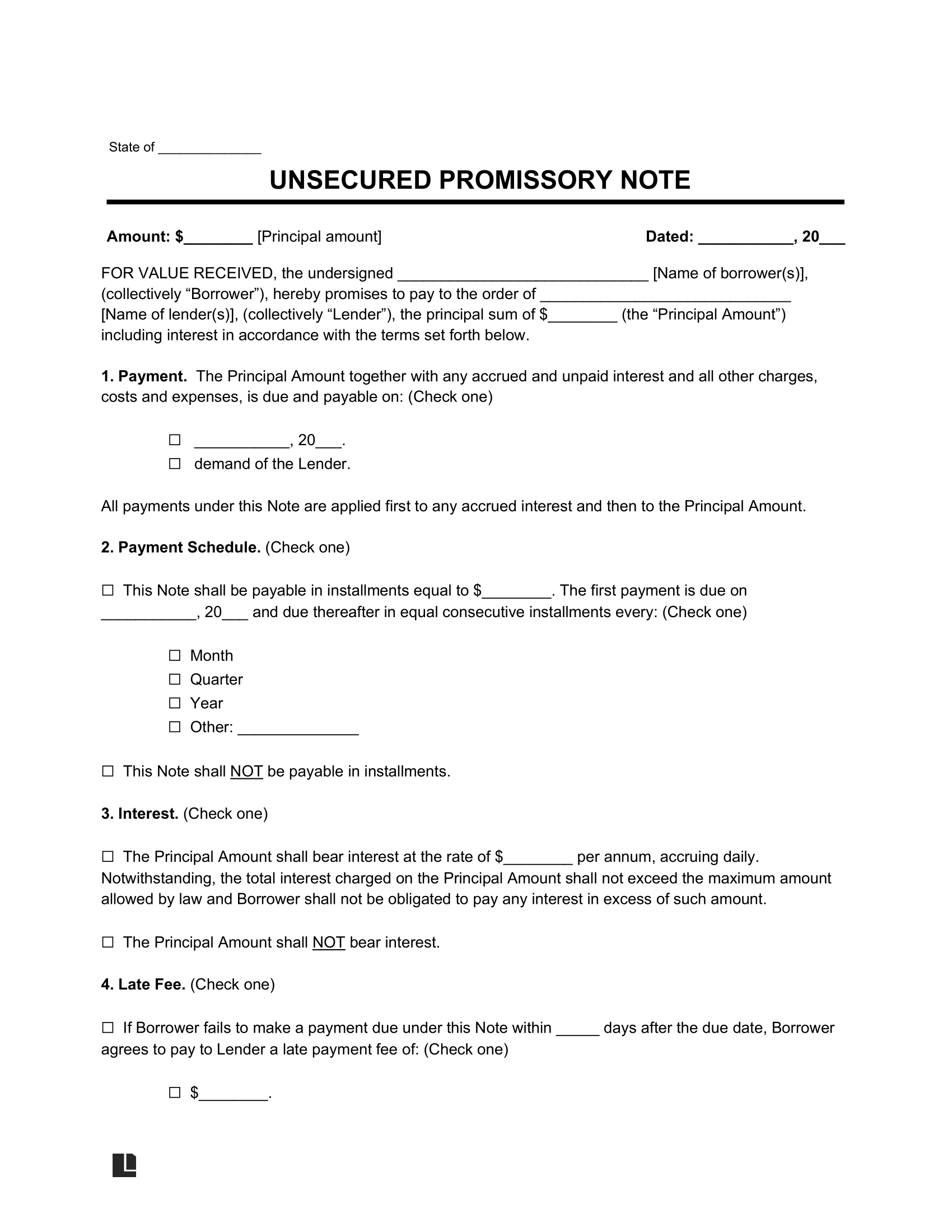

What Is an Unsecured Promissory Note?

An unsecured promissory note outlines the borrower’s obligation to repay a loan without pledging any collateral. It focuses on other terms, including the loan amount, interest rate, and repayment schedule. When the borrower and lender sign an unsecured note, it becomes legally enforceable if the borrower defaults.

Because an unsecured promissory note is not backed by collateral, it presents a greater risk to lenders. If the borrower defaults, the lender cannot immediately seize assets. Instead, they must go through lengthy court procedures to seek a judgment.

Since an unsecured note involves greater risk, it’s ideal for low-stakes situations or for quick loans. Consider using it in the following situations:

- When the loan is between trusted parties, such as friends, family members, or established business partners

- When the loan is for a small monetary amount over a short period of time

- When you need to issue a loan to help another party in an emergency

- When you want to facilitate short-term cash flow for a business venture

- When you want to issue a loan, but the other party does not have collateral readily available

Looking for a Safer Alternative?

Use a secured promissory note as a safer alternative to an unsecured note. A secured promissory note requires more setup, but it’s less risky because it’s secured by collateral.

How to Use an Unsecured Promissory Note

Unsecured promissory notes are riskier for lenders because there is no collateral to claim if the loan goes unpaid. You can mitigate this risk by knowing the borrower, defining the note’s terms, and understanding your options for debt recovery.

Step 1 – Screen the Borrower

Even if you are lending to a friend or family member, you should verify their ability to repay you. However, private individuals often cannot pull a formal credit report as easily as a bank or lender can.

The simplest way is to ask the borrower to pull their own free credit report and show it to you. They can use a website like AnnualCreditReport.com. Because laws like the Fair Credit Reporting Act (FCRA) are complex and mostly apply to businesses, you should speak with an attorney before trying to run a formal credit check on your own.

You can also ask the borrower to provide an employment verification letter to prove their ability to repay the loan.

Step 2 – Write the Terms

Write the terms of your unsecured promissory note. Clearly establishing the terms can help mitigate the risk that a lack of collateral can present. Here are some terms to clarify:

- Interest rate. Consider implementing a higher interest rate, as this can offset the risk of your note having no collateral attached to it. Whatever interest rate you establish, ensure that it complies with your state’s usury laws.

- Late fees. State how much the borrower must pay if they are late on their payments. Outlining late fees in advance can help you cover the administrative costs of handling delinquent payments.

- Payment schedule. Make the borrower’s obligations clear regarding how they will pay you. Specify whether you will collect the amount owed in installments, as a lump sum, or on demand.

- Default. Include what terms will result in a default of the note, such as a missed payment or consecutive late payments.

Other Documents to Document a Loan

If an unsecured promissory note won’t meet your needs, consider two other options:

- IOU template: An informal written promise that usually lacks legal enforceability. Ideal to use among family members and close friends.

- Loan agreement: A more formal agreement that focuses on the borrower’s and lender’s obligations, not just the borrower’s.

Step 3 – Strengthen the Unsecured Note Where Possible

With the lack of collateral at play, you can strengthen your unsecured promissory note where possible. For example, consider seeking a notary acknowledgment, as a notary public can ascertain that the note was signed willingly and without duress.

You should also have the borrower sign with a cosigner if one is available to them, as the cosigner will take legal responsibility for the loan from the start of its term. Another precaution is to establish the governing law for your unsecured promissory note. This provides the agreement with a clear framework, so the parties know in which jurisdiction disputes must be resolved.

Step 4 – Enforce Your Unsecured Promissory Note

Even though an unsecured promissory note does not have collateral attached to it, it can still be enforced. It will be more difficult to do so, but it is possible.

Once you determine that the borrower is not fulfilling their obligations under the note, you can issue a notice. Depending on the violation, you can send a demand letter for breach of contract or a demand letter for payment.

If the borrower still doesn’t comply within the granted notice period, you can take legal action by filing a lawsuit against them. While this process will cost you court filing fees and attorney fees, it may be worth it to recover the unpaid debt. The court can grant a judgment, allowing you to get some of the money back. For example, they may grant a property lien on the borrower’s property. This means if the borrower sells or refinances the property, you’ll get paid.

Alternatively, you can enlist the help of a debt collection agency. This is not a legal process. Instead, it’s a service that works on a contingency basis. They handle the work of chasing down the borrower, and if successful, they receive a percentage of the amount paid. If the borrower pays off their loan, you can issue a promissory note release form.

When entering into an unsecured promissory note, be prepared to accept the risk of not being repaid. While you have legal recourse, success is not guaranteed, especially if the note lacks the details required to withstand legal scrutiny. Also, your collection efforts, or those of a hired agency, may not achieve the desired results.

Sample Unsecured Promissory Note

View our simple unsecured promissory note template below. Legal Templates’s form makes it easy to include the key clauses and create an enforceable contract. Download your customized document in PDF or Word format to keep a record of the agreement.