A deed of trust is a document that dictates an arrangement between a borrower, a lender, and a trustee. It states that a lender will loan money to a borrower to purchase a home or another property, and the borrower will give the property’s legal title to the trustee as security against the loan.

What Is a Deed of Trust?

A deed of trust or trust deed officially recognizes a legally binding relationship between a borrower, lender, and trustee. The trustee holds the property’s title in trust for the lender until the borrower pays the loan in full. Once the borrower pays off the loan, the trustee returns the title to the borrower.

Please note that if the borrowing party consists of more than one person, each borrower must comply with all of the trust’s liabilities and obligations.

Who Is Involved With a Deed of Trust?

A deed of trust always involves three parties: the borrower, the lender, and the trustee.

Who Is the Borrower?

The borrower (or the trustor) is the person securing the loan. They borrow the money and pledge the property.

Who Is the Lender?

The lender (or the beneficiary) is the entity providing the loan. They receive a lien against the property.

The lender can use any legal methods available under relevant state laws to collect the owed debt on the deed of trust whether or not such remedies are listed in the document.

Who Is the Trustee?

The trust is the person who holds the title to the property for the lender. They’re a neutral third party, such as a real estate broker, attorney, escrow agency, trust company, or title company. If the borrower defaults, the trustee must transfer property to the lender to compensate for the lost amount. Check your state’s laws for restrictions on who can be a trustee.

There may also be a guarantor who agrees to be financially responsible for the loan or a co-signer who assumes equal liability for paying the loan.

Deed of Trust vs. Mortgage

Review some of the key differences between a deed of trust and a mortgage:

-

Parties Involved:

- Deed of Trust: A deed of trust has three parties: the trustee (the neutral third party), the lender (the beneficiary), and the borrower (the trustor).

- Mortgage: A mortgage only involves two parties: the lender (the mortgagee) and the borrower (the mortgagor).

-

Role of the Trustee:

- Deed of Trust: The trustee maintains the legal title until the borrower pays the loan back. They also enable the transfer of property to the lender in case the borrower defaults.

- Mortgage: There’s no trustee.

-

Geographic Variation:

- Deed of Trust: Only certain U.S. states use deeds of trust, such as Arizona, Texas, and California. States where non-judicial foreclosure is common are more likely to use deeds of trust.

- Mortgage: Mortgages are common in states that defer to judicial foreclosure procedures.

-

Title Transfer:

- Deed of Trust: While the loan is active, the trustee holds the legal title. The borrower has equitable ownership and maintains the right to use and live on the property.

- Mortgage: The borrower keeps the equitable and legal title. The lender keeps a lien on the property until the borrower fulfills their entire obligation.

-

Foreclosure Process:

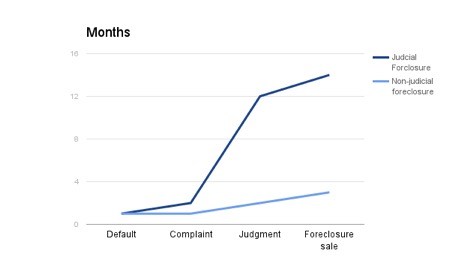

- Deed of Trust: A deed of trust usually contains a “power of sale” clause that allows the trustee to sell the pledged property in a non-judicial foreclosure sale if the borrower defaults. The trustee can bypass the court system and go straight to the foreclosure sale process. Unlike judicial foreclosure, a non-judicial foreclosure is a quick process that takes about two months.

- Mortgage: In judicial foreclosure under a mortgage agreement, the lender can only sell the property after receiving a judgment from the court authorizing the sale, forcing the lender to go through the formal court process. The judicial foreclosure process could take several months to years, depending on the court calendar, defense claims, and other factors.

View the timeline for foreclosure below:

How Does a Deed of Trust Work?

A deed of trust involves several steps. First, a lender must agree to loan a borrower money to purchase real property, including a house, land, or other immovable property. A lender and a borrower usually write a promissory note to dictate this agreement.

Then, the two parties use a deed of trust to finalize the loan and safeguard the lender’s interests. Under this document, an independent trustee receives ownership of a property’s legal title.

While the borrower makes their payments, the trustee retains the legal title. The borrower has the property’s equitable title, which is the right to live on or otherwise use the property.

Once the borrower fully repays the loan, the lender asks the trustee to give the borrower the property’s legal title.

IMPORTANT

If the borrower defaults, the lender can initiate a foreclosure. There must be a power of sale clause in place for the lender to take back the property in this manner.

When Do I Need a Deed of Trust Form?

A deed of trust is a critical security instrument in real estate transactions. Especially after the housing crisis in 2008 and today’s uncertain economy, lenders want added security that they will recoup the money they are lending to borrowers.

Because of this convenience, many states are moving away from mortgage agreements and allowing lenders to use deeds of trust.

Here is a table detailing some common borrowers and lenders who might need one:

| Possible lender | Possible borrower |

|---|---|

| Seller of a property or home | Buyer of a property or home |

| Private investor | Professional ‘flipper’ |

| Private mortgage company | Company looking to purchase an office |

| Family member 1. Uncle or aunt helping their favorite family member 2. Older wealthier family member divesting estate (i.e. grandparents) | Family member 1. Nephew or niece paying for first home or apartment 2. Younger less wealthy family members in need of financial assistance (i.e. grandchildren) |

| Sympathetic friend with extra funds (i.e. able to lend but not give money) | Reliable friend needing cash (i.e. for a real estate investment opportunity) |

Other Types of Deeds

If you want to explore other ways to transfer property ownership, read our guide on the different types of deeds.

Which States Allow Deeds of Trust?

Below, you can explore which states allow deeds of trust and the corresponding laws if they do. Also, see if each state allows for the use of mortgage agreements instead:

| State | Deeds of Trust Permitted? | Deeds of Trust Laws | Mortgage Agreements Permitted? |

|---|---|---|---|

| Alabama | Yes | AL Code §§ 35-10-11 to 35-10-16, § 35-10-3 | Yes |

| Alaska | Yes | AK Stat. §§ 34.20.070 to 34.20.135 | No |

| Arizona | Yes | AZ Rev. Stat. §§ 33-801 to 33-821 | Yes |

| Arkansas | Yes | AR Code, Title 18, Subtitle 4, Chapters 49 and 50 | Yes |

| California | Yes | CA Civ. Code §§ 2920 to 2944.10 | No |

How to Write a Deed of Trust

While there are multiple types of deeds, knowing how to create a deed of trust can help you gain a sense of security when loaning money to a trustor. Review the steps for writing your own:

Step 1 – Write the Effective Date

Write the date the document will go into effect.

Step 2 – Enter the Parties’ Information

Provide the full name and address of the parties signing the agreement. Indicate if the parties are individuals or entities. If any of the parties are entities, include the type of entity and the state of incorporation or formation.

Step 3 – Write the Loan Amount

Write the principal amount of the loan the lender provides to the borrower and the relevant interest rate.

Step 4 – Provide Loan Details

Indicate if a loan agreement, promissory note, or other document evidences the loan. Also, indicate if there’s a guarantor for the loan.

The following loan details outline the structure of the purchase deal and how you will repay it:

- Amount borrowed

- Payment terms

- Amount of each payment

- Interest details

- Interest adjustment date

- Date of the last payment

What Is the Amount Borrowed on a Mortgage?

The amount borrowed only includes the money you received from the lender to pay for the property. It does not include interest and fees.

Step 5 – Include a Property Description

Describe the property that is the subject of the loan and include as much detail as possible to identify the property accurately. Include the property’s street address and a legal description to clarify to which property you’re referring.

What Should I Include in a Legal Description?

The description should consist of exact survey information about the measurements of the property (e.g., metes and bounds, lots and blocks). It can also include details regarding any structures. Accuracy is essential.

Step 6 – Enter Financing Details

Provide details regarding the payment of principal and interest, partial payments, prepayments, application of payments, and funds for escrow items.

Step 7 – Note the Borrower’s Representations and Warranties

Select the representations and warranties the borrower will make under this deed of trust. Write in any other representations and warranties not already provided.

Step 8 – Enter Other Deed of Trust Details

Include details regarding maintenance and repair, property sale, sale of the note, events of default, acceleration, power of sale, and joint and several liabilities.

Step 9 – Write Miscellaneous Provisions

Provide for miscellaneous provisions, including the following:

- Prepayment penalty: Fees the lender imposes for paying the mortgage off early.

- Alienation: The borrower must pay the loan amount in full if they’re selling the property.

- Covenants: The borrower declares and promises ownership of the property and has the authority to mortgage the property.

- Default and Acceleration: The loan amount becomes due if the borrower defaults.

- Maintenance of Property: The borrower must maintain the property’s condition and obtain an acceptable amount of insurance.

- Ownership Transfer: If the borrower transfers ownership, the loan amount may become due.

- Rights of Lender: The lender can make payments to maintain the value of the property, which it can then add to the total loan amount.

- Security Interest: The deed of trust also secures any other liabilities of the borrower to the lender

- Senior Mortgages: Senior mortgages can’t be modified without the lender’s permission.

- Applicable Law: Indicates the state’s laws that will govern the agreement.

- Document Recording: Indicate the county or local clerk’s office where the document will be recorded to ensure searches of the property will reflect the lien.

Step 10 – Obtain Signatures

All parties will sign the deed of trust. You’ll also have a notary public acknowledge their signatures.

Correct minor details on a deed of trust using Legal Templates’s affidavit of correction.

Deed of Trust Sample

Download a free deed of trust template as a PDF or Word file so you can create your own:

Frequently Asked Questions

What Happens If I Don’t Use a Deed of Trust Form?

Without a deed of trust, a lender may have to go through a lengthy court battle to receive money. This form gives a lender recourse if a borrower suddenly stops making agreed-upon payments.

What’s the Difference between a Deed of Trust and a Warranty Deed?

A deed of trust gives temporary ownership of a property to a trustee, which helps assure the borrower will pay the lender back. A warranty deed confirms a property’s title has no encumbrances while one party transfers ownership to another.

Why Doesn’t a Borrower Just Get a Traditional Loan from a Bank?

A deed of trust grants borrowers and lenders more flexibility. A borrower who can’t show proof of a steady income or has a bumpy credit history can secure a loan from someone they know. They can negotiate interest rates, make higher down payments, and have shorter payback periods compared to traditional loans.

Is a Deed of Trust Risky for a Lender?

While a deed of trust can let a lender earn competitive interest on their excess capital while having peace of mind with a legally binding agreement, a deed of trust can come with some risk. Although the property secures the loan, the foreclosure sale may not produce enough money to cover the cost of the loan.

Can I Transfer a Deed of Trust?

While deed of trust transfers are uncommon, they’re usually permitted in case of a living will proceeding, a divorce, or the death of a property owner. You may initiate this with an assignment agreement. A municipal government or another authority will have to record the transfer, much like they would with a traditional purchase agreement.