What Is an Irrevocable Trust?

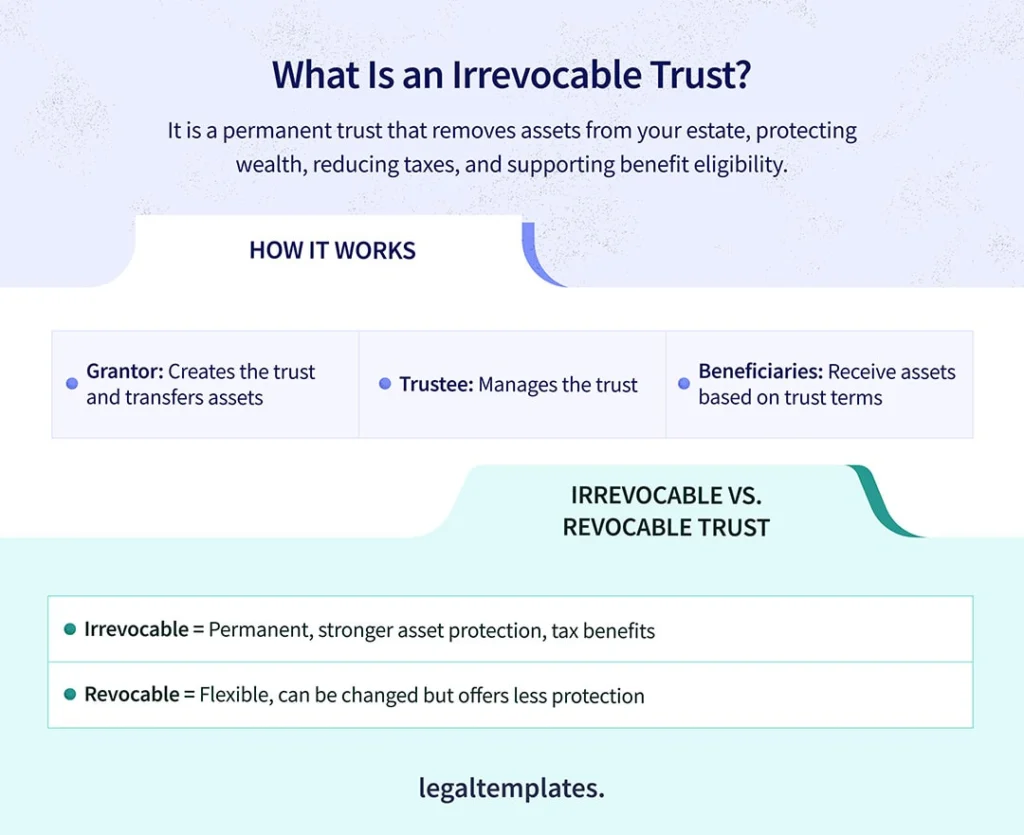

An irrevocable trust (or irrevocable living trust) is a permanent solution for holding assets outside of the grantor’s estate. The grantor, or the creator of the trust, decides which assets will go into it. They can include real estate, business interests, investment assets, cash, and life insurance policies.

Once a grantor creates an irrevocable trust, they cannot change or cancel it. Special circumstances may allow for amendments or revocation, but this type of trust is designed to remain effective until specified conditions are met.

How Does an Irrevocable Living Trust Work?

To create an irrevocable trust, the grantor nominates two parties: a trustee and a beneficiary.

The trustee manages the trust fund, so they decide what happens to the property in it. Ideally, the grantor should choose a third-party trustee who will uphold fiduciary duty and act in the beneficiaries’ best interest.

The beneficiary receives the property in the irrevocable trust. Depending on the trust’s terms, they may access the property when the grantor dies or certain conditions are met, such as the beneficiary turning a certain age.

Once you create an irrevocable trust, it’s unchangeable unless you get approval from the beneficiaries.

Who Needs an Irrevocable Trust?

Anyone can create an irrevocable trust with Legal Templates, but it can be particularly helpful to people looking to meet these goals:

- Protect assets from lawsuits: Putting assets in an irrevocable trust can make it difficult for plaintiffs to seize them in legal proceedings.

- Shield assets from creditors: Creditors may have trouble seeking payment for outstanding debts if some assets are outside of the grantor’s estate.

- Lower estate taxes: When assets go into an irrevocable trust, you can lower the value of your estate and potentially reduce tax liabilities.

- Qualify for benefits: You can use an irrevocable trust to reduce your countable assets and qualify for Medicaid and other government benefits.

- Pass wealth to children: An irrevocable trust can delay the transfer of wealth to children, which is helpful if you think they need to first learn bout financial literacy before managing assets on their own.

- Transfer wealth to special needs family: You can transfer wealth to a family member with special needs without making them ineligible for government benefits.

Irrevocable Trust vs. Revocable Living Trust

You can amend or repeal a revocable living trust during your lifetime whenever you’d like, but you cannot amend or repeal an irrevocable living trust without the beneficiaries’ approval or a court order.

When the grantor passes away, a revocable living trust typically converts to an irrevocable one. At this point, the assets follow the distribution outlined in the trust document.

Amending a Trust

If you write a revocable living trust and need to make a change, you can use a trust amendment form.

What Are the Tax Considerations for Irrevocable Trusts?

The IRS introduced a law (Rev. Rul. 2023-2) that says when someone passes away, assets in an irrevocable trust won’t get a “step-up” in value for tax purposes.

Before this rule, assets in an irrevocable trust would get a step up. This means that if a grantor put an item worth $100,000 into their trust and passed away when the item was worth $150,000, the beneficiary would inherit the property valued at $150,000 for tax purposes. If the beneficiary sold it for $160,000, they would only have to pay taxes on $10,000, not $60,000.

Now, the step-up rule doesn’t apply to irrevocable trusts. The assets will only get a step up in value for tax purposes if they are part of the grantor’s taxable estate.

As a result, beneficiaries might have to pay more taxes if the assets in an irrevocable trust appreciate. This is because they won’t get the “stepped-up” value. When planning your estate, you may consider rethinking how to use an irrevocable trust to ensure your beneficiaries avoid higher taxes. Consult a lawyer for the best approach for your situation.

What Are the Types of Irrevocable Trusts?

Irrevocable trusts are useful legacy planning tools that let you transfer assets while accessing specific benefits, such as tax savings, asset protection, or charitable contributions.

Depending on your personal goals and financial situation, different types of irrevocable trusts can help you achieve these objectives. Below are some of the most common types of irrevocable trusts, each serving a unique purpose:

- Charitable trust: Benefits charitable organizations while providing tax deductions.

- Medicaid trust: Protects assets for Medicaid eligibility by transferring ownership.

- Qualified personal residence trust (QPRT): Allows transfer of a personal residence, reducing estate taxes.

- Asset protection trust: Shields assets from creditors and lawsuits.

- Grantor-retained annuity trust (GRAT): Transfers assets to beneficiaries but lets the grantor receive regular payments from the trust for a set period.

- Irrevocable life insurance trusts (ILIT): Holds life insurance policies outside of the taxable estate.

Different Types of Trusts

Read more about different types of trusts, including irrevocable and revocable, to find one that meets your needs.

How to Write an Irrevocable Trust Form

Writing a legally sound irrevocable trust form without an attorney can be relatively simple, especially when you use Legal Templates’s form to help you through the process. Below, we explore the steps in writing an irrevocable trust form so you can take certain assets out of your taxable estate and set up your beneficiaries for financial success.

1. Enter Grantor Information

Begin by entering your information as the grantor, including your name and address. You’ll want to specify whether you’re the sole grantor or if you’ll have someone else as a co-grantor. When you use our template, you can choose whether the grantor is just you, a married couple, or an unmarried couple.

This distinction helps when it comes to joint estate planning. For example, a married couple or business partners may transfer assets into one trust to achieve shared goals, like asset protection or tax reduction. Family members may also want to pool their assets to help secure future generations’ finances.

2. Describe the Trust’s Purpose

Irrevocable living trusts can have different purposes depending on your situation, so be sure to clearly state yours. You can choose from pre-written options in our template for simplicity, such as managing the grantor’s assets or distributing the assets upon the grantor’s death. If you want to be more specific, you can write in your own purpose with more details.

3. Name the Trustee

Name someone you trust to watch out for the beneficiaries’ best interests as your trustee. While you can name yourself, you may lose some of the tax advantages that come with an irrevocable trust.

List all the powers the trustee will have and note any exclusions. If you aren’t sure which powers to award or limit, you can look through our template for pre-written options, like selling the property in the trust or exercising stock voting rights. These powers are common for trustees to have, but you can choose to award them all or narrow them down to meet your needs.

When sorting the trustee’s details, you can also record whether they will receive compensation. It can be a pre-set amount, or it can be a “reasonable” amount based on the degree of management work they do before the trust’s assets go to the beneficiaries.

4. List the Trust’s Property

All of your property likely won’t go into an irrevocable trust, so it’s essential you specify which assets you’re giving up. This way, you can maintain a clear distinction between your taxable estate and the assets that go into your trust for beneficiaries’ future use.

5. Designate Beneficiaries

Name general beneficiaries, who are the parties that will receive the assets in your irrevocable trust. If you have more than one beneficiary, designate the percentage of the trust each will receive.

Note that they may not receive all assets, as you can choose to gift some to other parties.

6. Make Specific Gifts

Gift designations are separate from your beneficiaries. If you want a specific organization or cause to get an asset from your irrevocable trust, you can name the entity and describe the item it will get. If you have pets, you can also decide that a certain dollar amount will go toward their care.

If you want to give a vehicle as a gift but don’t want to use a trust, you can use a gifted car bill of sale to prove you don’t expect anything in return.

7. Account for Children

If you have children, you can account for them in our template. Select that you have children and declare you will include a subtrust for them if desired. A subtrust receives funding from the main trust, and the assets only go to the children when they reach a certain age or milestone, like turning 30 or graduating from college.

Ensure you also prepare for your children’s future by granting a minor power of attorney so a trusted person can make decisions for them in your absence.

8. Sign & Notarize

Once you’ve filled out all the requested information, you can review your document for accuracy. As the grantor, you must sign the form before a notary public, as notarization is often mandatory for this document. Check your state’s laws for clarity on the requirements to ensure your document is enforceable.

How Legal Templates Helps With Irrevocable Trusts

Legal Templates makes it easy to create a comprehensive irrevocable trust. Secure your loved ones’ financial future by confidently creating this set-in-stone document. Our dynamic builder guides you through the process, leaving no aspect of your trust unaddressed. Once you create an account with us, you can enter your information, save it, and return again to continue filling it out.

When you’re done, you can save it as a PDF or Word document and print it out. For enforceability, be sure to wait to sign until you’re in front of a notary public.

Sample Irrevocable Trust Form

Below is an example of an irrevocable trust form. When you become familiar with all its parts, you can use our irrevocable trust template to fill yours out yourself.

Frequently Asked Questions

How much money do you need for an irrevocable trust?

There’s no monetary minimum you must have to make an irrevocable trust. However, it’s typically designed for individuals with larger estates (usually $1 million or more) who want to protect certain assets.

What should I not put in an irrevocable trust?

You should not put assets you may need in the future in an irrevocable trust, as it’s difficult to regain control of items in this type of trust.

Other assets you should consider keeping out of this trust include your primary residence, certain retirement accounts, and assets with high appreciation potential because of the tax complications they can cause.

What is the downside to an irrevocable trust?

The downside to an irrevocable trust is that you can’t change it easily once you sign it. However, it can still offer significant asset protection for your heirs, so you can still consider it but do so thoughtfully before finalizing it.