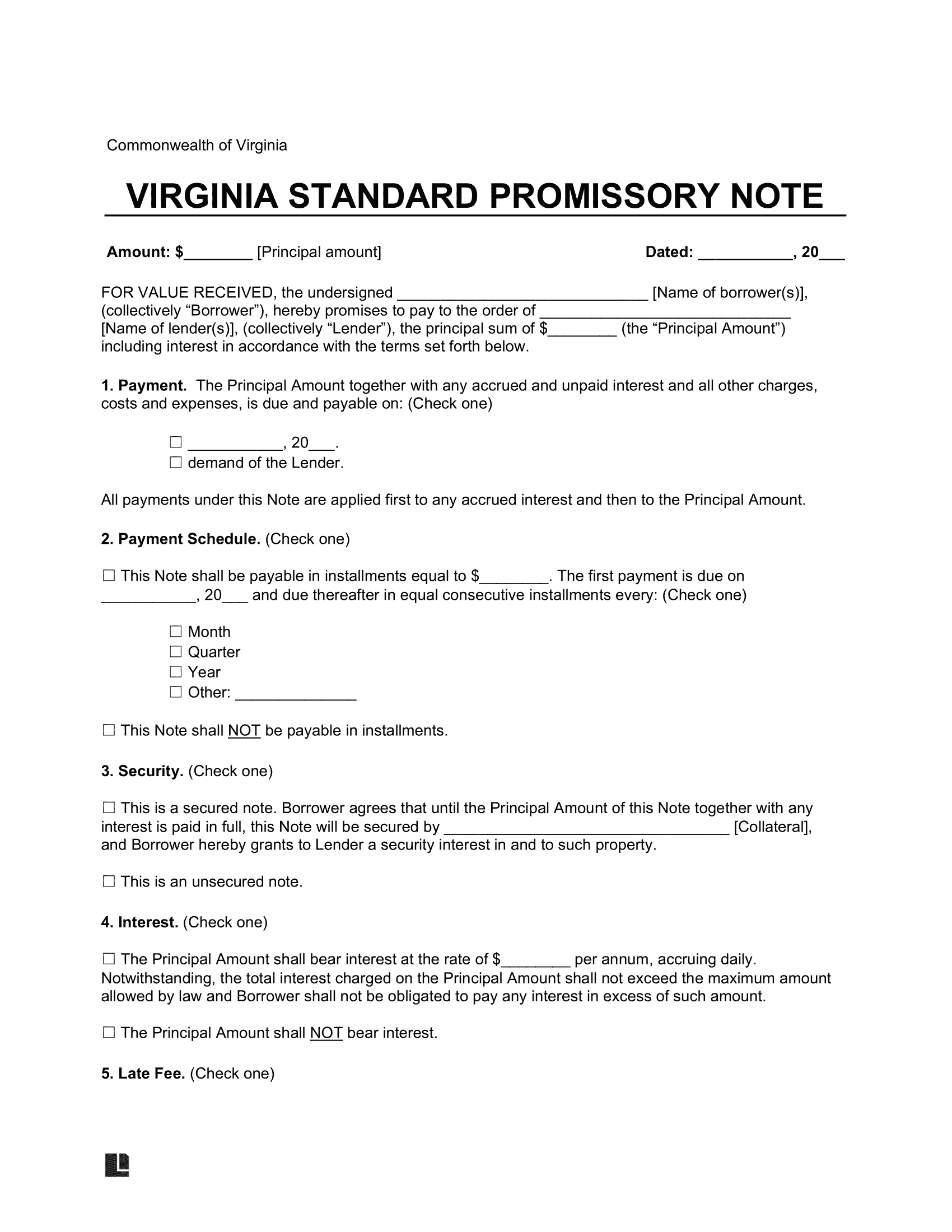

What Is a Virginia Promissory Note?

A Virginia promissory note is a legally binding contract between a borrower and a lender that explains the terms under which the lender will loan the borrower a specified sum. It also describes the interest the borrower is responsible for paying and other repayment conditions they must abide by, like payment due dates and penalties for late payment.

If the lender wants extra security when it comes to receiving the initial loan amount back, plus interest, they may request the borrower to provide collateral. Even without collateral, this document protects both parties’ interests by providing a structured and enforceable framework.

Laws: Title 8.3A of the Virginia Code discusses negotiable instruments, including promissory notes.

Statute of Limitations: Six years (§ 8.3A-118(a)).

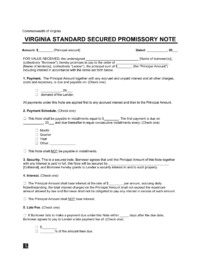

Types of Virginia Promissory Notes: Secured vs. Unsecured

In Virginia, choosing the right promissory note adds structure to your loan. It ensures the agreement is enforceable and tailored to the loan’s value and purpose.

Secured Virginia Promissory Note

Has a borrower provide collateral so they can obtain a loan.

Unsecured Virginia Promissory Note

Issues a collateral-free loan if a borrower can show evidence of high credit or utilize personal connections.

Usury Laws and Interest Rates in Virginia

When you write a promissory note, you must abide by the state’s usury laws present in Title 6.2, Chapter 3 (Interest and Usury):

- With a Contract (§ 6.2-303(A)): 12%; exceptions include consumer finance loans, short-term loans, loans issued by motor vehicle title holders, Virginia Housing Development Authority loans, finance company loans, and loans issued by pawnbrokers (§ 6.2-303(B)).

- In General (Without a Contract) (§ 6.2-301(A)): 6%.

-

For Pawnbrokers (§ 54.1-4008(A)):

- For Loans of More Than $100: 5%/month.

- For Loans of $100 or Less: 7% per month.

- For Loans of $25 or Less: 10% per month.

- For Insurance Premiums (§ 38.2-1806(A)): 1.5% per month.

- With a Bankruptcy Proceeding (§ 6.2-1522): 6%.

- For Third Party Tax Payments (§ 58.1-3018(B)(2)): At an annual rate approved by the local treasurer but not to exceed 16 % per annum.

Sample Virginia Promissory Note

View a free sample Virginia promissory note to learn its format. Create your own using our document editor and download it in PDF or Word format.