What Is an Alabama Promissory Note?

An Alabama promissory note is a legally binding document that outlines the terms of a loan agreement between a lender and a borrower. It serves as a written promise from the borrower to repay a specific amount of money and any accrued interest within a defined period.

The document includes details such as the borrowed sum, interest rate, repayment schedule, and any late charges or penalties for failing to meet loan obligations. Upon signing, both parties commit to the predetermined terms, thereby ensuring protection in the event of disputes or non-compliance.

Laws: Promissory notes fall under Alabama Code Title 7 and Title 8.

Statute of Limitations: Six years (AL Code § 6-2-34).

Types of Alabama Promissory Notes: Secured vs. Unsecured

In Alabama, promissory notes generally fall into two categories—secured and unsecured—each offering different levels of protection and flexibility depending on the nature of your loan.

Secured Alabama Promissory Note

Enables the lender to retain a valuable asset should the borrower fail to repay the loan amount.

Unsecured Alabama Promissory Note

It does not mandate the offering of valuable assets as collateral and typically extends to family or friends.

Usury Laws and Interest Rates in Alabama

The promissory note must adhere to the state’s usury laws as outlined in Title 8, Chapter 8.

- With a Contract (§ 8-8-1): 8%.

- Without a Contract (§ 8-8-1): 6%.

- For Loans Secured by Savings Account (§ 8-8-1.2): 2% added to the interest rate (rate of return) applied to the account.

- For Loans ($2,000+) (§ 8-8-5): No limit.

- For Judgments (§ 8-8-10): 7.5% or the rate specified in the contract.

- For Board of Education Loans ($100,000+) (§ 8-8-4): 15%.

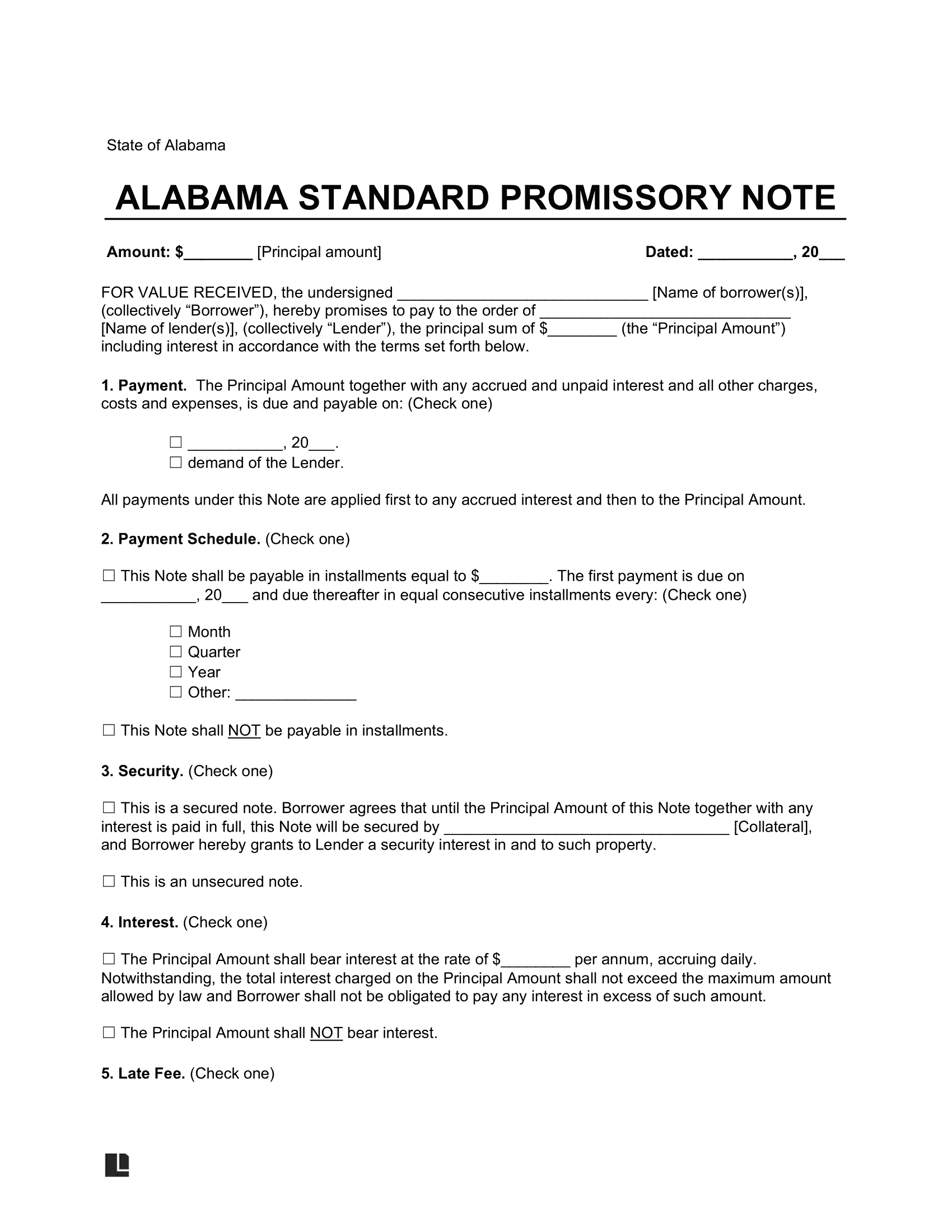

Sample Alabama Promissory Note

Below, you can see what an Alabama promissory note looks like. You can customize this template using our document editor and then download in PDF or Word format.