What Is a Florida Promissory Note?

A Florida promissory note formalizes the loan arrangement between a lender and borrower, specifying the loan amount, repayment schedule, interest rate, and any applicable late fees. Additionally, clauses covering various conditions of the agreement, such as payment allocation, prepayment options, default interest rates, or acceleration, are typically established.

These documents can be secured or unsecured, with the former involving collateral to secure the loan repayment. While financial institutions may issue promissory notes, they are more frequently utilized for obtaining financing from non-bank lenders. They offer a less formal alternative to traditional loan agreements with fewer provisions and punitive measures for default.

Laws: Promissory notes are subject to state law. Enforcement where real property collateral is not at issue is subject to limitations outlined in Florida Statutes § 95.11. Further restrictions can also be identified in Title XXXIX Chapter 679.

Statute of Limitations: Five years (§ 95-11(2)(b)).

Types of Florida Promissory Notes: Secured vs. Unsecured

Florida promissory notes can be structured as secured, using collateral to reduce risk, or unsecured, relying solely on the borrower’s commitment to repay.

Secured Florida Promissory Note

Involves collateral, providing the lender with the borrower's property in case of default on the loan balance.

Unsecured Florida Promissory Note

Since it lacks collateral, in the event of borrower default, the lender typically resorts to small claims court in order to recover their funds.

Usury Laws and Interest Rates in Florida

Promissory notes must comply with the state’s usury laws as detailed in Chapter 687 of the Florida Statutes.

- With a Contract (§ 687.03(1)): 18%.

- For Loans Over $500,000: Not to exceed 25% per annum (§ 687.03(1) and § 687.071(2)&(3)): Over 25% per annum constitutes a second-degree misdemeanor; over 45% per annum represents a third-degree felony.

- For Judgments (§ 55.03(1)): 4% higher than the federal discount rate.

- For Life Insurance Policy Loans (§ 627.4585(2)): 10% or an adjustable legal maximum as established by the life insurer according to law.

- For Consumer Finance Loan (Up to $25,000) (§ 516.02(2)(a)): 18%.

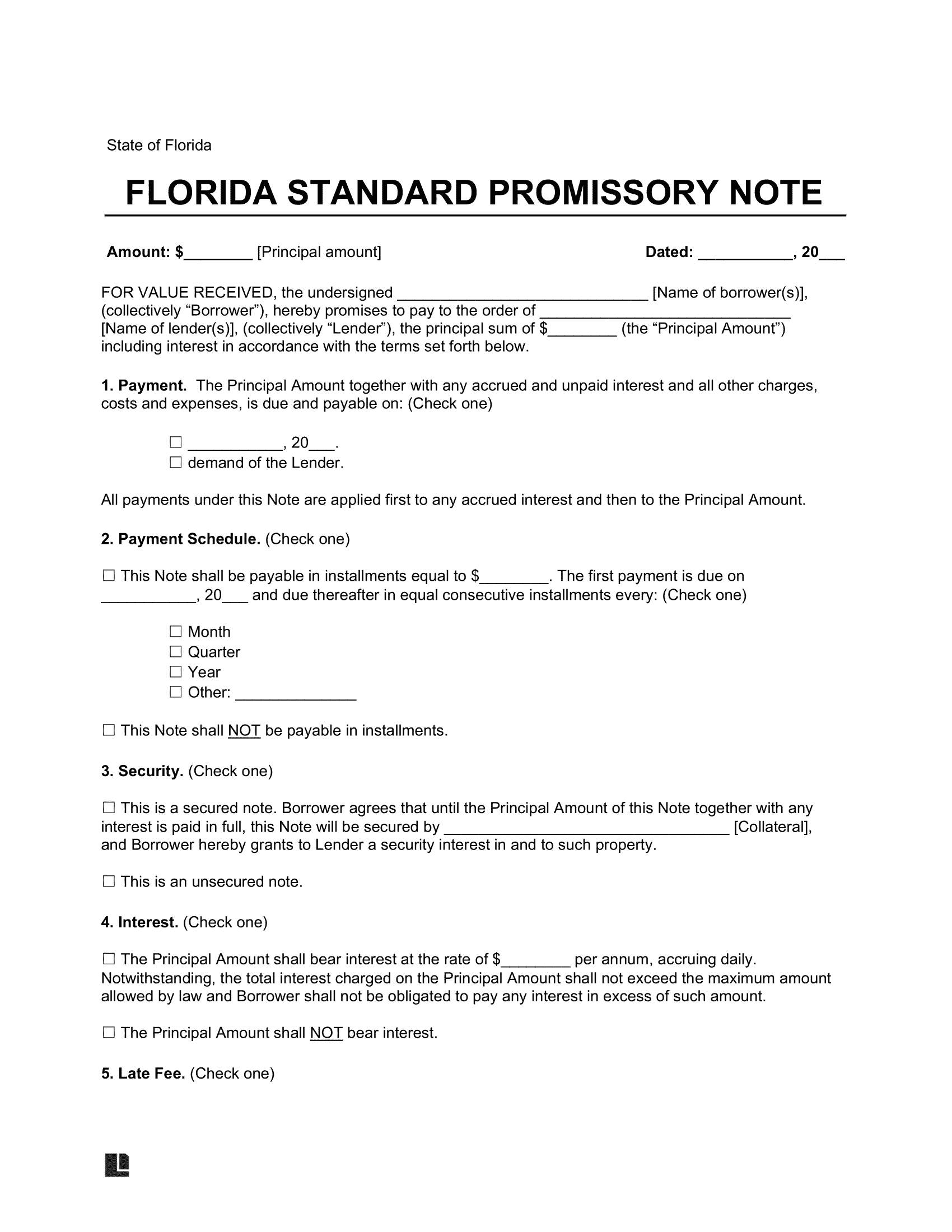

Sample Florida Promissory Note

Below, you can see what a Florida promissory note looks like. You can customize this template using our document editor and then download in PDF or Word format.