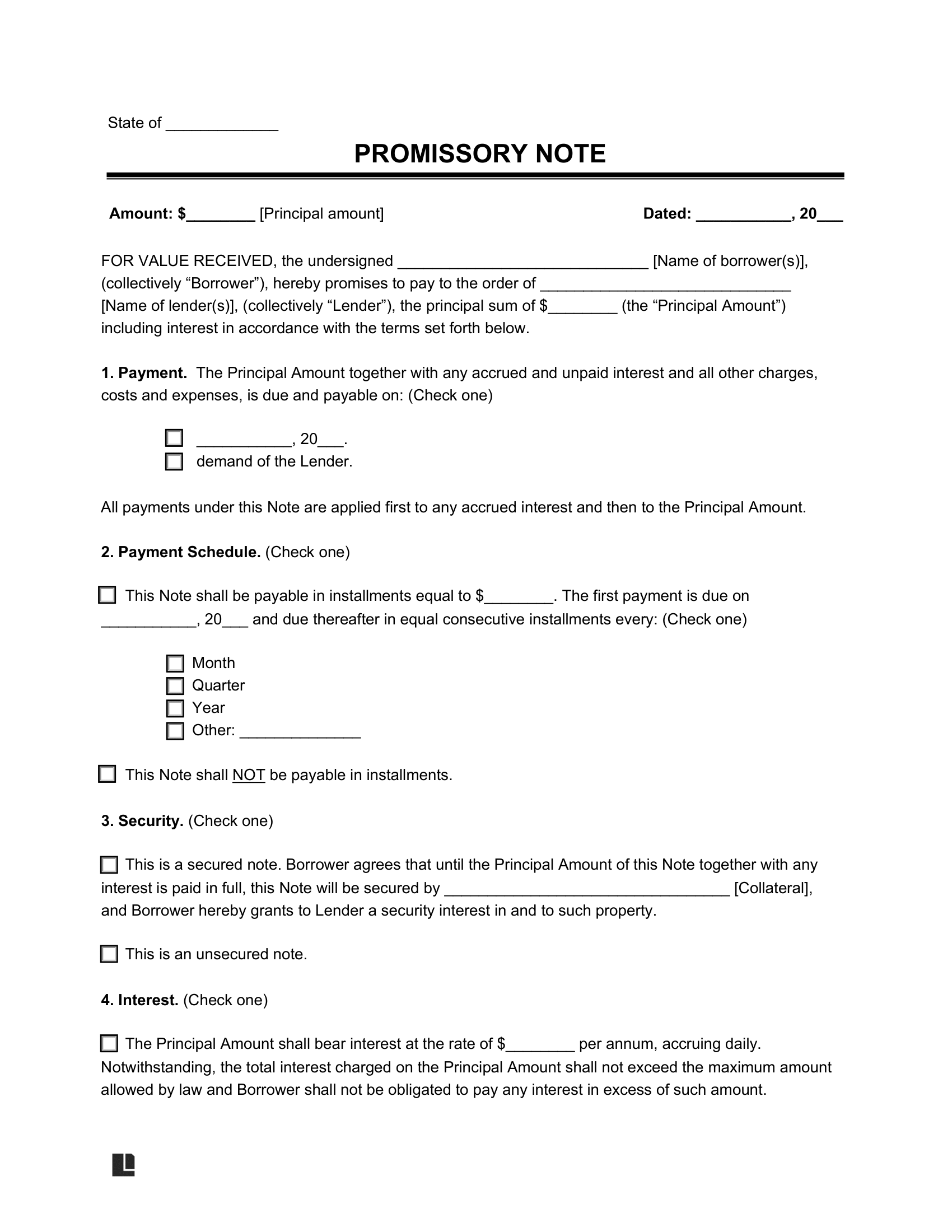

What Is a Promissory Note?

A promissory note is a written agreement where one party promises to repay a loan amount. This promise-to-pay agreement outlines agreed-upon terms, including repayment schedules, interest rates, and penalties. Both parties review and sign it to accept their obligations. Putting the loan terms in writing can help reduce misunderstandings and disputes.

If a promissory note is negotiable, the lender can sell the loan to someone else. Some notes are non-negotiable, meaning the repayment must stay with the original lender and borrower. Decide upfront if you want the note to be transferable and ensure the loan terms allow it.

Promissory notes are ideal for personal loans between people who know each other well. They can also be used for business funding and real estate deals. Use Legal Templates’ promissory note template to create your own in minutes. It provides a clear framework when lending money.

When Should You Use a Promissory Note?

Promissory notes help document loans in various situations. They provide legal protection and peace of mind for both parties. Common uses include:

- Formalizing personal loans: Create clear repayment terms when lending money to friends or family.

- Securing real estate financing: Document private loans or contributions toward a property purchase.

- Funding business growth: Establish repayment plans for startups or equipment purchases.

- Purchasing vehicles or equipment: Ensure clear expectations when financing cars or machinery.

- Covering educational expenses: Set repayment terms for tuition or other training-related costs.

- Managing medical expenses: Provide financial support for treatments with a structured contract.

Pre-Existing Relationships & Promissory Notes

Promissory notes are particularly useful when trust exists between the lender and borrower. However, formal documentation helps protect both parties.

Promissory Notes: By State

Promissory notes must follow different rules depending on your state. Our state-specific guides provide tailored information on local laws. You can learn about interest rate limits and how long you have to collect on a debt. Confidently complete your state-compliant promissory note using our guided form.

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- District of Columbia

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

Promissory Notes: By Type

Secured promissory notes use collateral to reduce risk, while unsecured notes are backed by the borrower’s promise to repay. Use the table below to compare these options and choose the right type for your needs.

| Feature | Secured Promissory Note | Unsecured Promissory Note |

|---|---|---|

| Collateral | Backed by an asset | No collateral required |

| Risk for lender | Lower risk due to presence of collateral | Higher risk due to lack of collateral |

| Interest rates | Tend to be lower | Tend to be higher |

| Common uses | Real estate and business transactions | Smaller personal loans |

Secured Promissory Note

Use this template for high-stakes loans with collateral.

Unsecured Promissory Note

Use this template for quick loans with trustworthy borrowers.

How to Write a Promissory Note

Creating a promissory note is straightforward when you know the key elements to include. Follow these steps to ensure your document is legally enforceable and tailored to your needs.

1. Identify the Parties

List the borrower (the person or entity receiving the loan) and the lender (the provider of the loan). If either party is a business, include the business name and ensure an authorized representative signs the note.

If the lender has concerns about the borrower’s financial stability, they can request a cosigner or a personal guarantee of repayment from a business owner. This person agrees to be responsible for the loan if the borrower defaults.

Assessing the Borrower's Ability to Repay

To assess the borrower’s financial reliability, you can request their credit report with their written permission. Borrowers can access free annual credit reports through websites like AnnualCreditReport.com. If you perform a credit check on a borrower, you must follow the Fair Credit Reporting Act (FCRA). This act requires a permissible purpose and written consent. Some lenders may also request references and proof of employment during this process.

2. Define the Loan Terms

Outline the loan’s details to ensure everyone understands the agreement. Include the following:

- Loan amount: Specify the exact amount the borrower will receive.

- Debt acknowledgment: Include a statement from the borrower recognizing their obligation to repay.

- Repayment schedule: Define how the borrower will pay. They may pay in a lump sum, in installments, or on demand.

- Interest rate: State the percentage rate and confirm it complies with state usury laws.

- Collateral: List any assets that will secure the loan.

- Due date: Include the final date by which the borrower must repay the loan.

- Late payment penalties: Explain the fees for delayed payments.

- Default terms: Record the lender’s rights if the borrower cannot meet their obligations. For example, the lender may require immediate repayment.

- Prepayment terms: Indicate whether the borrower can prepay the loan early. Specify any conditions or penalties for doing so, such as whether there is an interest penalty for paying early.

Write Your Promissory Note With Clarity

Use simple and specific language to avoid misunderstandings and ensure the terms are enforceable.

3. Include Additional Terms

These optional clauses can make your borrow-and-repay contract more comprehensive:

- Amendments: Define how the parties can make changes to the contract.

- Governing law: State which jurisdiction’s laws will apply to the note.

- Prepayment: Specify whether the borrower can repay the loan early without penalties.

- Joint and several liability: State that multiple borrowers will share equal responsibility for repayment (if applicable).

- Right to transfer: Indicate whether the lender can transfer the note to another party.

- Dispute resolution: Determine how disputes regarding the note will be resolved, either by mediation, arbitration, or court involvement.

4. Sign and Distribute the Note

All parties, including any cosigners, should sign the promissory note. Their signatures indicate their agreement to its terms. Notarization isn’t required, but it’s a good idea for larger or more complex loans.

Keep the original note in a lockbox or another safe place. Ensure both parties have copies of the signed note for their records. Store a digital copy in a secure location for easy access.

5. Enforce the Agreement (If Necessary)

If the borrower defaults on the agreement to repay the debt, you can take steps to enforce the promissory note. Start by issuing a demand for payment letter to request payment by a specific date. If the borrower ignores this letter, you can pursue other options, such as:

- filing a case in small claims court

- filing a lawsuit in a higher court (if the loan amount exceeds small claims limits)

- recovering collateral (if the note is secured)

What Makes a Promissory Note Invalid?

A promissory note may be unenforceable if any of these statements are true:

- The note doesn’t include essential details like the loan amount or repayment terms.

- One or both parties signed under duress or coercion.

- The transaction involves illegal activities such as loan sharking or exceeds the state’s maximum interest rate.

- One party forged or altered the note fraudulently.

- The note is for an agreement that is otherwise illegal or against public policy.

6. Release the Borrower

Upon full repayment from the borrower, the lender can release them using a promissory note release. This form acknowledges that the borrower has fulfilled the loan terms. It serves as proof that the debt has been repaid, giving clarity and closure to both parties.

Promissory Note Sample

You can see what a promissory note looks like below by viewing our sample. Create your own using our template and download the final version in PDF or Word format.

Usury Limits by State

Usury laws limit the interest rates lenders can charge. These limits protect borrowers from excessively high costs and promote fair lending practices. They vary by state and depend on the loan type and terms. Charging more than the legal rate can lead to penalties or make the loan unenforceable. Below is a summary of maximum interest rates for private loans by state.

| State | Maximum Annual Rate | Additional Notes | Law |

|---|---|---|---|

| Alabama | 6%; 8% if agreed upon in writing | Excluding loans over $2,000 | AL Code § 8-8-1 |

| Alaska | Federal funds rate + 5%; 10.5% if no contract | Excluding loans over $25,000 | AK Stat § 45.45.010 |

| Arizona | 10%; no limit if agreed and contracted upon | AZ Rev Stat § 44-1201 | |

| Arkansas | Federal discount rate + 5% (capped at 17%) | Capped at 17% | AK Const. Art. XIX § 13 |

| California | 7%; 12% if agreed upon | CA Const. Article XV § 1 and CA Civ Code § 1916.1 | |

What Promissory Notes Are Not

While promissory notes are valuable tools for documenting loan agreements, they have limitations. Here’s what they don’t do:

- They aren’t full loan agreements: Promissory notes focus solely on repayment terms. Loan agreements cover broader details like the loan’s purpose.

- They don’t guarantee repayment: A promissory note creates a legal obligation, but repayment still depends on the borrower’s willingness to pay.

- They aren’t informal IOUs: Unlike IOUs, promissory notes are formal, legally binding documents with specific terms.

- They aren’t for services or goods: Promissory notes are for monetary loans, not bartering or service agreements.