An Arizona promissory note is a legally binding document that solidifies a loan agreement between a lender and a borrower within the state. It represents a commitment from the borrower to repay a predetermined sum borrowed from the lender, including any interest accumulated, within an agreed-upon timeframe.

The document includes the borrowed amount and interest rate, repayment schedule, and consequences for late payments or defaults. Although not mandatory, notarization can offer additional evidence of the document’s legitimacy and add an extra layer of protection against potential disagreements regarding its validity.

Laws: Promissory notes are subject to the regulations specified within Arizona Revised Statutes Title 44.

Statute of Limitations: Six years.

Types of Arizona Promissory Notes

Arizona promissory notes are available as secured or unsecured, depending on whether the loan includes collateral to protect the lender.

Secured

Requires the borrower to provide collateral which the lender can legally seize if payments are not made.

Unsecured

Relies heavily on mutual trust, as the lender has no collateral to fall back on in case of borrower default.

Usury Laws and Interest Rates

The promissory note must comply with the usury laws of the state, as mandated by Title 44, Chapter 9, Article 1.

- With a Contract (§ 44-1201(A)): No limit.

- Without a Contract (§ 44-1201(A)): 10% (not including medical debts).

- On Judgments (§ 44-1201(B)): 10% or 1% plus the prime rate, whichever is lower (not including medical debts).

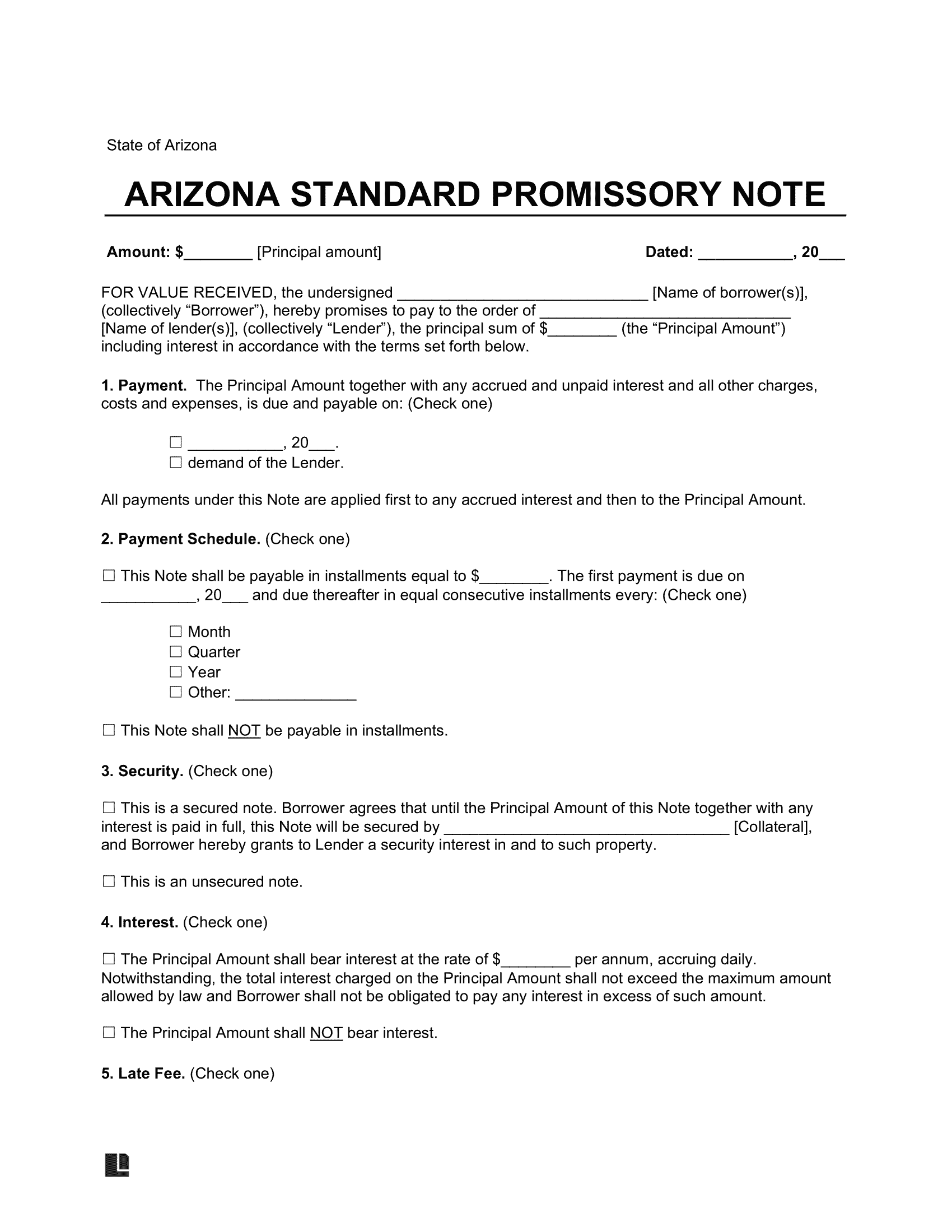

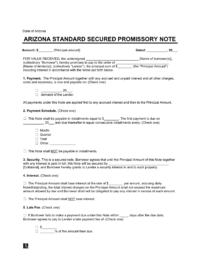

Sample Arizona Promissory Note

Below, you can see what an Arizona promissory note looks like. You can customize this template using our document editor and then download in PDF or Word format.