promissory Note?

A promissory note is a written agreement where one party promises to repay a specific loan amount to another under agreed-upon terms. It clearly outlines repayment schedules, interest rates, and any applicable penalties, ensuring both parties understand their obligations.

This document provides a clear framework for trust, clarity, and accountability in personal loans, business funding, or real estate transactions.

When to Use a Promissory Note?

If you’re lending money to a friend or family member or helping finance a personal project, a promissory note can provide clarity and protection for everyone involved. By putting the loan terms in writing, both parties understand the expectations, reducing the risk of misunderstandings or disputes down the line.

Here are a few situations where a promissory note can be especially helpful:

- Personal Loans: When you’re lending money to someone you trust, setting clear terms can ensure both sides are on the same page.

- Real Estate: If you’re helping someone finance a property purchase or lending money for home repairs, a promissory note makes the agreement official.

- Business Loans: Whether you’re funding a new business or helping with expansion, a promissory note ensures the loan is documented and enforceable.

How to Write a Promissory Note

Creating a promissory note is straightforward when you know the key elements to include. Follow these steps to ensure your document is clear, legally enforceable, and tailored to your needs:

1. Identify the Parties

Start by listing the borrower (the person or entity receiving the loan) and the lender (the person or entity providing the loan). If either party is a business, include the business name and ensure an authorized representative signs the note.

If the lender is concerned about the borrower’s financial stability, they can request a cosigner. The cosigner agrees to take responsibility for the loan if the borrower defaults.

2. Define the Loan Terms

Clearly outline the loan’s details to ensure everyone understands the agreement. Include the following:

- Loan amount: Specify the exact amount the borrower will receive.

- Repayment schedule: Define how and when payments will be made—installments, lump sum, or on demand.

- Interest rate: State the percentage rate and confirm it complies with state usury laws.

- Collateral: List any assets being used to secure the loan, such as property or a vehicle.

- Due date: Include the final date by which the loan must be fully repaid.

- Late payment penalties: Explain the fees or consequences for missed or delayed payments.

- Default terms: Detail the lender’s rights if the borrower cannot fulfill their obligations, such as requiring immediate repayment.

- Prepayment terms: Indicate whether the borrower can repay the loan early and if there are any conditions or penalties for doing so.

Use simple, specific language to avoid misunderstandings and ensure the terms are enforceable.

3. Include Additional Terms

These optional clauses can make your promissory note more comprehensive:

- Amendments: Define how changes to the agreement can be made.

- Governing law: State which jurisdiction’s laws will apply to the agreement.

- Prepayment: Specify whether the borrower can repay the loan early without penalties.

- Joint and several liability: If there are multiple borrowers, state that they share equal responsibility for repayment.

- Right to transfer: Indicate whether the lender can transfer the note to another party.

Adding these provisions upfront can prevent disputes later.

4. Sign and Distribute the Note

All parties, including any cosigners, should sign the promissory note to indicate their agreement to its terms. While notarization isn’t required for most promissory notes, it’s a good idea for larger or more complex loans.

Tips for Signing

- Sign the note: Both parties, including any cosigners, should sign the note to make it legally binding.

- Store it securely: Keep the original note in a safe place, such as a lockbox or a fireproof safe.

- Make copies: Ensure both parties have copies of the signed note for their records.

- Backup digitally: Store a digital copy in a secure location, such as Legal Templates’ document editor, for easy access.

5. Enforce the Agreement (If Necessary)

If the borrower fails to meet their repayment obligations, you can take these steps to enforce the promissory note:

- Issue a demand letter: Send a formal demand for payment letter reminding the borrower of the loan terms and requesting payment by a specific date.

- File in small claims court: For loans under the state limit, you can pursue repayment through small claims court. This process is cost-effective and typically doesn’t require legal representation.

- Recover collateral: For secured promissory notes, reclaim the pledged asset, such as property or a vehicle, according to the terms outlined in the note.

- Explore additional legal options: If the loan exceeds small claims limits or the borrower continues to default, you may need to file a lawsuit in a higher court.

If the borrower fulfills their obligations, the lender can issue a promissory note release to acknowledge that the loan terms have been satisfied formally. This document proves that the debt has been repaid, providing clarity and closure for both parties.

Usury Limits by State

Usury laws set the maximum interest rates lenders can charge on loans, protecting borrowers from excessively high rates. Each state has its own rules, and these limits often depend on the type of loan and its terms.

Key Points:

- Usury rates ensure fair lending practices by capping annual percentage rates (APRs).

- State-specific laws determine the maximum interest rates for personal loans, mortgages, and business financing.

- Exceeding these limits may result in penalties for the lender and render the loan unenforceable.

Here’s a summary of state usury limits:

| State | Maximum Annual Rate | Additional Notes |

|---|---|---|

| Alabama | 6%; 8% if agreed in writing | No limits on loans over $2,000 |

| Alaska | Federal funds rate + 5% | No limits on loans over $25,000 |

| Arizona | 10%; no limit if contracted | |

| Arkansas | Federal discount rate + 5% | Capped at 17% |

| California | 7%; 12% if agreed upon | |