What Is a Promissory Note Release Form?

A promissory note release form is a legal document that releases a secured or unsecured promissory note. It’s often used to show that the original note was paid in full. However, it can also be used to end the agreement under any of these circumstances:

- The lender and the borrower agree to end the note before full payment is made.

- The parties agree to replace the old note to update its terms, such as the maturity date or interest rate.

- The lender settles for less than the amount originally owed.

- The original promissory note has invalid terms and is unenforceable.

A release form is referred to as a “cancellation and release of promissory note” if the note is being released without being fully paid off. When the debt is completely paid off, the release is referred to as a “release and satisfaction of debt.”

A release from a promissory note sets the borrower free from their obligations under the loan. Once the lender signs the release, the borrower is no longer required to pay the principal amount, interest, or any late fees. The borrower also gets protection from future claims, as their ties to the loan end with the release form.

Does a Promissory Note Automatically Get Released Upon the Borrower's Death?

No, a promissory note is not automatically released upon the borrower’s death. A promissory note is a debt, so it goes into their estate. The estate’s executor is responsible for paying the debt using the deceased person’s assets.

A promissory note will only be released upon the borrower’s death if it includes a death discharge clause. This clause explicitly states that the debt is forgiven upon death, resulting in a release from the note.

How to Release a Promissory Note

You and the borrower should be certain about ending the loan before writing a promissory note release form. Once the release has been signed and issued, the note is terminated. Follow these steps to release a promissory note and ensure a smooth process.

Step 1 – Verify Fulfillment of the Promissory Note

Confirm that the borrower actually paid off the debt. If you both decide to end it for other reasons, determine that they have met the agreed-upon conditions for the note’s release, such as paying a lesser amount.

If the loan was secured by collateral, your legal claim doesn’t go away on its own. As the lender, you must “discharge” the security to give the borrower full ownership back. The instrument that you use to discharge the security depends on the type of property involved:

- Personal property. You can file a UCC-3 Termination Statement with the same office where the original lien was recorded.

- Real estate. If the loan was backed by real estate, the process is handled at the county level. You can file a deed of reconveyance or a satisfaction of mortgage, depending on local rules.

Step 2 – Fill Out the Promissory Note Release Form

Use Legal Templates’s promissory note release form to complete your document. We help you fill out the key details, including the following:

- The lender’s details

- The borrower’s details

- The date the original promissory note was created

- The principal amount of the promissory note

- Notary acknowledgment (optional but highly recommended)

- The date of the promissory note release

- The lender’s signature (or the representative’s signature if applicable)

You should attach the original promissory note to the release form to prevent the original note from being used to collect the debt a second time. If you have lost the original note, attach an affidavit stating that the original note cannot be recovered. Include all key details of the original note

Step 3 – Send to the Borrower & Store Copies

Make copies of your satisfaction of loan letter. Send one to the borrower via registered mail so you can ensure they receive it. Store another copy in your records so you can refer to it later if disputes or disagreements arise.

State laws vary on how long you should keep these types of financial records. It’s common practice (and aligns with IRS standards) to keep a satisfaction of promissory note document on file for at least seven years. You do not need to record your promissory note payoff letter at any local or state government office.

Tax Implications

If you release a borrower from their obligation before they pay the full amount, the IRS may view the unpaid money as income. Depending on the situation, the IRS might treat the canceled debt as taxable income for the borrower or as a taxable gift from the lender. Consult with a tax professional to understand how your circumstances can impact your tax liability.

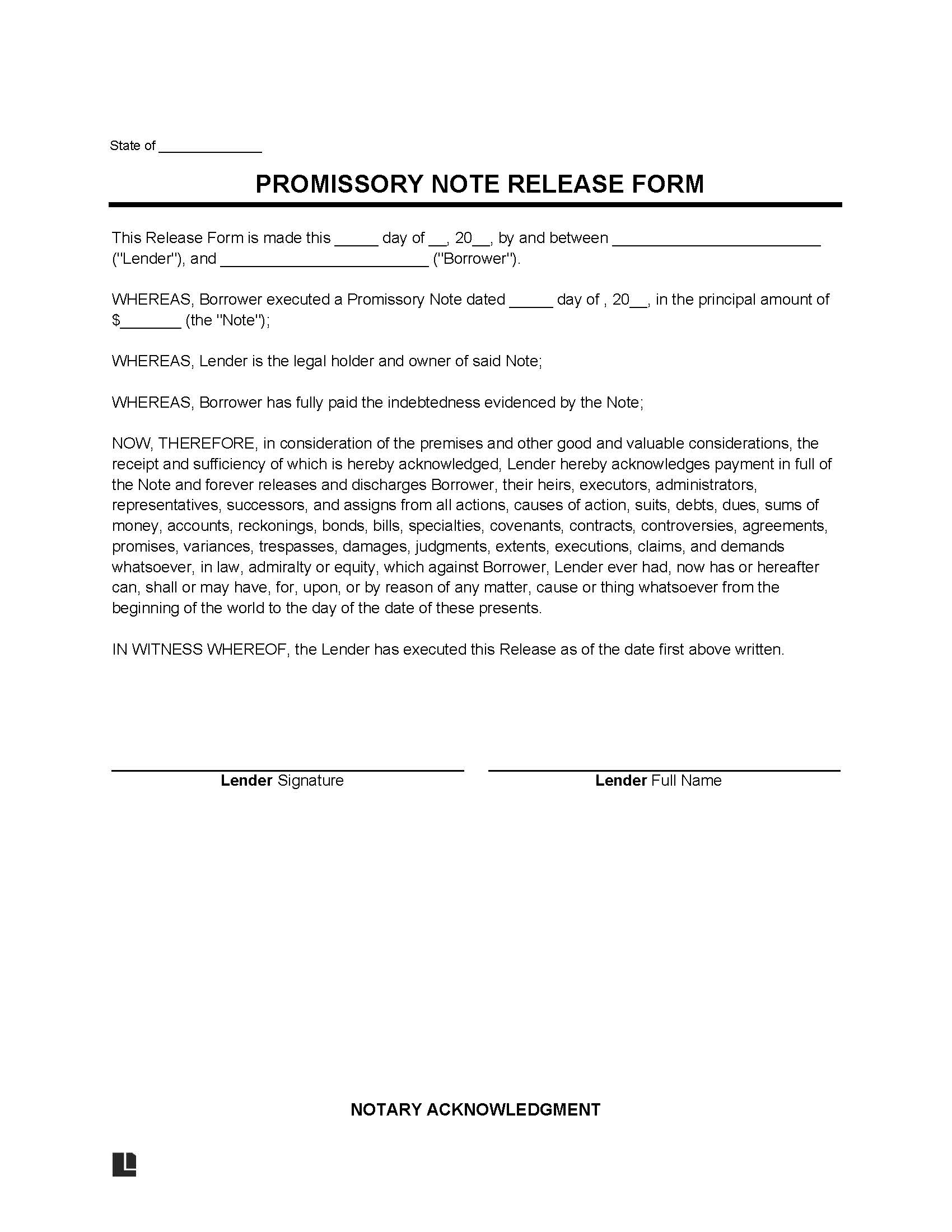

Release of Promissory Note Sample

View our printable release of promissory note template to see how to discharge someone from a loan. Once you’re ready, you can complete yours online with Legal Templates’s guided form. Then, download copies in PDF or Word format for distribution to the relevant parties.