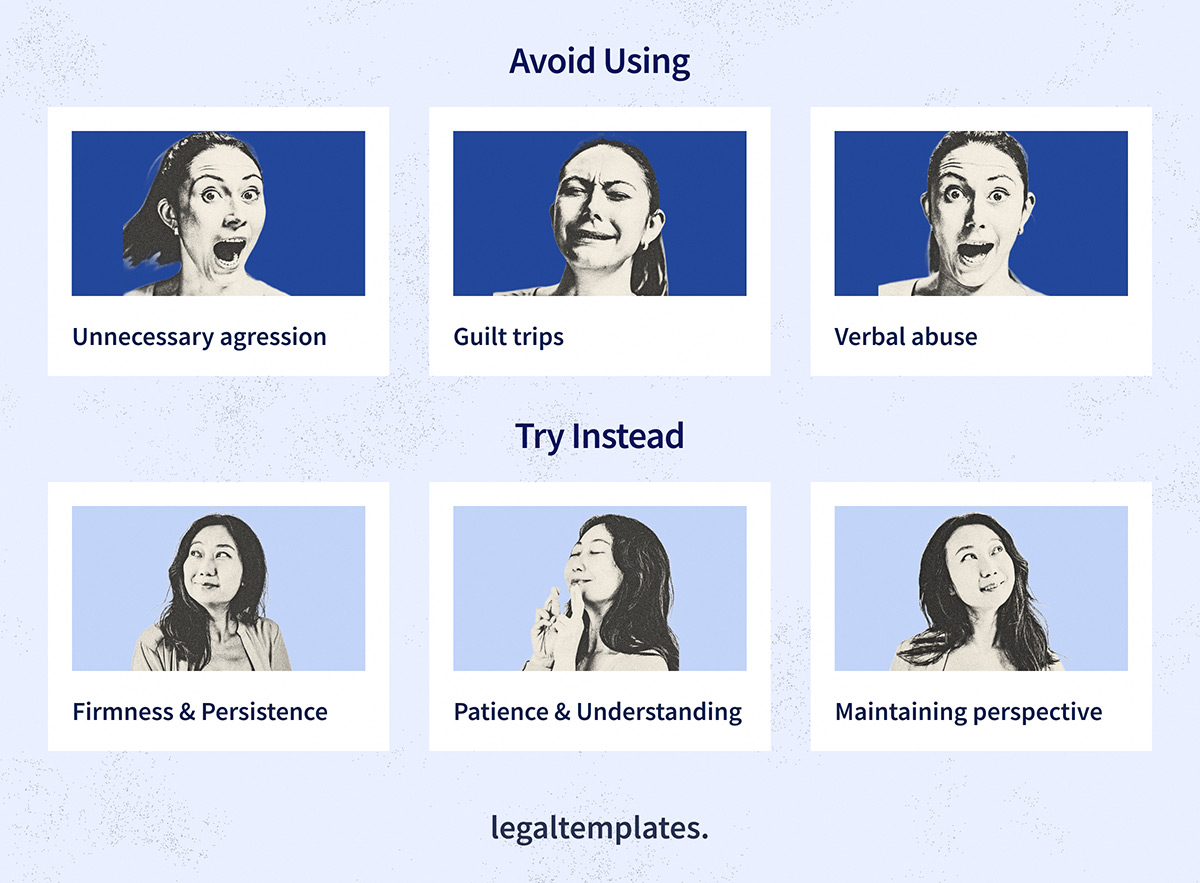

If you’ve lent someone money, they may take their time paying it back or neglect their obligation. You may need to try different strategies and rely on your persistence to get it back.

Getting a personal loan back can be tricky, depending on your circumstances and relationship with the borrower. Read on for tips on how to recover a personal loan without damaging the relationship in the long term.

5 Ways to Get Someone to Pay You Back

When someone owes you money and won’t pay, you can try to get your money back via various methods. Sometimes, the non-paying party might just need a gentle reminder. For more stubborn individuals, you may offer alternative payment options or take more official legal action. Below, you can explore five effective ways to get someone to pay you back.

1. Have a Conversation

Initiate a conversation with the person who owes you money. Approach it gently, first asking about an update on the reason they borrowed the money. For example, ask, “How is your car repair going? Has it been fixed yet?” if they borrowed the money to fix their broken-down car. This provides a way for you to ease into the subject.

Then, you can inquire about repayments. If you’re open to flexibility, ask about their plan to pay you back. Letting them suggest a realistic pay-by date can encourage accountability.

In your discussion, you can mention why you need the money back. Highlighting your financial situation can appeal to their empathy, create a sense of urgency, and potentially hasten their payment.

Give consistent reminders as the days or weeks go on. If more time passes and they continue not to pay, consider implementing a strict deadline. If you inform the borrower that their payment is due in two weeks or you’ll take further action, they may have a more tangible reason to pay.

Lending to Friends & Family?

If you’re lending to friends and family, read our guide on family loan agreements to learn how to navigate these unique loan arrangements.

2. Offer a Payment Plan

The non-payer may be able to pay back their debt in installments instead of all at once. In this case, you can set up a payment plan agreement with them. Meeting in the middle ground means both parties achieve some progress: you get some of the money back, and they gradually alleviate their debt burden.

For example, imagine that the indebted person owes you $500. You can write a payment plan that obligates them to pay you $50 every two weeks for five months. They can make these smaller payments over time and eventually pay off their debt. This agreement keeps them accountable and makes the payoff arrangement more manageable.

3. Accept Other Forms of Payment

If you’re at a loss for what to do when someone owes you money, you may consider more creative alternatives. They may not be paying you back because they don’t have the funds readily available. In this case, you can accept other forms of payment. For example, you may:

- Accept personal items: They may give you a vehicle, a piece of equipment, or another item roughly equivalent to the dollar amount they owe you. This kind of repayment is called payment in kind (PIK). Ensure that you use a bill of sale to transfer ownership of the item correctly.

- Have them perform a service: If the person who owes you money is skilled in a trade, you may have them perform a service for you. Whether you need a room in your house painted or furniture moved, their labor can pay off their debt. Record the terms of their work with Legal Templates’s service agreement.

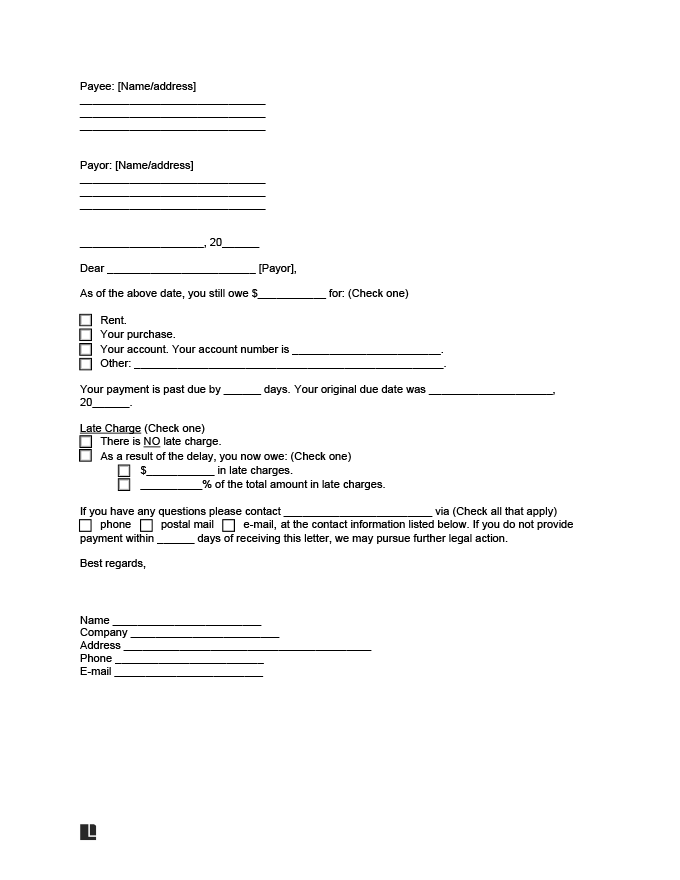

4. Put Your Request in Writing

If your attempts to have a discussion, issue reminders, break up payments over time, or accept alternative methods are futile, you may resort to a more formal process.

Put your request in writing by creating a demand for payment letter. Summarize the details of the unpaid debt and state that you will pursue further legal action if the recipient doesn’t pay on time. Add any information about late charges if applicable and put a final deadline for payment in your letter. You can write yours from scratch, but it’s best to use a pre-made form like Legal Templates’s so you don’t leave out any key details.

5. Consider Legal Action

If none of the steps above work, you may pursue legal action. Before seeking legal action, think about whether the amount of money you’re owed is worth jeopardizing your relationship with the person. Also, consider the costs that may come with this route. If the amount is negligible, consider refraining from legal action, and try to get your money back via the four previous steps.

If the amount is significant and you feel like you’ve exhausted your options, you can first try mediation. Mediation has you and the party who owes you money go before a mediator. The mediator is a neutral third party who facilitates communication and helps you both come to a mutually acceptable resolution.

Mediation doesn’t always result in an outcome. You may consider arbitration instead (which requires an arbitration agreement) to reach an enforceable resolution without going to court.

Your resort will likely be going to small claims court. Each state has different thresholds for small claims court, so check the limit in your jurisdiction. You may have to pay additional filing fees for claims under certain dollar amounts, so consider these when deciding if it’s worth bringing your case to small claims court. You must also ensure you have a solid case and can prove that the money given was truly a loan and not a gift.

Can You Go to the Police if Someone Owes You Money?

In most cases, instances of owed money are civil matters, not criminal ones. If you go to the police because someone owes you money, they’ll likely direct you to legal options like small claims court. The police will only get involved if the situation involves violence, theft, or fraud.

How to Safeguard Yourself When Lending Money

No matter how well you know the person you’re lending money to, the act comes with inherent risk. Here are some tips to protect yourself when lending money:

- Be okay with not getting paid back: Set an expectation for yourself—you may not get back any money you lend. Because of this truth, be sure only to lend money that you’re okay with losing.

- Get everything in writing: Whenever you loan money, get it in writing. Depending on the formality and terms you want to include, consider an IOU template, promissory note, or loan agreement. Check your state law to determine whether your agreement needs to be notarized.

- Ask for collateral: Consider only loaning to someone if they provide collateral, which mitigates risk if the borrower fails to repay.

- Don’t lend to repeat nonpayers: If you lent money to someone in the past and they never repaid you, deny their requests for more money. You may also consider limiting the amount you loan to someone who took a long time to repay an initial debt.