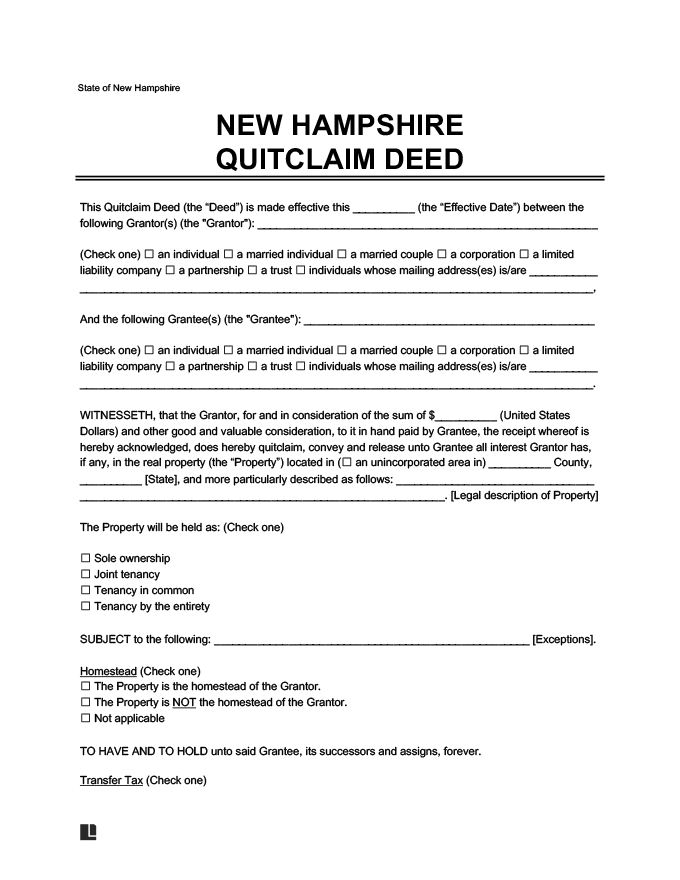

What Is a New Hampshire Quitclaim Deed?

A New Hampshire quitclaim deed (commonly called a release deed in NH) is a document that transfers property without warranties. Unlike a warranty deed, it only transfers the interest that the grantor might have. It doesn’t guarantee that the grantor actually owns the property.

Because of the lack of covenants involved, it’s best to use an NH quitclaim deed for low-risk transfers. For example, family members may use it when transferring property between each other, or a grantor may use it to correct a misspelled name on the original deed. It’s not traditionally used in standard real estate sales.

What to Include in a New Hampshire Quitclaim Deed

NH Rev Stat § 477:28 offers the statutory quitclaim deed form for NH. Buyers and sellers can use this exact form or one “in substance.” Here are the key elements for your NH quitclaim deed form:

- Grantor’s full name, county, and state of residence

- Grantee’s full name and street address

- A statement that consideration was paid (the amount may be stated or referenced and typically includes a nominal amount)

- Clear language stating the grantor “grants” the property with quitclaim covenants

- A legal description of the property or interest being conveyed

- Disclosure of any encumbrances, exceptions, or reservations, if applicable

- A statement releasing homestead and other marital interests

- Signature or acknowledgment by the grantor’s spouse, if required

- The grantor’s signature

NH Rev Stat § 478:4-a offers further guidance for deed requirements, which include the following:

- The latest mailing address of the grantee

- The names of all municipalities in which the property is located (must appear in the first sentence of the first description paragraph)

- The name of each person signing the deed as a party to the transaction (printed or typed under the signature)

New Hampshire Quitclaim Deed Sample

See an example of an NH quitclaim deed form to understand its structure and key elements. Then, use Legal Templates’s guided form to create your own. You can download copies as PDF or Word documents to record and keep for your reference.

Formatting Requirements for a New Hampshire Quitclaim Deed

NH Rev Stat § 478:4-a(II) allows each New Hampshire register of deeds to create and adopt document standards suitable for reproduction. Most counties (like Merrimack County and Strafford County) follow the National Standards for Document Formatting. To meet these standards, your New Hampshire quitclaim deed should:

- Be printed or typed on white 8 ½ in. x 11 in. paper of not less than 20-pound weight.

- Be legible and reproducible.

- Contain all original signatures.

- Be printed on one-sided sheets.

- Not be bound, continuous, stapled, taped, or otherwise affixed.

- Be printed or typed in dark blue or black ink.

- Only use fonts larger than 10-point Times New Roman, except for specified items not in the headings or text of the document.

- Not include stamps that render text illegible or irreproducible.

- Include a margin of at least three inches on the top right half of the first page.

- Include margins of at least one inch on the page sides and bottom and the top of all subsequent pages.

How to File a Quitclaim Deed in New Hampshire

Filing a quitclaim deed in New Hampshire is a simple process if you gather the right information and record the deed correctly. Taking the proper steps protects your interests.

Step 1 – Locate the Original Property Deed

If you are the current property owner, you should have the original property deed in your possession. If you are not the owner, or you have misplaced it, you can request a copy from the county register of deeds where the property is located.

Step 2 – Fill Out the Quitclaim Deed Form

The legal property description should be indicated on the original deed. You can pull this information directly from the original document and transfer it to your quitclaim deed.

Fill out the rest of your NH quitclaim deed using the relevant details. Legal Templates guided questionnaire helps ensure you don’t miss any important information.

Step 3 – Sign and Record

According to NH Rev Stat § 477:3, a quitclaim deed must be signed before a notary public, justice, or commissioner. Wait to sign your quitclaim deed until you are in the presence of one of these individuals. Failure to do so could void the document.

NH Rev Stat § 477:3-a requires real estate conveyances, such as a New Hampshire quitclaim deed, to be officially recorded with the registry of deeds in the property’s county. If the property crosses county lines, you must register the quitclaim deed with each county where the property is located.

Step 4 – Pay Real Estate Transfer Tax

The real estate transfer tax is generally split between the buyer and seller. Both parties must complete and file a Real Estate Transfer Tax Declaration of Consideration form with the New Hampshire Department of Revenue Administration (NH DRA) within 30 days of recording the deed. The buyer’s version of the form is CD-57-P, while the seller’s version is CD-57-S.

The grantee must complete an Inventory of Property Transfer (Form PA-34). This form is due no later than 30 days from the recording date or the date of the transfer, whichever is later. It serves as evidence of payment, per NH Rev Stat § 78-B:3.

How Much Does a Quitclaim Deed in New Hampshire Cost?

When you convey property using a New Hampshire quitclaim deed, you are subject to certain fees and taxes, including recording fees, state taxes, and federal taxes.

1. Recording Fees

Recording fees for filing a quitclaim deed in New Hampshire are established under NH Rev Stat § 478:17-g as follows:

- $10 recording fee for the first recorded page

- $4 fee for each additional recorded page

- $25 fee for recording a deed (the Land and Community Heritage Investment Program (LCHIP) surcharge)

2. Real Estate Transfer Tax

Per NH Rev Stat § 78-B:1, each sale, grant, or transfer of real estate is subject to a real estate transfer tax of $0.75 per $100 or a fraction of the consideration received. If the consideration for the property transfer is $4,000 or less, there is a minimum tax of $20.

Tax should be paid to the registry of deeds office in the county where the property is located. The real estate transfer tax is imposed on both the buyer and the seller, who are required to pay their taxes directly to the registry of deeds.

Exemptions to Transfer Tax

Per NH Rev Stat § 78-B:2, certain real estate transactions are exempt from the New Hampshire real estate transfer tax. Exemptions that could apply to quitclaim deeds include:

- Transfer of title to a state or local governmental agency or district

- Transfer of title to the US or its agencies

- Deeds to correct a previous deed or real estate document

- Transfer of title from a tax-exempt organization to another tax-exempt organization for the purpose of reorganization or internal transfer

- Noncontractual transfers

- Transfers of cemetery plots

- Transfer of property through joint tenancy

- Transfer of property to a beneficiary in a partnership due to the death of a partner

- Transfer of title between spouses due to a divorce decree

If you are not sure whether exemptions apply to your New Hampshire quitclaim deed, consider consulting with a tax professional or real estate attorney before you sign.

Potential Land Use Change Tax (LUCT)

If the property is currently being used as farmland or forest land, it may trigger a 10% Land Use Change Tax on the property’s full value.

3. US Gift Tax

New Hampshire does not charge a gift tax, but the federal government imposes a gift tax on gifts over a certain amount, set by the IRS each year. If the grantor gifts real estate to the grantee through a quitclaim deed, and the value of the property exceeds the federal gift tax exemption, the grantor must fill out Form 709 when they complete their annual income tax return.

Gift tax rates are based on the amount of the gift—in this case, the value of the property conveyed using the quitclaim deed.

4. Capital Gains Tax

While you may owe federal capital gains tax on a real estate transfer through a New Hampshire quitclaim deed, you do not need to worry about state capital gains. The US capital gains tax is calculated based on the amount of time the grantor owned the property before they transferred it and the amount of consideration they received. The IRS also considers your taxable income when determining the capital gains tax rate, exemptions, and deductions.