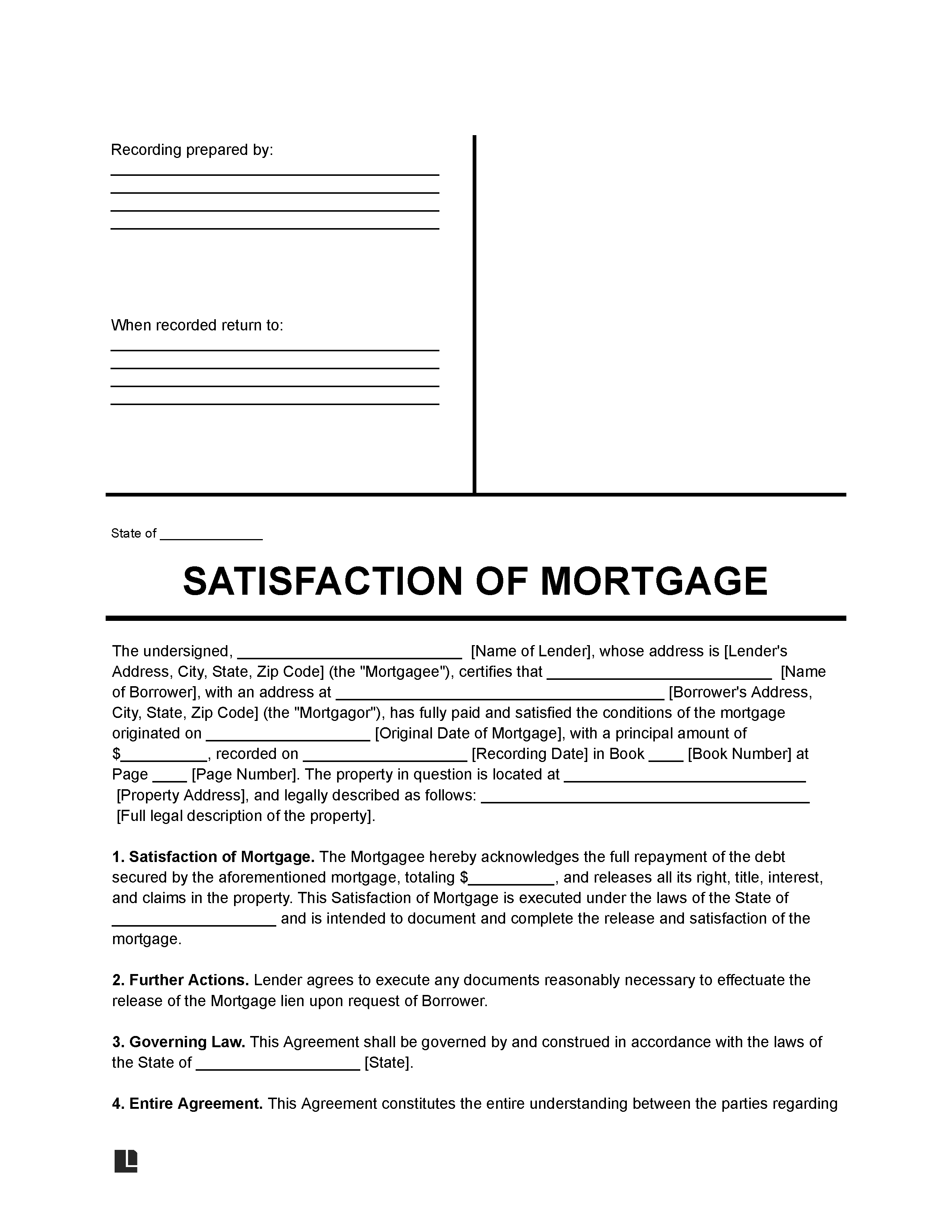

What Is a Satisfaction of Mortgage Form?

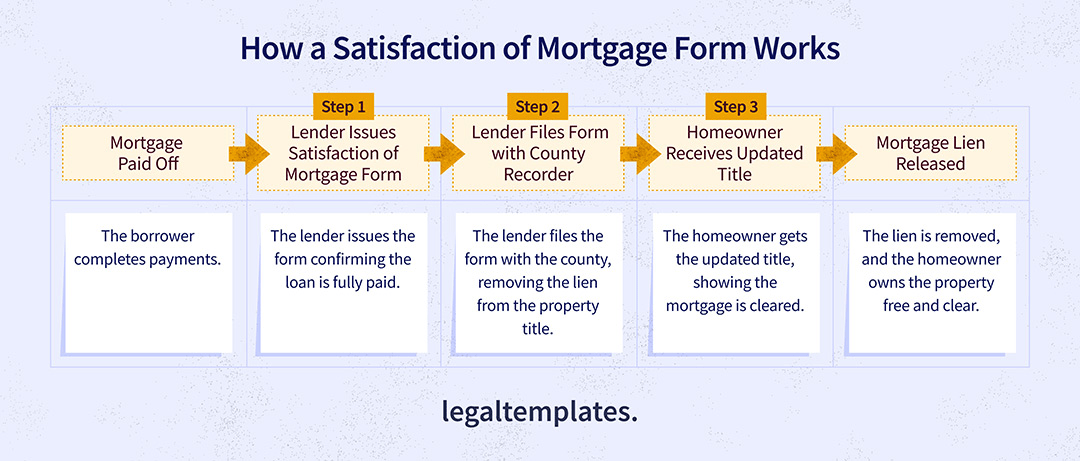

A satisfaction of mortgage form confirms that the borrower has paid off the mortgage on a property. Upon repayment from the borrower, the mortgage lender prepares the satisfaction form. After writing it, they file it for recording in the county where the property lies.

You may also hear this form called a mortgage release form or a mortgage lien release form. Once the satisfaction is properly filed, the lien is removed, resulting in a clear title for the borrower. If the borrower later wants to transfer ownership of the property, they can use a quitclaim deed. A quitclaim deed is useful for quick transfers to family members or trusted individuals.

Legal Templates offers a customizable satisfaction of mortgage form for lenders. You can easily write one for a borrower and meet your legal obligation to report their repayment.

When to Use a Release of Mortgage Form

In some states, the lender needs to complete a release of mortgage form to satisfy legal requirements. This requirement is most often in place after full repayment of a mortgage.

Here are some scenarios when the borrower would need a release of mortgage letter:

- After refinancing: When a new loan replaces the old mortgage, the previous financial institution must issue a satisfaction to remove their lien.

- When selling a home: If the borrower sells their home and pays off the mortgage at closing, the lender files a satisfaction to make the property free of its lien.

- When transferring a property: If the borrower transfers ownership through inheritance, they must satisfy the mortgage to ensure a clear title.

- When clearing title issues: If there are disputes in property records, a recorded satisfaction helps confirm that the mortgage is fully paid and the lien is removed.

How to Get a Copy of the Satisfaction of Mortgage

Getting a copy of the mortgage satisfaction helps borrowers seek a release of the lien on their property. It starts with the borrower paying off their mortgage plus interest per their mortgage deed with the lender.

Once the lender confirms the final payment, they can fill out the mortgage release form. Our template makes it easy, as lenders can record the details of their specific arrangement. The lender must notarize the form to reduce disputes over the form’s validity.

The lender must file the completed form within 30 to 90 days with the county recorder, county clerk, or land registry office. This step is required to officially recognize the mortgage being removed as a lien. The exact requirements vary by state.

If the lender fails to file in time, they can face penalties or fines. The borrower may also take legal action to clear the lien on their property.

| State | Recording Satisfaction | Penalty |

|---|---|---|

| Alabama | The mortgage is satisfied, and the title passes, once all debts and obligations are cleared, and a written request is served and acknowledged by the mortgagee (§ 35-10-26). | If the mortgagee fails to fulfill the satisfaction request within 30 days, they forfeit $200 to the requester unless there's a pending action contesting the payment (§ 35-10-30). |

| Arizona | Upon satisfaction of a mortgage or deed of trust, the mortgagee or must acknowledge this by delivering or recording a release that includes the docket and page number or recording number (§ 33-707). | Failing to record within 30 days of receiving full satisfaction makes the person liable for actual damages; if they fail to do so within 30 days of a certified mail request, they owe $1,000 plus any actual damages (§ 33-712). |

| Arkansas | Upon full satisfaction of a mortgage, the mortgagee must acknowledge the satisfaction in the public records, releasing the mortgage and revesting the property title to the mortgagor. | If a person receiving satisfaction fails to acknowledge it within 60 days of being requested, they must forfeit a sum up to the mortgage amount, recoverable through civil action (§ 18-40-104). |

Finalizing the Satisfaction of Mortgage

Once the mortgage lien release form is filed, the appropriate office verifies that the document is properly completed, signed, and notarized. If everything looks good, they will record the satisfaction in the public land records. At this point, the lender’s lien will be cleared from the property title.

The office may send the borrower a recorded copy of the satisfaction or notify them that the lien has been removed. Some counties require borrowers to request a copy.

How to Write a Satisfaction of Mortgage Form

You can produce a satisfaction of mortgage form that fulfills legal requirements by following a few basic steps.

1. Record Lender & Borrower Details

Using Legal Templates’s form, you can easily identify each party. Include the names and addresses of both the borrower and the lender. You must also indicate whether the lender is an individual or an entity.

Who is the grantee on a satisfaction of a mortgage?

The grantee on a satisfaction of a mortgage form is the borrower. The grantor is the lender.

2. Add Mortgage Information

Add the mortgage information, including when it was executed and the principal amount. List the recording details, such as the date the mortgage was recorded, the book number, and the page number. Provide the legal description of the property and tax parcel number. Our template provides fields for all this information so you can summarize it on your mortgage lien release form.

3. Specify the Final Mortgage Payment

List the amount the borrower had to pay to satisfy the mortgage. This includes all charges, including the principal amount, fees, interest, and costs. You can input the final amount paid on our mortgage lien release template, and we’ll make it clear that the borrower met their payment obligations.

4. Finalize Details

Fill in the remaining details of the mortgage release document, including:

- what state law applies

- who witnessed the document

- the date of signing

Be sure to identify the person preparing the mortgage payoff statement. This way, the recording office can ask follow-up questions if needed. Also, specify whether the borrower or property owner will receive a copy of the mortgage release letter.

Sample Satisfaction of Mortgage Form

View a free sample of a satisfaction of mortgage form to learn how to structure your lien release document. When you’re ready, you can fill out your own using our satisfaction of mortgage template and download it as a PDF or Word file.

What Happens After Writing a Satisfaction of Mortgage Form?

Once the mortgage debt release form is completed and signed by both parties, it must be legally recorded. Depending on the location, the lender must record the release of mortgage form in the county recorder’s office in the county where the property is located.

While the recording process remains your responsibility as the lender, Legal Templates gives you the tools to prepare. Our form has a blank space at the top, which was created with intention. It allows the office to add its stamp and identify and record the document.

Check your state’s Secretary of State office for property records and learn if the lien release was successful.

What Happens if a Satisfaction of Mortgage Isn’t Filed?

If the mortgage satisfaction letter is not filed, there can be consequences for the lender and the borrower. The lender might face penalties and be liable for damages for not upholding their legal obligation to file the document. The borrower might not be able to prove a clear title, which can stall or delay property sales or transfers.

Is a Satisfaction of Mortgage the Same as a Deed of Reconveyance?

A satisfaction of mortgage and deed of reconveyance both indicate a mortgage has been paid off. Their differences lie in what states use them.

A satisfaction of mortgage is used in lien theory states. In these states, the lender has a lien on the property until the borrower makes the last payment on the mortgage. Then, the lender files a satisfaction of mortgage document to remove the lien.

A deed of reconveyance is used in title theory states. In these states, a trustee holds the property title on the borrower’s behalf. When the borrower pays off the mortgage loan, the trustee issues this deed to transfer ownership back to the borrower.

If the loan was a mortgage, the borrower gets a satisfaction of mortgage. If the loan was a deed of trust, the borrower gets a deed of reconveyance.

Clear a Mortgage by Writing a Satisfaction of Mortgage Today

Legal Templates helps you to save time, money, and stress when you’re ready to complete a lien release certificate. Our platform lets you edit, save, and print the form so it is ready for you to record in the appropriate office. Write your satisfaction of mortgage form in compliance with local requirements today.

Frequently Asked Questions

What does it mean when a mortgage is unsatisfied?

Borrowers who borrow money to purchase property start with unsatisfied mortgages. If the mortgage is unsatisfied, the lender still has a claim to the property. This could be the case if the borrower hasn’t yet paid their mortgage. It can also happen if the borrower has paid their mortgage but the lender hasn’t properly filed a satisfaction of mortgage form.

How much does it cost to record a mortgage release?

The recording fee for mortgage release can vary between states and counties within states. The cost can be as low as $10, but it may be closer to $100, depending on your local office.

What is a partial satisfaction of mortgage?

A partial satisfaction of mortgage acts as an incomplete release. It means that the borrower has paid the mortgage for part of the property but not all of it, so a lien will remain on a portion of the property.

How long does it take to get a satisfaction of mortgage?

The lender must file a release of mortgage letter within a timely manner. Depending on local requirements, they must do it within a certain number of days. It may take between 30 and 90 days to get a final certificate of mortgage satisfaction.

What’s the difference between satisfaction of mortgage and release from mortgage?

Releasing and satisfying a mortgage refer to the same concept. They allude to the process of the borrower paying off their loan and getting the lien removed from their property.