What Is an Alaska Promissory Note?

An Alaska promissory note formalizes a loan agreement between a lender and a borrower. It is a written commitment from the borrower to repay a specified amount of money and any agreed-upon interest within a predetermined timeframe.

The document includes the principal amount borrowed, interest rate, repayment schedule, and penalties for late payments or defaults. Additionally, it specifies whether the borrower is allowed to prepay the loan before the set date and if any discounts apply for doing so.

Laws: Promissory notes are governed by the statutes outlined in Alaska Statutes Title 45 – Trade and Commerce.

Statute of Limitations: Three or six years, depending on the type of item borrowed.

Types of Alaska Promissory Notes: Secured vs. Unsecured

Alaska promissory notes are available in secured and unsecured formats, depending on whether collateral is involved in the loan agreement.

Secured Alaska Promissory Note

Requires the borrower to provide an asset to the lender as collateral upon initiating the contract.

Unsecured Alaska Promissory Note

Does not mandate the offering of an asset (like a home or car) as collateral to secure the loan with the lender.

Usury Laws and Interest Rates in Alaska

The promissory note must comply with the usury laws of the state, as per Alaska Code, Title 45, Chapter 45.

- With a Contract (Under $25,000) (AK Stat § 45.45.010(b)): The maximum is determined by the higher of either 10% or 5% plus the annual rate charged to member banks of the Federal Reserve on the day of the loan.

- With a Contract (Over $25,000) (AK Stat § 45.45.010(b)): No limit.

- Without a Contract (AK Stat § 45.45.010(a)): 10.5%.

- For Small Business Loans (AK Stat § 45.81.210(a)): Must be acceptable collateral and 75% of the value of the collateral. The rate of interest may not exceed 9.5% a year on an unpaid balance.

- For Small Loans ($25,000 or Less) (AK Stat § 06.20.230): 3% per month for up to $850, 2% per month for amounts ranging from $850 to $10,000, and a rate agreed upon by contract for balances between $10,000 and $25,000.

- For Credit Union Loans (AK Stat § 06.45.060(a)(5)(A)(vi)): The limit is determined by the higher of either 15% or the rate specified in AK Stat § 45.45.010(b).

- On Judgments (AK Stat § 09.30.070): 3% above the Federal Reserve District discount rate in effect on January 2nd of the year in which the judgment is entered, with no maximum if the rate is established by contract.

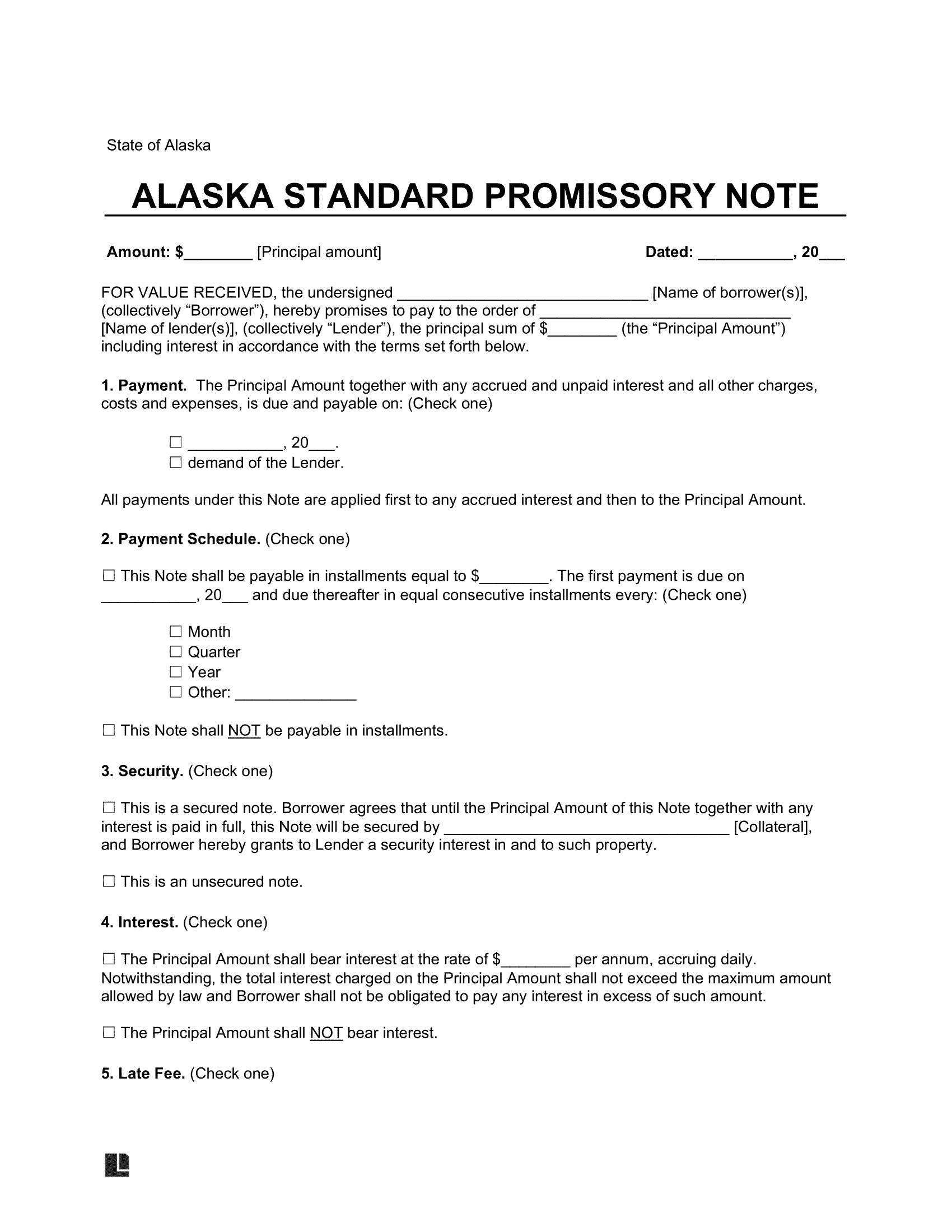

Sample Alaska Promissory Note

Below, you can see what an Alaska promissory note looks like. You can customize this template using our document editor and then download in PDF or Word format.