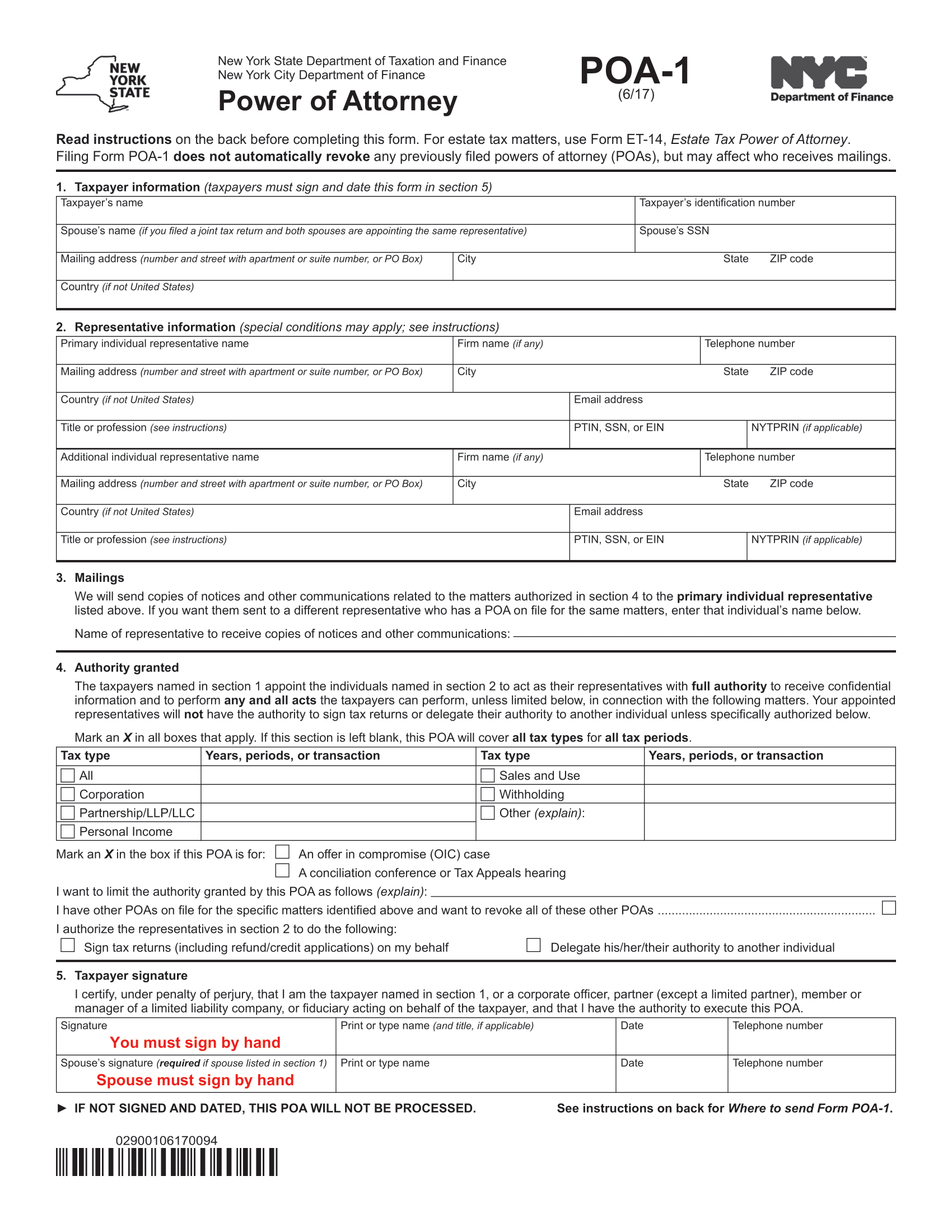

A New York tax power of attorney form (POA-1) is a legal document that enables a taxpayer to appoint a representative, typically a CPA, attorney, or other tax professional, to manage their tax affairs with the New York State Department of Taxation and Finance. This form allows for specific tax-related tasks to be designated to the representative. For estate tax matters, a New York estate tax power of attorney (Form ET-14) serves as an authorization form designating a representative for the executor of an estate.

The POA remains effective until the taxpayer revokes it or the representative withdraws. Note that this POA does not automatically revoke any previously filed POAs unless specifically indicated on the form. One or more representatives may be appointed on Form POA-1.

Signing Requirements — Taxpayer(s).