What Is a Redemption Agreement?

A redemption agreement, also known as a redemption buy-sell agreement, is a contract that outlines a corporation’s purchase of a departing shareholder’s ownership interest. In this agreement, the business entity itself, not the individual shareholders, buys back stock.

This contract simplifies the transaction, as there is only one buyer (the entity) and one seller (the departing shareholder). This distinguishes it from a cross-purchase buy-sell agreement, in which the remaining shareholders must fund the purchase of the departing shareholder’s interest.

With a stock redemption agreement, the business uses its own assets or financing to complete the payments. The process is usually easier to manage compared to coordinating payments from multiple partners.

Once the sale is complete, the redeemed shares are retired. As a result, the remaining shareholders have a larger portion of ownership.

Benefits of a Redemption Agreement

- Used to manage a shareholder’s interest when they die, retire, or become disabled

- Allows for stock purchases without using personal funds

- Keeps the transaction simple

- Ensures a smooth ownership transition

- Prevents conflicts among shareholders

Key Elements of a Stock Redemption Agreement

A stock redemption agreement makes it clear how and when the corporation will buy back its stock. Here are the key elements to include in your stock redemption agreement to ensure a smooth exit:

- Corporation name. Record the name of your corporation. If you have not yet formed it, you can file your articles of incorporation to legally establish it. You can also write your corporate bylaws to create the entity’s rules.

- Owners. Write the names of all the corporation’s owners and their respective number of ownership interests. Specify the type of ownership interest, such as common stock or preferred stock.

- Valuation of the entity. State the value of the corporation. It should account for the company’s cash flow and goodwill to ensure the payout is fair to the departing shareholder without hurting the business’s financial future.

- Trigger events. State events that will trigger a stock buyback. Examples include a shareholder’s retirement, death, or disability. Unresolvable shareholder conflicts or bankruptcy can also be defined as trigger events.

- Funding methods. Discuss whether the buyback will be funded with cash from a business bank account, life insurance policies, or loans.

- Life insurance policy minimums. Specifying these will ensure that if a shareholder passes away, the corporation has the cash on hand to buy their shares from their family or estate.

- Payment terms. Discuss whether the corporation will pay for the stock via a lump sum or over several years with interest. If needed, you can set up a payment plan agreement to manage the payments.

- Transfer of rights. Confirm that once the buyout occurs, the departing shareholder no longer has the right to claim a share of future profits. Highlight the redistribution of voting power among the remaining corporation shareholders.

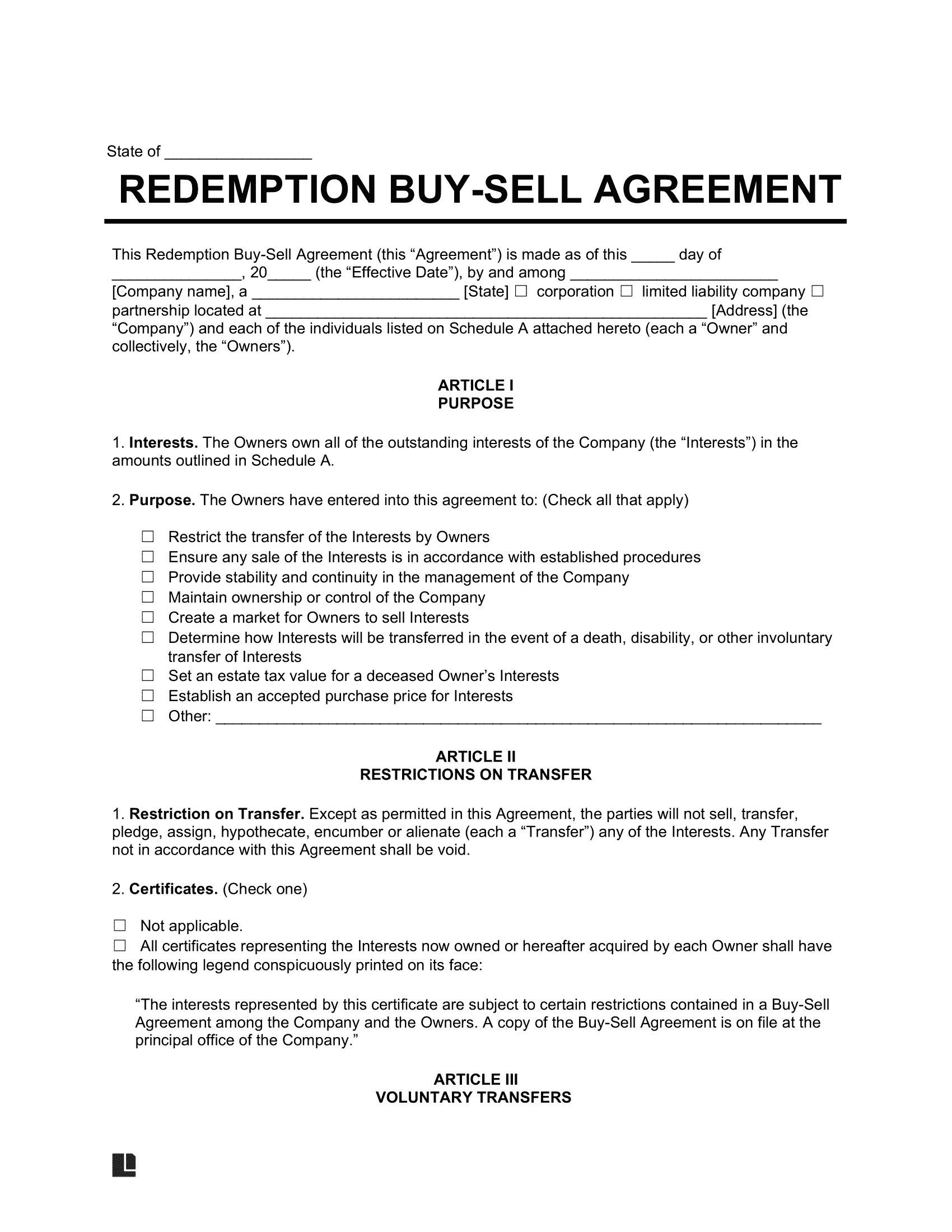

Stock Redemption Agreement Sample

View our simple redemption agreement to explore how to set up an agreement to buy back stock as the corporation. Then, customize your form using Legal Templates’s guided questionnaire. Once you’re done, you can download a copy in PDF or Word format to distribute to the involved parties.

Tax Implications of a Redemption Agreement

When a business buys back stock from a departing shareholder, it changes the tax situation for the remaining owners. Here is what you need to know:

- The shareholders’ investment cost stays the same. When a company buys back stock, the remaining shareholders get an automatic boost in their ownership percentage, but their tax basis stays the same because they didn’t contribute any new capital. Most redemptions are taxed at the lower capital gains rate, but if the IRS thinks the payout looks too much like a profit distribution, they’ll tax it as a dividend (ordinary income), which is more expensive for the shareholder (26 US Code § 302).

- Shareholders may pay higher taxes when they sell shares later. Since the tax basis looks lower to the IRS, shareholders might have to pay more in taxes later. If they sell their shares in the future, the gap between their “low” investment cost and the “high” sale price will be bigger. As a result, they will owe more in capital gains tax than if they had bought the shares themselves.

- Life insurance policies have special rules. If your corporation uses life insurance to fund a shareholder’s exit, the insurance company issues a check directly to your corporation upon a shareholder’s death. Your company receives this money tax-free, so the full amount can be used to buy back the shares. While the payout is tax-free, the premiums that your business pays to keep the insurance active are not tax-deductible.

Always review your situation with a tax professional to avoid surprises and ensure legal compliance.

Considerations for an LLC Redemption Agreement

Redemption agreements are most common among corporations, but LLCs can use them as well. While the goal is the same, LLCs operate under different rules. If your business is an LLC, you must adapt the agreement to fit these specific requirements:

1. Membership Interests vs. Stock

LLCs don’t distribute stock. Instead, they allocate membership interests or units. An LLC redemption agreement must state that the LLC is redeeming percentage interests rather than shares or stock.

2. Operating Agreement Priority

Corporations are heavily regulated by state statutes. Meanwhile, LLCs offer more flexibility, allowing members to govern many aspects of ownership with an operating agreement. You must refer to your LLC’s operating agreement to navigate the redemption buyout process.

If you have not yet officially formed your LLC, you must file the articles of organization with your state’s Secretary of State.

3. Series LLC Specification

If you operate a series LLC, you must specify which series will fund the redemption. If the wrong series funds the purchase, your LLC could lose the liability protection that keeps your various business assets separate. Series LLCs are allowed in the following states:

- Alabama

- Arkansas

- Delaware

- District of Columbia

- Florida

- Illinois

- Indiana

- Iowa

- Kansas

- Minnesota (not explicitly outlined in the statutes, but permitted)

- Missouri

- Montana

- Nevada

- North Dakota

- Ohio

- Oklahoma

- South Dakota

- Tennessee

- Texas

- Utah

- Virginia

- Wisconsin (not explicitly outlined in the statutes, but permitted)

- Wyoming

The Solvency Test

Before a business, whether it operates as an LLC or a corporation, buys back its stock in a redemption agreement, it must pass the solvency test. There are two prongs to this test:

- The business must still be able to pay its regular bills after the buyout.

- The business must still be worth more than its debt obligations after the buyout.

If a business is not able to meet these conditions, the buyout cannot happen. This safeguard protects businesses from running out of money and shields the remaining owners from legal liability.

These rules are outlined in most states’ laws, as most states have adopted a version of the Uniform Limited Liability Company Act (ULLCA) or the Model Business Corporation Act. For example, the laws for LLCs and corporations in Florida are found in FL Stat § 605.0405 and FL Stat § 607.06401, respectively.