What Is an I Owe You (IOU) Agreement?

An I Owe You (IOU) agreement is a written record of a debt that includes the borrower’s intent to repay it. This document details when and how the borrower will pay the debt and provides recourse for non-payment. Generally, an IOU applies to informal loans between family, friends, or trusted borrowers.

It’s recommended to put your IOU in writing, even for small or personal loans. Written agreements carry more weight than verbal ones and serve as clear proof of

- Splitting bills

- Personal loans

- Advance payment

- Borrowing personal property

Use Legal Templates’ free I Owe You template to get your loan details in writing and set expectations for repayment.

IOU Vs. Promissory Note vs. Loan Agreement

An IOU, a promissory note, and a loan agreement all document loans or repayments. These agreements each include specific conditions and serve slightly different purposes for borrowers and lenders. Consider the use and details of each document with the information in the table below.

| Aspect | IOU | Promissory Note | Loan Agreement |

|---|---|---|---|

| Complexity | Most informal and least complex | More formal and complex than IOU. Less formal and complex than loan agreement. | Most formal and complex of the three |

| Content | Includes amount owed and borrower's signature. May have more depending on the parties' attention to detail. | Includes the borrowed sum, interest rate, repayment date, and borrower's signature | The details in a promissory note and information about collateral (if applicable), default terms, and legal provisions |

| Legal Enforceability | Most challenging to enforce in court because of its ambiguity | Typically enforceable in court | Easiest to enforce in court because of its detailed nature |

| Use Cases | Most commonly used when loaning small sums to family and friends | Individuals commonly use this document for business or personal loans. | Individuals and businesses use this document for mortgages or complex loans involving larger sums of money |

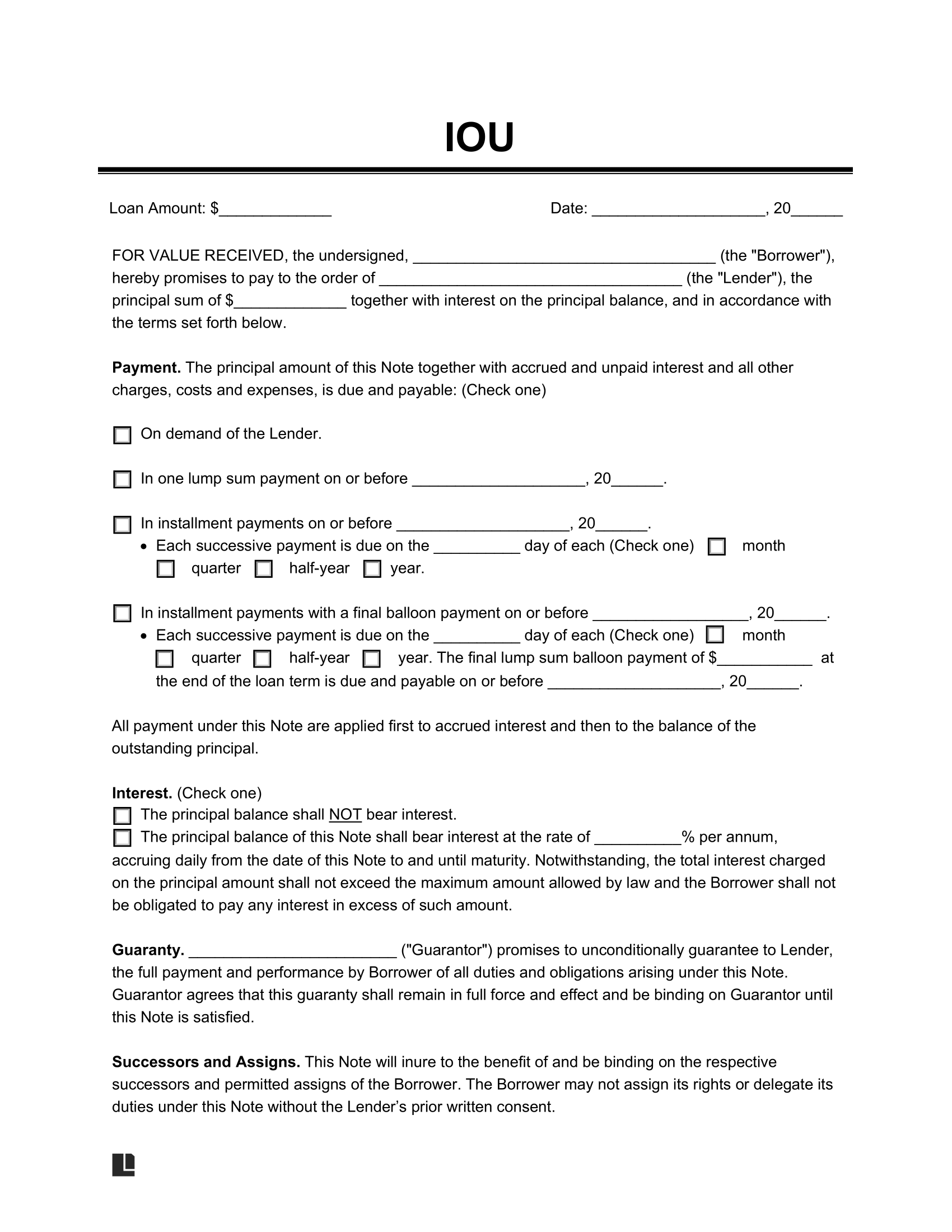

How to Write an IOU Agreement

While an I Owe You serves as an informal document, it’s essential to include all relevant information and follow proper formatting. Creating an agreement with clear terms ensures everyone understands their obligations. Write an effective IOU agreement with the following steps and information.

1. Identify the Parties Involved

Name the borrower and lender involved in the agreement. You may also include a cosigner or guarantor to take responsibility if the primary lender fails to pay. Record every party’s full name and clearly identify their role.

2. Record the Loan and Payment Methods

Write down the details of the loan and the approved repayment methods. Include the full principal amount owed. For the payment, select whether it will be paid back using the following methods:

- Installments: The borrower repays the lender through a set number of consistent installments over the pre-determined period.

- Installments with a final balloon payment: The debt is paid via installments with a larger sum due on the final payment date.

- Due date: For loans paid back all at once, set a due date for the full repayment.

- On demand: If payment terms include on-demand repayment, the lender can ask for the entire sum paid at any time, and the borrower pays upon request.

3. Add Interest Rates

If the lender wants to charge interest on the loan, include the amounts and terms in the document. Clearly state the interest rate and any terms for payments. Also, check state usury laws to find the maximum interest rate legally permitted in your state.

4. Set the Governing State

Determine which state laws will govern your agreement, including setting the maximum for interest and overseeing disputes. Typically, the lender or borrower’s state of residence acts as the governing state for the agreement.

5. Sign and Date

The lender, borrower, and other parties should sign and date the agreement. For extra protection or proof of validity, consider getting a notary acknowledgment. The exact signing and notarization considerations may vary depending on the agreement’s formality or complexity.

Sample I Owe You Agreement

View Legal Templates’ free I Owe You agreement sample for the proper terms, formats, and uses. Use our customizable document, available in PDF and Word format, to make your own IOU.