What Is a Gift Letter for a Mortgage?

A gift letter for a mortgage is a written statement that confirms that the funds given to a homebuyer are a true gift and not a loan. If a family member or partner helps you pay for your down payment or closing costs, the company financing your home, such as a bank, credit union, or mortgage company, will usually require this letter.

This letter confirms that:

- The funds are a true gift

- No repayment is expected for this amount, now or in the future

- The donor does not have a financial interest in the purchase of the home

According to the Fannie Mae Selling Guide section on Personal Gifts (B3-4.3-04), lenders must verify and document the source of gift funds when reviewing your mortgage application to make sure they aren’t undisclosed loans. A mortgage gift letter helps your lender see that the funds used to buy your home are truly a gift and not additional debt.

Who Can Provide a Mortgage Gift Letter?

Who can gift your funds may depend on your lender and their requirements. In most cases, the donor must have a close relationship with the borrower, such as:

- Parent(s)

- Grandparent(s)

- Sibling(s)

- Partner(s)

The donor cannot be someone who has a financial interest in the sale. This means that the donor cannot be the seller, builder, or real estate agent. This helps prevent hidden incentives and undisclosed financing.

Is there a Limit on How Much Can Be Gifted?

There is no federal limit on how much someone can gift for a mortgage down payment, though large gifts may have tax-reporting requirements. If the gift exceeds the IRS annual exclusion amount, the donor may need to file Form 709. Filing Form 709 does not always mean the donor owes tax. It simply reports the gift. The borrower does not pay gift tax.

How to Write a Gift Letter for a Mortgage

A gift letter for a mortgage should include key details about the borrower, the donor, and the source of the funds. It’s also a good idea to check with your lender if they have any specific requirements. Follow the step-by-step guide below to create a mortgage gift letter that lenders can easily review and accept.

Step 1 – State that the Funds Are a True Gift

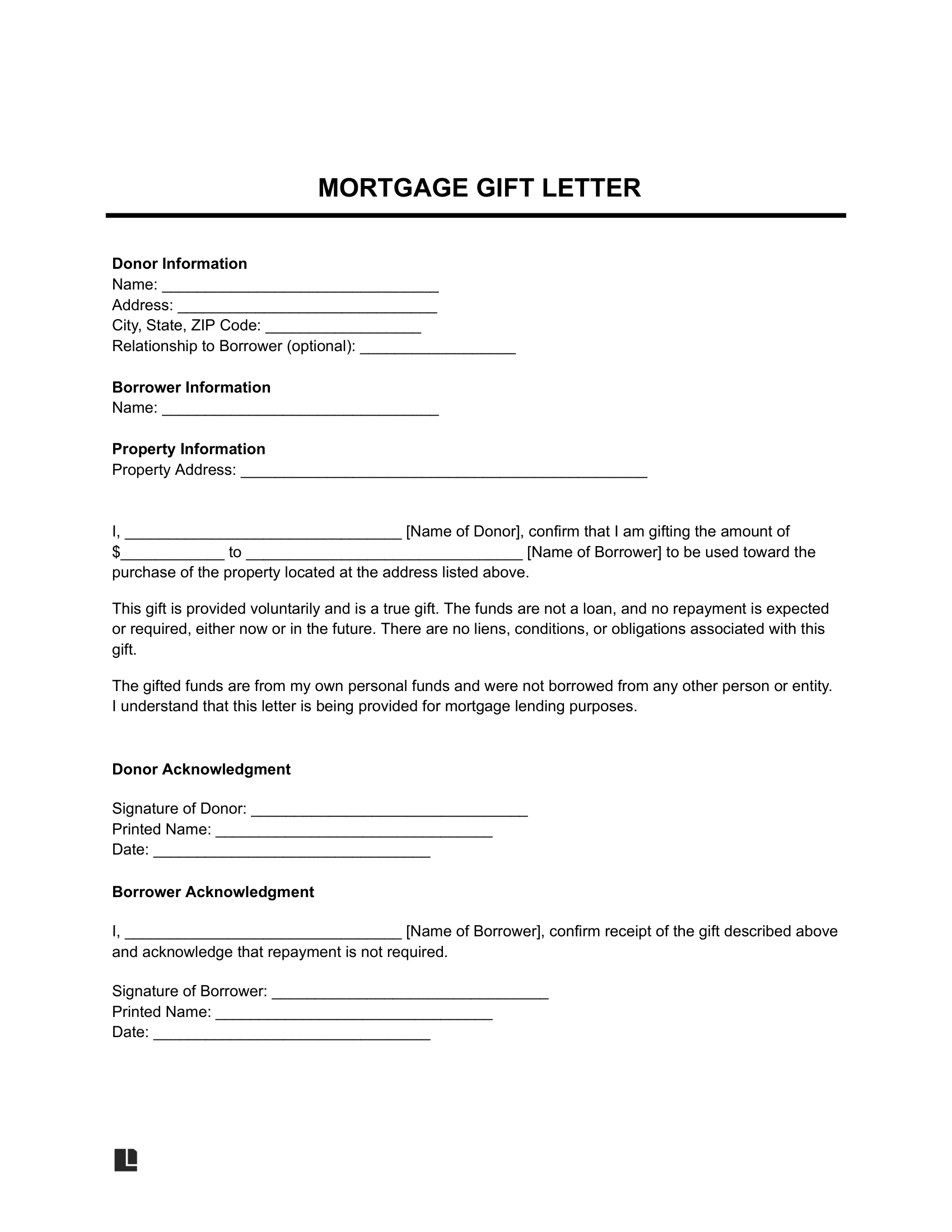

Begin your letter by clearly stating that the money is a gift. In your letter, confirm that the funds were given voluntarily and that no repayment is expected now or in the near future. This statement should be clear, as this is the most important part of your letter.

A gift letter for a mortgage cannot include repayment. If the money must be paid back in any way, it is not a gift and should not be documented with a gift letter. Instead, you may consider using a promissory note.

Step 2 – Identify the Donor and Borrower

Add the full legal names of both parties. Include the donor’s full legal name and mailing address, and specify their relationship to the borrower. Disclosing your relationship is important, as most lenders require this information to determine eligibility for the gift.

Step 3 – Specify the Gift Amount

Write the exact dollar amount being gifted. Do not estimate the amount or round it off. The amount should match the amount on your bank records or the transfer confirmation your lender will review.

Step 4 – Confirm the Source of Funds

Your gift letter for a mortgage should state that the funds are from the donor’s personal funds and were not borrowed from another person or lender. It should also state that there are no hidden conditions, obligations, or repayment agreements tied to the gift.

Step 5 – Include the Property Address

List the full address of the home being purchased. Make sure it matches the address on your purchase agreement or loan application.

Step 6 – Confirm the Donor Has No Interest in the Sale

Include a statement confirming that the donor is not the seller, builder, or real estate agent, or anyone else who stands to benefit from the sale of this home. This helps show that the money is truly a gift and not a part of the purchase deal.

Step 7 – Sign and Date the Letter

The donor should sign and date the letter. Some lenders may also ask the borrower to sign to confirm the receipt of the gift and acknowledge that repayment is not required.

Step 8 – Add Notary Acknowledgment (If Required)

A gift letter for a mortgage loan does not always need to be notarized. However, some lenders may request notarization. If they do, include a notary acknowledgment and sign the letter in front of a notary public.

Sample Gift Letter for a Mortgage

View a mortgage gift letter template below to see what your completed letter should look like. Then, use Legal Templates’s step-by-step questionnaire to fill out and download yours in PDF or Word format.

How to Submit a Mortgage Gift Letter

After you complete your letter of gift for a mortgage, you can submit it to your lender while they are reviewing your mortgage application. In addition to the letter, your lender may also request proof that the money was transferred, such as:

- A bank statement showing the withdrawal from the donor’s account or the deposit into the borrower’s account.

- A wire transfer confirmation if the funds were sent electronically.

- A copy of the check used for the gift.

Providing complete and correct information can help avoid delays in your mortgage approval process.

You may need a satisfaction of mortgage form to officially show that your home loan has been paid off and remove the lender’s claim from the property record.