What Is a Colorado Promissory Note?

A Colorado promissory note is a legally binding document formalizing a promise to repay borrowed money. It outlines essential loan terms, like interest rates and repayment schedules, alongside details such as the parties’ names and addresses, the borrowed amount, and, if applicable, collateral securing the loan.

To prevent disputes, the parties must understand their rights and obligations under state law. Failure to adhere to the note’s stipulations may prompt the lender to initiate legal action against the borrower for breach of contract.

Laws: Given their contractual nature, promissory notes are governed by Colorado contract law and the Uniform Commercial Code.

Statute of Limitations: Six years (§ 4-3-118).

Types of Colorado Promissory Notes: Secured vs. Unsecured

In Colorado, promissory notes are issued as either secured—backed by collateral—or unsecured, based solely on the borrower’s promise to repay.

Secured Colorado Promissory Note

Ensures that if the borrower defaults, the lender can recover losses by repossessing or transferring the borrower’s property.

Unsecured Colorado Promissory Note

Enables an arrangement where the borrower isn't required to provide collateral to secure the debt.

Usury Laws and Interest Rates in Colorado

Promissory notes must comply with the state’s usury laws detailed in Colorado Revised Statutes Title 5, Articles 1-9 and Article 12.

- With a Contract (§ 5-12-103): Not more than 45% per annum.

- Without a Contract (§ 5-12-101): 8% per annum in the absence of an agreement.

- For Municipal Indebtedness (§ 5-12-104): 6% per annum.

- For Commercial Credit Plans (§ 5-12-107(2)(a)): Not more than 45% per annum.

- For Unsupervised Consumer Loan (§ 5-2-201(1)): Not to exceed 12% per year on the unpaid balance.

- For Supervised Consumer Loan (§ 5-2-201(2)): 21% on the total loan amount or 36% for amounts up to $1,000, 21% on $1,001 to $3,000, 15% above $3,000, whichever is greater.

- For Deferred Deposit/Payday Loan (§ 5-3.1-105): 36%.

- For Judgment for Damages (§ 13-21-101(1)): 9% per annum from the date the action accrued.

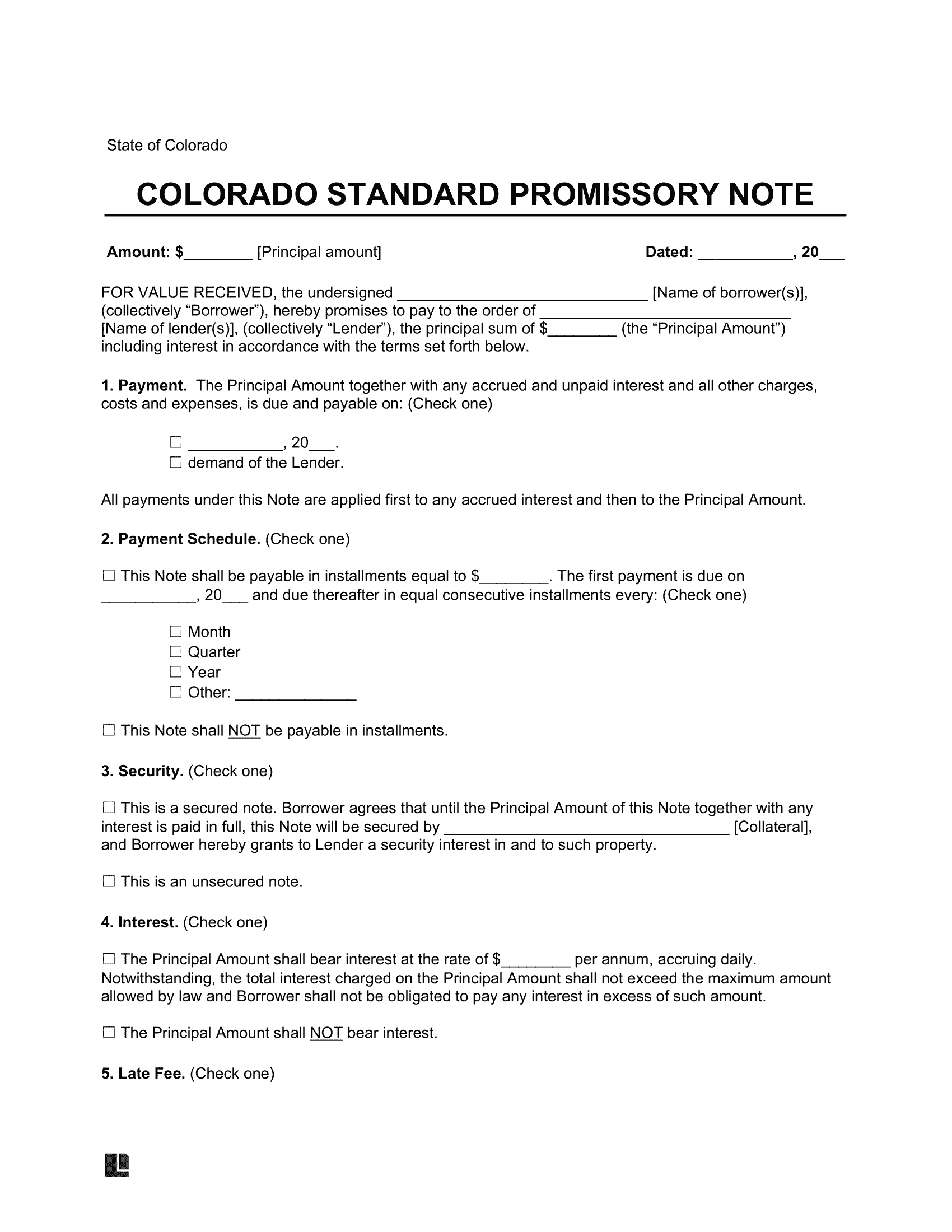

Sample Colorado Promissory Note

Below, you can see what a Colorado promissory note looks like. You can customize this template using our document editor and then download in PDF or Word format.