What Is a Loan Agreement?

A loan agreement is a written contract between 2 parties – a lender and a borrower, that can be enforced in court if one party does not hold up their bargain.

The borrower agrees that the borrowed money will be repaid to the lender at a future date and possibly with interest. In exchange, the lender cannot change their mind and decide not to lend the borrower the money, primarily if the borrower relies on the lender’s promise and makes a purchase expecting to receive money soon.

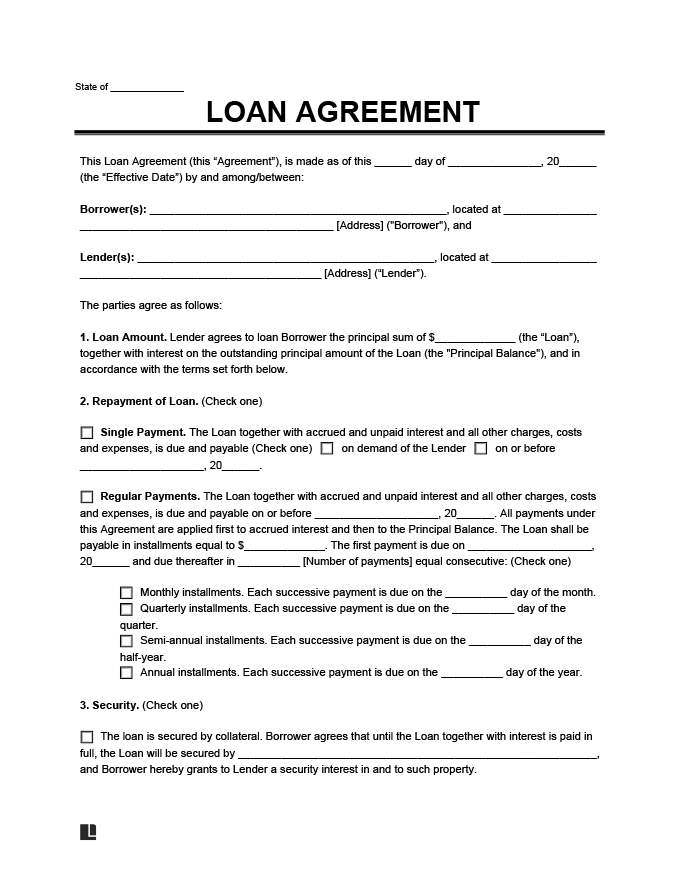

A simple loan agreement in writing will identify the following essential elements:

- Borrower: (aka. the “buyer” or “payer”) who is receiving the money and will repay it back

- Lender: (aka. the “issuer,” “maker,” “payee”, or “seller”) who is giving the money and will get the money back

- Principal Amount: the sum of money being borrowed

- Interest: additional money owed, usually a percentage, based on the amount borrowed

- Maturity Date: when the money should be repaid to avoid being in default

Further, the parties should consider these two additional questions:

1. How will the money be repaid?

The loan agreement should detail how the money will be paid back and what happens if the borrower cannot repay.

There are generally four types of repayment options:

| Installment Payments | Installments with Final Balloon Payment | Due on Specific Date ("Lump Sum") | Due on Demand (“Payable on Demand”) |

|---|---|---|---|

| Specific due date | Specific due date | Specific due date | No specific due date |

| Payments for principal and interest are made at regular intervals | Payments for interest only are made at regular intervals, principal amount due on maturity date | Entire amount owed, including interest, is paid all at once | Entire amount owed is due whenever the lender wants his or her money back |

| Example: $1,500 monthly payment actually consists of $500 towards the outstanding principal and $1,000 towards the interest with $1,500 due on the maturity date | Example: $500 monthly payment is applied only towards interest and full $10,000 loan amount is due on the maturity date | Example: $10,000 loan for a friend’s small business is due on a specific date | Example: $10,000 loan for a friend's small business is due at any time or whenever financially feasible |

2. What other details should be included?

The contract may also include these additional provisions:

-

Acceleration: whether the lender can move up the date of repayment and make the borrower repay the loan immediately

-

Possible Events of Acceleration

- if the borrower becomes bankrupt

- if the borrower fails to make payments

- if the borrower passes away (i.e., death) or dissolves

- if the borrower wants to pay off the note early

- if the borrower sells off a significant or material portion of their assets

-

Possible Events of Acceleration

- Amendment: any changes to the agreement must be in writing

- Collateral: what real estate or property can the lender keep if the borrower defaults

- Governing Law: which state laws apply if there is a problem with the agreement

- Joint and Several Liability: all of the borrowers are individually responsible for the total amount of the loan

- Late Charges: the borrower pays the penalty if payment is late

- Prepayment: the borrower can pay off the loan and interest early, possibly for a discount

- Right to Transfer: the lender may be able to transfer the loan to another party

The Difference Between a Loan Agreement, Promissory Note, and IOU

Generally, a loan agreement is more formal and less flexible than a promissory note or IOU. This agreement is typically used for more complex payment arrangements and often gives the lender more protections, such as borrower representations, warranties, and borrower covenants.

In addition, a lender can usually accelerate the loan if an event of default occurs, meaning if the borrower misses a payment or goes bankrupt, the lender can make the entire amount of the loan plus any interest due and payable immediately.

Here is a simple chart explaining the difference between an IOU, a promissory note, and a loan agreement.

| Loan | Promissory Note |

|---|---|

| promise to repay | promise to repay |

| steps for repayment | steps for repayment |

| timeline to repay | timeline to repay |

| legally binding | legally binding |

| signature of borrower | signature of borrower |

| signature of lender | |

| repay in installments | |

| consequences of defaulting (i.e. right to foreclosure) |

Who Needs a Loan Agreement?

While loans can occur between family members – called a family loan agreement – this form can also be used between two organizations or entities conducting a business relationship.

Here is a table detailing common borrowers and lenders who might need this agreement:

| Possible Lender | Possible Borrower |

|---|---|

| Seller of a home | Buyer of a home |

| Seller of a car | Buyer of a car |

| Investor | Startup company |

| Family member | Family member |

| Sympathetic friend with extra funds (i.e. able to lend but not give money) | Reliable friend with unexpected debt (i.e. unforeseen medical bills) |

When To Use a Loan Agreement Form

Relying only on a verbal promise is often a recipe for one person getting the short end of the stick. If the payback terms are complicated, a written agreement allows both parties to spell out any installment payment terms and the amount of interest owed.

If a disagreement arises later, a simple agreement serves as evidence to a neutral third party, like a judge, who can help enforce the contract.

Here are some situations where you may need a Loan Agreement:

- Starting a business and need a capital loan

- Purchasing land or a home with a real estate loan

- Investing in higher education or repaying a student loan

- Buying a new car or boat for personal reasons

- An employee loans from their employer

- Helping a friend or family out with a personal loan

Using a loan contract can be even more important for personal loans. To the IRS, money exchanged between family members can look like either gifts or loans for tax purposes.

Consequences of Not Having This Contract

A simple loan agreement details how much was borrowed, whether interest is due, and what should happen if the money is not repaid.

Here is a chart of some of the preventable suffering a loan agreement could prevent:

| Lender | Borrower |

|---|---|

| Borrowed money unpaid | Unpaid bills |

| Loss in value of used house or car | Paid for a house or car with no proof |

| Pay the IRS a gift tax of up to 40% | Pay the IRS income tax on the “gift” |

| Expensive lawyer fees to: | Expensive lawyer fees to: |

| Loss of friendship or family trust | Loss of friendship or family trust |

| Personal safety & well being | Personal safety & well being |