What Is a Secured Promissory Note?

A secured promissory note defines a borrower’s commitment to repay a loan, backed by collateral. The collateral acts as a security measure in case the borrower defaults on their loan payments. If a default occurs, you, as the lender, can seize the collateral to recover the remaining debt.

An important distinction to make is that a secured promissory note only records the debt and the intent to create a security interest. It does not actually establish the security interest. Instead, a separate security document that gets recorded creates the lien, or the creditor’s right to the collateral. A separate security document can be:

- A deed of trust for a promissory note secured by real property; or

- A security agreement for a promissory note secured by personal property

Consider using a secured promissory note when the stakes are high or when you need additional assurance. Here are some situations where a secured promissory note is useful:

- When lending significant monetary amounts

- When lending to individuals you do not know well

- When lending to individuals with lower credit scores

- When offering a lower interest rate (to hedge against the risk of default)

Alternatives to a Secured Promissory Note

Not backing your loan with collateral? Use Legal Templates’s unsecured promissory note to record the debt. This document focuses on the repayment terms and the borrower’s commitment rather than an interest in specific assets. If you want something more informal, use an I Owe You (IOU) template.

How Is a Promissory Note Secured?

Securing a promissory note involves determining the collateral and officially recording the security. From there, you can fill out your asset-backed promissory note, sign it, and exchange funds. Learn more about the process of securing a promissory note below.

Step 1 – Determine the Collateral

Begin by determining the item that will be used as collateral. While its value does not need to be the exact loan amount, it should be sufficient to cover the loan amount.

Before finalizing a promissory note secured by real property or personal assets, evaluate these criteria to ensure the collateral provides adequate protection:

- Asset condition and depreciation. Will the asset require minimal maintenance? Will its value decrease by a minimal amount during the loan’s term?

- Market demand and desirability. Will it be easy to sell the asset if the borrower defaults?

- Market stability. Is the asset’s market activity stable, allowing for a worthwhile sale if the borrower defaults?

- Ease of title transfer. Does the asset have a clear title, free of any liens that could make transferring ownership challenging?

Hire a professional appraiser or conduct your own research using current market data to determine an accurate valuation.

Some examples of assets you can use as collateral include the following:

- Real estate, including residential homes, commercial properties, or land

- Vehicles and titled property, including cars, boats, or planes

- Financial assets, including savings accounts, certificates of deposit, and bonds

- Valuable personal property, including jewelry, fine art, machinery, or specialized tools

Step 2 – Secure the Asset

A secured promissory note does not secure the asset on its own. You and the borrower must enter into a security agreement, which grants you a legal interest in the collateral. This legally binding contract reinforces the asset’s role as collateral.

You should also consider filling out a Uniform Commercial Code (UCC) financing statement, commonly known as a UCC-1 Form. This form gets filed with the Secretary of State’s office in the state where the debtor resides (or in the state of organization if it’s a registered business). Filing creates public notice of your interest in the collateral, ensuring you have priority over other creditors.

While a security agreement is the most common tool for personal property, loans involving real estate require a deed of trust or mortgage deed.

Step 3 – Fill Out Your Secured Promissory Note

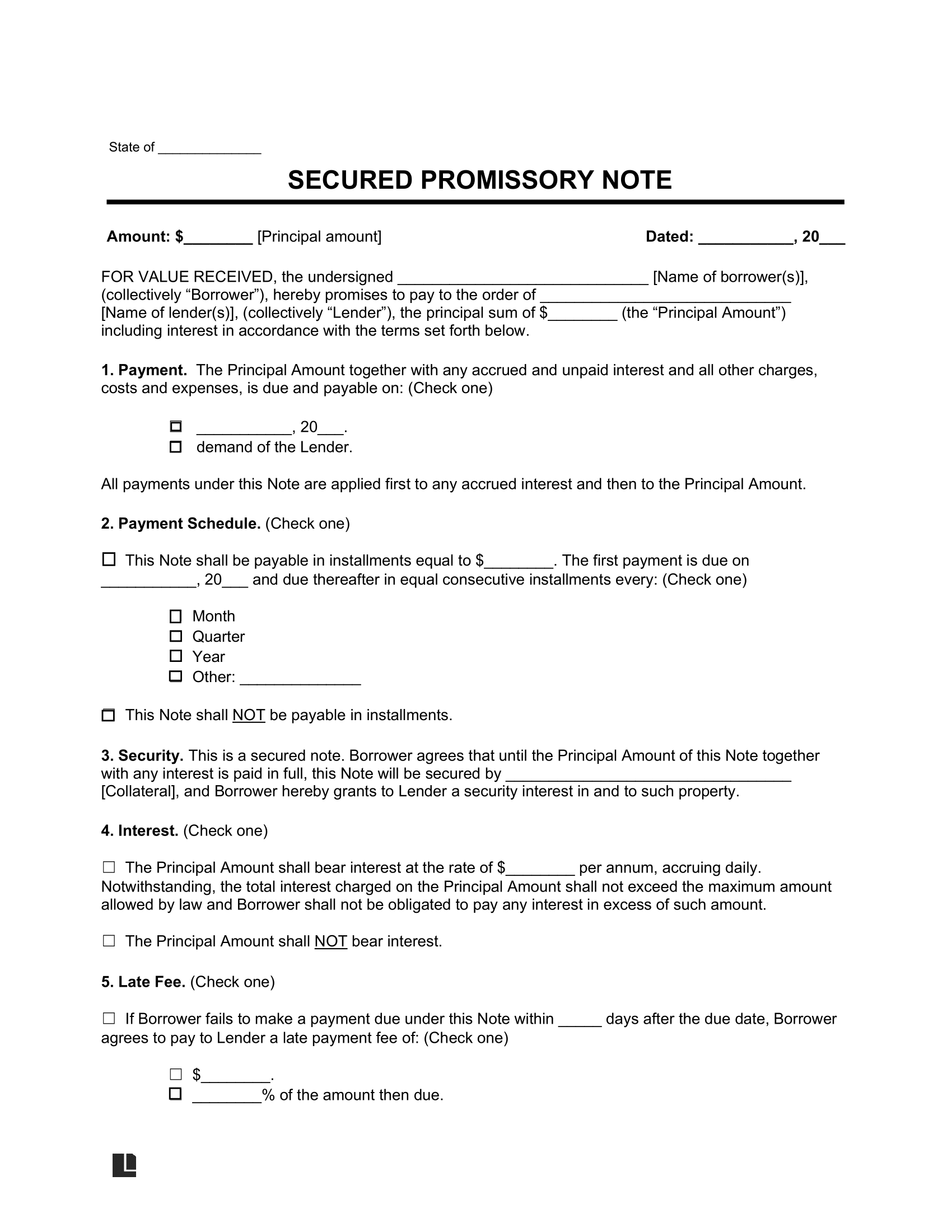

Once you officially secure the asset that you’ll use in your loan, you can start filling out your secured promissory note. Make sure to include these key details:

- Collateral description

- Consequences of default

- Acceleration terms

- Prepayment terms

- Late fees

- Principal amount

- Payment schedule

- On-demand provisions

Having a separate security agreement in place alongside your secured promissory note is essential. Without a separate recorded instrument, your secured promissory note can still be enforced as a personal debt, but you won’t have the legal authority to claim the collateral if a default occurs. Your note will function as an unsecured loan because it does not create a legally enforceable interest in the collateral.

A secured promissory note is a unilateral document, focusing on the promise to repay with the backing of collateral. If you want a more comprehensive contract that details all the terms between you and the borrower, use a loan agreement.

Step 4 – Sign, Exchange Funds, & Store Note Securely

You and the debtor should sign the secured debt agreement. These signatures ensure the document is legally binding and provide protection if either party defaults. The agreed-upon funds should be exchanged upon signing the note.

As the lender, you should retain the original copy in your records and provide a copy to the borrower for their records. Both parties should keep these on hand until the borrower fully repays the loan and is released with a promissory note release form.

Sample Secured Promissory Note

View an example of a secured promissory note to see how to record the details of a debt backed by collateral. Then, fill out your own with Legal Templates’s guided form. Once you’re done, you can download copies in PDF or Word format and distribute them to all parties involved.

How to Enforce a Secured Promissory Note

Once you have followed the above steps to secure a promissory note, you may be wondering how to ensure the debtor meets their obligations. A promissory note secured by collateral can be enforced using this process:

- Confirm default. Review the terms of your collateralized promissory note to ensure a default actually occurred. It may be a missed payment or the arrival of the maturity date without full payment.

- Notify the debtor. Send a formal written demand letter for payment to inform the borrower of the default. State the required cure, ensuring that you issue the proper amount of notice as per the original secured promissory note.

- Seize the pledged collateral. Take control of the collateral as outlined in the security agreement. You may be able to repossess vehicles or equipment, or go through the foreclosure process for real estate. Do not commit a breach of peace by using force, threats, or trespassing to seize property.

- Conduct a “commercially reasonable” sale. Once you seize the assets, you must sell them in a way that is “commercially reasonable” to ensure a fair price. Any proceeds you get from the sale should be applied first to the sale costs, then to the remaining loan balance.

- Seek a deficiency judgment. If the asset sale proceeds don’t cover the total debt, you may file a lawsuit for a deficiency judgment to pursue the borrower’s other assets or income for the remaining balance.

- Execute the judgment. Once you obtain a judgment, you can use the awarded legal tools to collect the remaining amount owed to you. For example, wage garnishment deducts payments from the debtor’s paycheck and distributes them to the creditor. Another possible judgment is a bank levy, which involves seizing funds in the debtor’s bank account.