What Is a Mortgage Deed?

A mortgage deed is a legal document that secures a home loan by placing a lien on the property until it’s fully repaid. It involves two parties, the borrower and the lender. By comparison, a deed of trust includes three parties.

The deed explains the loan terms. It states how much was borrowed, the repayment schedule, the interest rate, and what happens if the borrower defaults. Many also contain an acceleration clause, which makes the full balance due if payments stop. The purpose is to protect the lender. If the borrower fails to pay, the lender has the right to foreclose, often through the courts.

How Mortgage Deeds Affect Ownership

Ownership rules vary by state, and they generally fall into three categories:

- Lien theory: The borrower keeps legal title, while the lender holds a lien that gives them legal recourse. Most states follow this model.

- Title theory: The lender holds the title until the debt is cleared. Once the mortgage is satisfied, the borrower receives the title.

- Intermediate theory: A blend of both. The borrower keeps legal title, but if they default, the lender automatically gains title. Only a few states use this approach.

Lenders sometimes ask for a mortgage verification form during the loan process to confirm details like balance, interest rate, and payment history.

When to Use a Mortgage Deed

A mortgage deed comes into play when someone borrows or lends money to buy property. It secures the lender’s interest by placing a lien on the home until the loan is fully repaid. If part of the home purchase is funded by family or friends, lenders may also require a mortgage gift letter to confirm that the funds are a gift and not a loan.

You’ll find mortgage deeds in states that follow the mortgage deed system rather than deeds of trust. In these states, foreclosure takes place through the courts, known as judicial foreclosure.

A mortgage deed also applies when a buyer assumes an existing mortgage during a property sale. In those cases, the deed governs how the loan transfers along with the home. Because mortgage deeds are the most common way to finance real estate, they must be recorded in the public registry. Recording makes the lender’s claim official and adds it to the property’s history.

If you want to explore other ways to transfer property ownership, read our guide on the different types of deeds.

What to Include in a Mortgage Deed

For a mortgage deed to be valid, it needs the right details. Each element works together to make the lender’s rights clear and enforceable. If anything’s missing, the agreement could be challenged. Here’s what to include:

- Names of borrower and lender for official recording.

- Full legal property description from the deed or title.

- Loan instrument and execution date connecting the mortgage to the note.

- Principal amount secured by the mortgage deed.

- Interest rate on the debt.

- Promissory note summary outlining repayment schedule, maturity date, and what counts as a default.

- Prepayment penalty clause explaining any fees for early payoff or extra payments during the term.

- Escrow provisions require payments into an escrow account for property taxes and insurance.

- Default and remedies detailing grace periods, notices, and lender remedies.

- Assigned rents clause give the lender rental income if the borrower defaults.

- Power of sale clause for non-judicial foreclosure if state law allows.

-

Protective clauses that safeguard the lender’s rights, such as:

- Due-on-sale clause: Requires the loan to be paid in full if the property is sold.

- Due-on-encumbrance clause: Stops the borrower from adding new debts or liens to the property without the lender’s consent.

- Governing law clause stating which state’s laws apply.

A mortgage deed creates a legal record that can stand in court. With the right property details, loan terms, and lender-protection clauses included, it secures the lender’s rights and sets clear obligations for the borrower.

If you need a ready-made structure, you can use Legal Templates’ mortgage deed template to draft a compliant and professional agreement quickly.

What Happens to Deeds When a Mortgage Is Paid Off?

When a mortgage is paid off, the property deed changes status. The lender’s claim is removed, and the borrower becomes the full legal owner. The process is simple in principle, but updating the records can take some time. Here’s what happens:

- Loan payoff triggers action from the lender or loan servicer to prepare a satisfaction of mortgage (sometimes called a release of lien or deed of reconveyance, depending on the state).

- Satisfaction of the mortgage is recorded in public records, which removes the lender’s lien from the property deed.

- Full ownership transfers to the borrower, who now holds the property free of the lender’s security interest.

- Notification goes to the local records office from the lender or servicer confirming the payoff.

- The borrower may receive proof in the form of a property deed, certificate of satisfaction, or deed of reconveyance.

- Recording updates takes time, often a few days to several weeks, depending on local procedures.

- State property and contract laws govern the process, so exact steps can vary.

Payoff documents are worth holding onto because they confirm the lien is released and ownership is secure. Once the loan is paid off, the lender also closes the escrow account and returns any remaining balance to the owner.

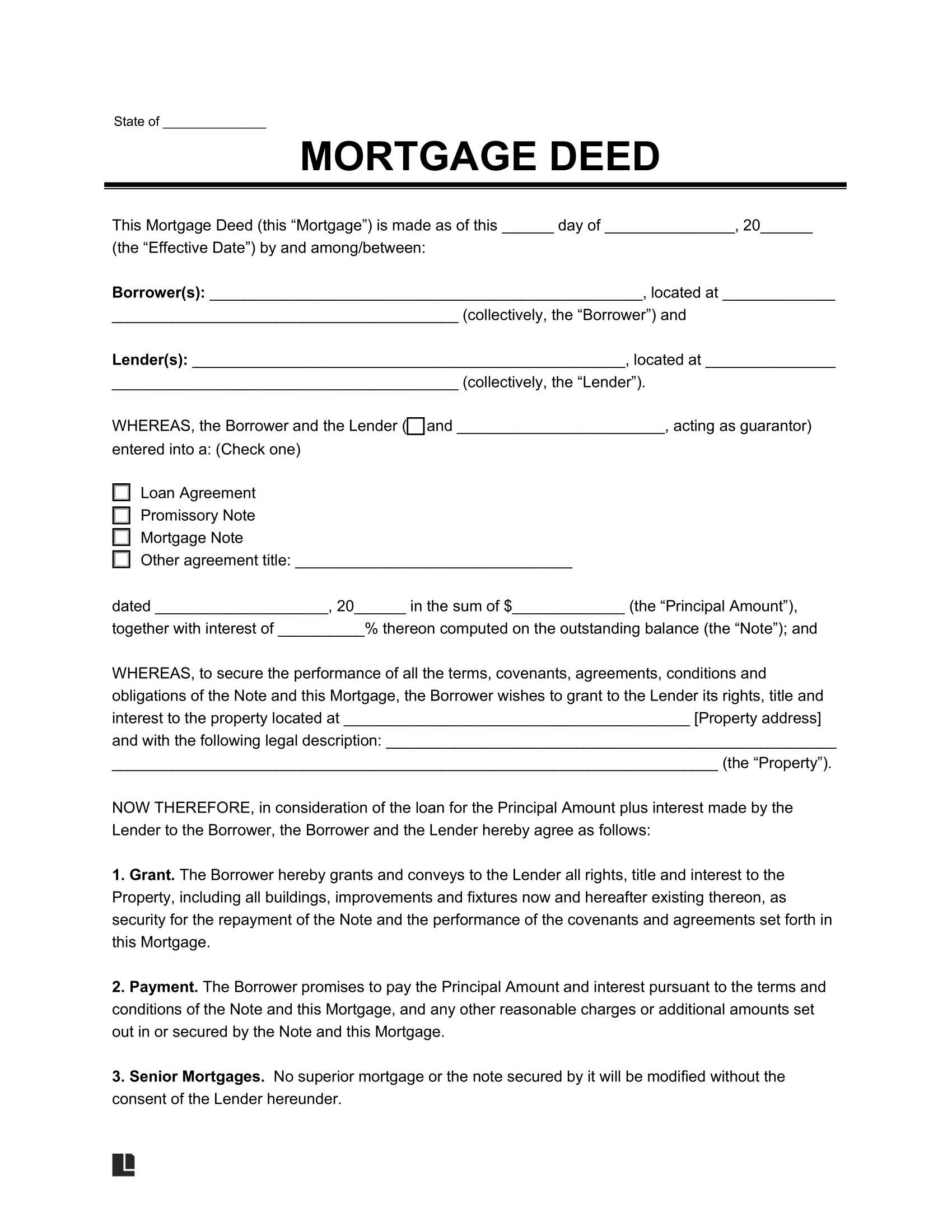

Sample Mortgage of Deed

Here’s a sample mortgage deed so you can see exactly how the document is structured. Use it as a reference, or customize and download a mortgage deed template in PDF or Word with Legal Templates.