What Is an Arkansas Promissory Note?

An Arkansas promissory note represents a written commitment from the borrower to repay the lender a specified sum, including any accrued interest. It outlines the terms and conditions of a loan agreement, such as the deadline by which the loan must be fully repaid and any penalties applicable for late payments or defaults.

In the case of secured loans, the document may specify the collateral provided by the borrower to secure the loan. While notarization is not mandated by state law, it can serve as valuable evidence of the document’s authenticity and may strengthen legal standing in case of disputes.

Laws: The applicability of relevant laws varies depending on the purpose for which the documents are issued. For instance, promissory notes falling under business or commercial law are governed by Arkansas Code Title 4, whereas those associated with higher education are regulated by Title 6.

Statute of Limitations: Five years.

Types of Arkansas Promissory Notes: Secured vs. Unsecured

Arkansas promissory notes can be secured with collateral or left unsecured, depending on the level of risk the lender is willing to take on.

Secured Arkansas Promissory Note

Used when both parties agree on specific physical item(s) to be transferred to the lender if the loan cannot be repaid.

Unsecured Arkansas Promissory Note

Used in non-collateralized loan agreements.

Usury Laws and Interest Rates in Arkansas

The promissory note must adhere to the state’s usury laws, as stipulated in Title 4, Subtitle 5, Chapter 57.

- With a Contract (§ 4-57-104): Amendment 89 of the Arkansas Constitution establishes the maximum interest rate at 17%.

- Without a Contract (§ 4-57-101(d)): 6%.

- For Judgments (§ 16-65-114(a)(2)): 17% (under Arkansas Constitution, Amendment 89).

- For Policy (Life Insurance) Loan (§ 23-81-109(c)(1)): 8% or an adjustable maximum interest rate (subject to usury limitations).

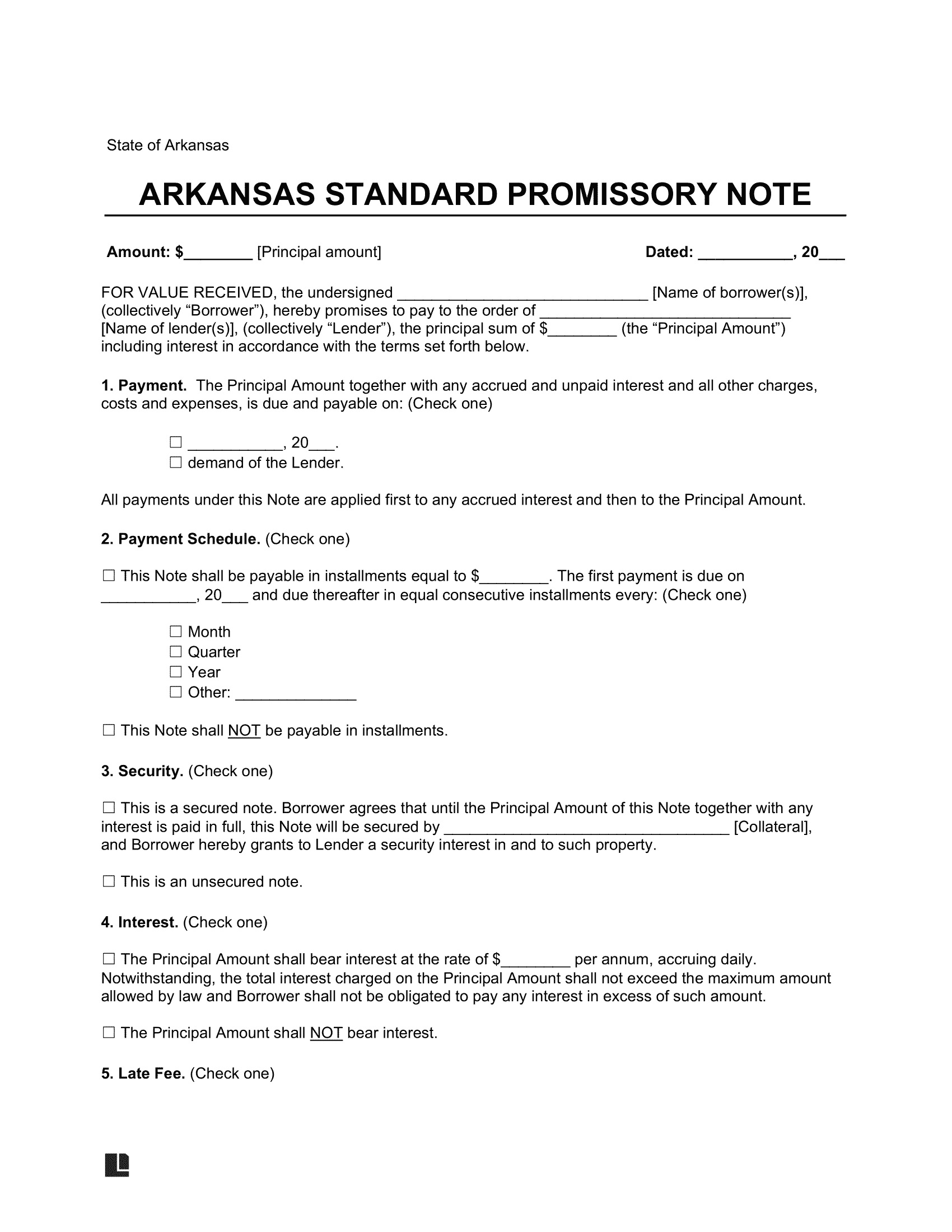

Sample Arkansas Promissory Note

Below, you can see what an Arkansas promissory note looks like. You can customize this template using our document editor and then download in PDF or Word format.