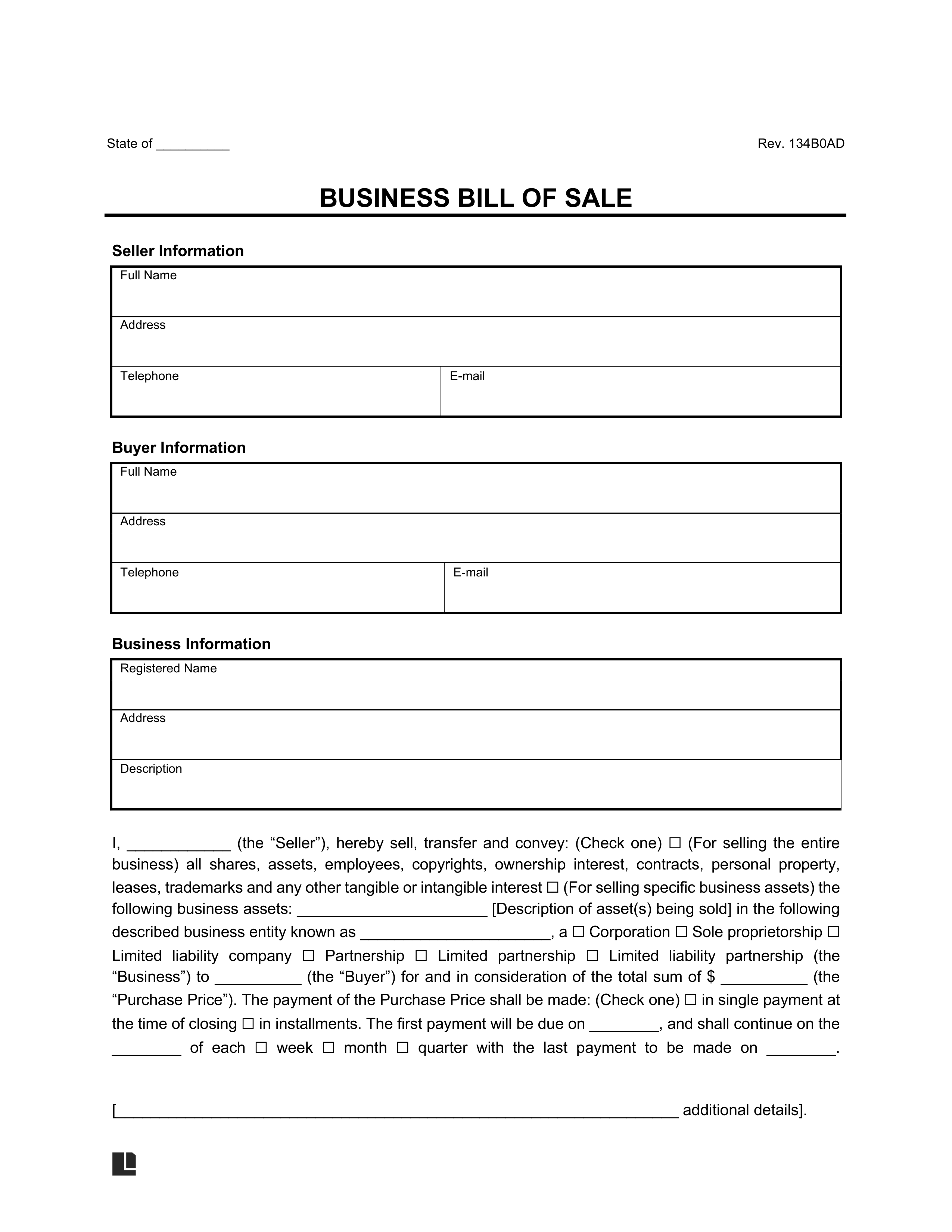

What Is a Business Bill of Sale?

A business bill of sale records the sale or transfer of a business or its assets. It confirms that ownership moved from the seller to the buyer and that payment or other consideration was exchanged. Depending on the deal, the document can be used for different types of transactions, including:

- Entire business sales transfer shares and assets, and the buyer usually takes on existing liabilities.

- Asset-only sales transfer only the listed items, such as equipment or inventory, without transferring the business itself.

For that reason, the bill of sale identifies exactly which assets or ownership interests transferred. It helps clear up questions about what was sold and when payment occurred. Most deals use a bill of sale at closing. The main terms already exist in a purchase agreement. The bill of sale finalizes the transfer of ownership. In simple, low-risk transactions, it can sometimes stand on its own.

Conditional vs. Absolute Bills of Sale

A conditional bill of sale delays ownership transfer until certain conditions are met or uses the sale as security. An absolute bill of sale transfers ownership immediately. Our template creates an absolute business bill of sale.

When to Use a Business Bill of Sale

A business bill of sale works best once the deal is already settled. The parties agree on price and terms and need a final document to complete the transfer. Common situations include:

- Transferring ownership of a small business, especially when the sale is straightforward.

- Transferring business assets only, such as equipment, inventory, intellectual property, or goodwill.

- Closing a transaction where the terms are already set and the bill of sale serves as the final transfer document.

- Simple, unconditional sales that fit an absolute bill of sale, with ownership passing immediately.

- Recordkeeping needs, such as tax filings, licensing updates, or internal business records.

In these cases, a business bill of sale confirms that the transfer happened and provides written proof for future reference.

Other Agreements You Might Need

A business bill of sale does not set deal terms. Other agreements handle that part of the transaction. Which one applies depends on what is being sold:

- Asset purchase agreement covers the purchase of specific personal or business assets.

- Business asset purchase agreement focuses only on business assets, not shares.

- Share purchase agreement transfers company shares and usually includes existing liabilities.

These agreements define the price, representations, and obligations. A business bill of sale then completes the transfer.

Benefits of Using a Business Bill of Sale

- Shows what was sold and the agreed price

- Helps with updates to banks, licensing agencies, and permitting authorities

- Keeps closing simple with an absolute transfer and no conditions to track

- Provides clear proof of ownership change, even when a purchase agreement exists

How to Write a Business Bill of Sale

When selling a business or its assets, a business bill of sale captures the exact details of the transfer at closing. It should leave no doubt about who transferred ownership, what was included, and when the transfer took effect. To do that, the document should clearly cover the following:

- Name the seller by listing the authorized representative and their address.

- Identify the buyer using the buyer’s full legal name and address.

- Describe the business with the registered name, business structure (LLC, corporation, partnership, or sole proprietorship), a brief summary of what the business does, and its physical address.

- Define what transfers by stating whether the sale covers the entire business or only specific assets, such as equipment, inventory, intellectual property, or goodwill.

- Set the sale price by recording the total amount agreed to by both parties.

- Explain how payment works by noting whether the buyer pays in one lump sum or installments (you may want to set out a payment plan), even though ownership transfers on the stated date.

- Address warranties by stating whether the seller provides any business-related warranties or sells the business as is.

- Add deal-specific terms to capture any extra conditions the parties agreed to.

- State the transfer date to show when the business officially changes hands.

- Dispute resolution: state how any disagreements over the sale will be resolved and which state’s laws apply to the transaction

- Include notarization if needed when the document will support banking, licensing, or tax records.

Once signed, the business bill of sale serves as the final record of the transaction. It confirms that ownership changed hands, supports updates with banks and regulators, and gives both parties a clear document to rely on after closing.

Business Bill of Sale Sample

Review a completed business bill of sale to see how the information fits together. You can then customize your own using Legal Templates’s questionnaire and download the finished template in Word or PDF.