Changes for Form 1099-MISC in 2025

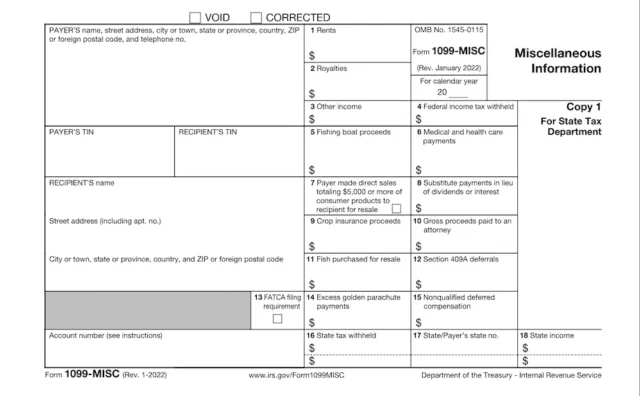

The only change to the 2025 version of Form 1099-MISC is the removal of Box 14, which was previously used to report excess golden parachute payments. Now, Box 14 on Form 1099-MISC is labeled as “Reserved for future use.” You can now report excess golden parachute payments on Box 3 of Form 1099-NEC instead.

What Is Form 1099-MISC?

Form 1099-MISC (Miscellaneous Information) reports payments of $600 or more in miscellaneous income. It also accounts for other miscellaneous income amounts, depending on the category.

The business payer fills out Form 1099-MISC and must send a copy to the recipient by February 2, 2026. The usual due date is January 31, but January 31, 2026, falls on a Saturday, so the deadline is pushed to Monday, February 2.

Exception to the February 2 Due Date

In most cases, the business payer must furnish Form 1099-MISC to the recipient by February 2, 2026. However, if they report amounts in Box 8 (substitute payments in lieu of dividends or interest) or Box 10 (gross proceeds paid to an attorney), the deadline is Wednesday, February 18, 2026.

The business payer must also furnish a copy to the Internal Revenue Service (IRS). If filing by mail, the due date is March 2, 2026. If e-filing, the due date is March 31, 2026.

Since tax year 2020, Form 1099-MISC has not been used to report non-employee compensation. Non-employee compensation, like commissions and other payments for services, is reported on a separate form, Form 1099-NEC.

What If I Need to Report Wages Paid?

Employers use Form W-2, not Form 1099-MISC, to report wages paid.

What Is Form 1099-MISC Used For?

Businesses or individual payers should be aware of the three different types of payments that require a 1099-MISC for each payee:

1. Payments of $600 or More

Form 1099-MISC is used for certain payments that exceed $600. If you pay someone at least $600 for the following payments, you will have to file a 1099-MISC:

- Rents

- Prizes and awards

- Other income payments

- Health care and medical payments

- Crop insurance proceeds

- Cash payments for fish or other aquatic life purchased from anyone engaged in the trade of catching fish

- Cash paid from a notional principal contract to an individual, partnership, or estate

- Payments to an attorney

- Fishing boat proceeds

Form 1099-MISC excludes non-employee compensation like contractor payments.

2. Payments of $10 or More for Royalties and Broker Payments

If you paid someone $10 or more in royalties or broker payments, you’ll need to report it on Form 1099-MISC. But keep in mind, this applies specifically to royalties—such as payments for using intellectual property like books or music—or broker payments that aren’t tied to dividends or tax-exempt interest.

3. Consumer Product Sales

If you sold $5,000 or more in consumer products to a customer, you may need to complete Form 1099-MISC. However, this rule only applies when the buyer intends to resell those products.

For instance, if you supply goods to a retailer or distributor under a buy-sell or deposit-commission arrangement, you must report those transactions on Form 1099-MISC. However, personal purchases or small-scale sales to end consumers don’t fall under this category.

What Payments Are Not Included on Form 1099-MISC?

Some types of compensation might be taxable to the recipient but do not require reporting on Form 1099-MISC. Here are some types of compensation that you can keep off the 1099-MISC form:

- Payments to a corporation (and payments to an LLC that the IRS treats as an S or C corporation)

- Payments for storage, freight, telephone, telegrams, merchandise, and similar items

- Rent payments to intermediaries like property managers or real estate agents

- Cost of current life insurance protection

- Business travel allowances paid to employees

- Payments to tax-exempt organizations

How to Fill Out a 1099-MISC Form

Form 1099-MISC is short and easy to complete when you have the correct information on hand. Before you begin, organize your data on payments made and to whom during the year. Then, you will fill out the relevant information by category:

- Payer details

- Recipient information

- Income types

- Taxes withheld

1. Payer Details

Your business is the payer. From the top left, fill in the business name, complete address, and telephone number.

Next, you will add the business taxpayer identification number (TIN), which should be one of the following:

- Social Security number formatted as xxx-xx-xxxx

- Employer Identification Number (EIN) formatted as xx-xxxxxxx

- Individual TIN formatted as 9xx-xx-xxxx (only if the business is a sole proprietorship using the owner’s SSN)

Familiarize yourself with other fields that relate to your business:

- Box 13: You will add an “X” to Box 13 only if the business is subject to the FATCA filing requirement. Under FATCA, certain foreign financial institutions must provide information about US account holders to the IRS.

- Account number: Add a unique account number in the last box on the left side of the form. You will need an account number if the FATCA box is checked or if you are submitting multiple 1099-MISC forms for the same person.

- 2nd TIN Not.: If the IRS notified you more than once within the last three years that the payee’s TIN is incorrect, add an “X” to this field on Copy A.

2. Recipient Information

The recipient is the person who received the payments reported on the form. Enter the recipient’s TIN, name, street address, city, state or province, country, and ZIP or foreign postal code in the corresponding fields.

Form W-9

Use Form W-9 to collect TINs from individuals you paid.

3. Income Types

You will use Boxes 1 through 3, 5 through 12, and 14 through 15 to report amounts paid by income type. You report amounts only when payments during the year exceed the income thresholds noted above.

- Box 1: Enter the total rent paid to the recipient, including rents for office space, pastures, or equipment, unless paid to an intermediary.

- Box 2: Enter royalties paid to the recipient.

- Box 3: Input other income that does not apply to the other boxes here.

- Box 5: If you operate a fishing boat and share income with the crew, use this box to report each recipient’s portion of the proceeds.

- Box 6: Note the business’s total payments to healthcare providers or suppliers here.

- Box 7: If you sold over $5,000 to an individual for resale under a commission-based arrangement, check Box 7 without including the exact dollar amount.

- Box 8: Enter total payments of $10 or more issued to replace tax-exempt interest or dividends.

- Box 9: Enter crop insurance proceeds, paid from an insurance company to a farmer.

- Box 10: Record gross payments made to an attorney.

- Box 11: Add the total cash payments your business made to the recipient to buy fish for resale.

- Box 12: The IRS does not require you to complete this box for Section 409A deferrals. You may skip it.

- Box 14: Leave this box blank.

- Box 15: Enter nonqualified deferred compensation paid to employees. This should not include amounts reported for prior years on Form 1099-MISC, Form W-2, or Form W-2c.

4. Taxes Withheld

You will report any withholding and related information in Boxes 4 and 16 through 18.

- Box 4: If the business withheld federal taxes from the reported payments, add the withholding amount here.

- Box 16: Enter any state tax withheld from the recipient’s payments in this box.

- Box 17: Add the abbreviated name of the state and your state identification number.

- Box 18: Report the state tax income associated with the payments.

Sample 1099-MISC Form

View our free sample to see what a 1099-MISC form looks like. While you must complete the official Copy A through the IRS’s website, you can complete Copies 1, B, and 2 with Legal Templates’s guided form. When you’re done, they’ll be ready to download as a printable PDF document for distribution.

How to File Form 1099-MISC

All businesses can file Form 1099-MISC electronically. Businesses that file nine or fewer returns annually also have the option to file by mail.

Electronic Filing

You will see that the 1099-MISC form has four copies, beginning with the red version titled Copy A. If you are filing electronically, you can skip Copy A. Filing online produces a readable version for the IRS. However, you will need the following copies:

- Copy 1: For the recipient’s state tax department (when required).

- Copy B: For the recipient’s records.

- Copy 2: For the recipient so they can file it with their state income tax return (when required).

Send copies to the recipients by March 2, 2026, and e-file your returns by March 31, 2026.

Paper Filing

To send in paper filings, you must obtain official printed red copies of the 1099-MISC directly from the IRS. You also need special software to complete them. These official red versions of the form are scannable by the IRS. If you print a red version of the form and complete it manually, the IRS scanning technology cannot read the information.

After you complete the official version (Copy A) properly, you must send it to the address below based on where you live:

| If Your Legal Residence or Principal Place of Business Is In: | Use the Following Address: |

|---|---|

| Alabama, Arizona, Arkansas, Delaware, Florida, Georgia, Kentucky, Maine, Massachusetts, Mississippi, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Ohio, Texas, Vermont, Virginia | Internal Revenue Service Austin Submission Processing Center P.O. Box 149213 Austin, TX 78714 |

| Alaska, Colorado, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Montana, Nebraska, Nevada, North Dakota, Oklahoma, Oregon, South Carolina, South Dakota, Tennessee, Utah, Washington, Wisconsin, Wyoming | Department of the Treasury IRS Submission Processing Center P.O. Box 219256 Kansas City, MO 64121-9256 |

| California, Connecticut, District of Columbia, Louisiana, Maryland, Pennsylvania, Rhode Island, West Virginia | Department of the Treasury IRS Submission Processing Center 1973 North Rulon White Blvd. Ogden, UT 84201 |

| If your legal residence or principal place of business, or principal office or agency, is outside the United States, use the following address. | Internal Revenue Service Austin Submission Processing Center P.O. Box 149213 Austin, TX 78714 |

Once you send Copy A to the IRS, you must print and fill in Copies 1, B, and 2 by hand. Distribute Copies B and 2 to recipients by February 2, 2026. Send Copy 1 to the recipient’s state tax department before the locally established date.

Ensure that you mail Copy A to the IRS by March 2, 2026. Include Form 1096, Annual Summary and Transmittal of US Information Returns, with your mailed 1099-MISC forms.

Penalties for Failing to File Form 1099-MISC

Failure to file any information return, including a 1099-MISC, can result in financial penalties. The penalty amount depends on how late the return is:

- $60 per 1099-MISC if you file less than 30 days late

- $130 per 1099-MISC if you file more than 30 days late but before August 1, 2026

- $340 per 1099-MISC if you file after August 1, 2026

- $680 if you intentionally disregard the filing obligation

Small businesses, which are businesses that made an average of $5 million or less over the past three years, have smaller maximum penalties than large businesses that made an average of more than $5 million over the past three years.

Fine limits only apply to late filings. Intentional filing disregards have no maximum penalties for small or large businesses.