What Is a California Promissory Note?

A California promissory note is a crucial legal instrument in formalizing a loan agreement between a lender and a borrower. It serves as a written commitment from the borrower to repay a specified sum within a defined timeframe. While it does not outline the consequences of complete default, the lender retains the option to pursue legal action if the borrower fails to pay on time or refuses to make payments.

The state’s legal landscape emphasizes consumer protection; therefore, these types of documents may include additional provisions to safeguard borrowers’ rights, such as disclosures regarding their rights and obligations and provisions addressing prepayment penalties, acceleration clauses, and non-recourse language.

Laws: Governed by the California Civil Code, promissory notes in California must be in writing and adhere to specific requirements to ensure their legality and enforceability (§ 1624).

Statute of Limitations: Four years if based on a contract (CCP § 337). Six years if the document is a negotiable instrument (COM §3118(a)).

Types of California Promissory Notes: Secured vs. Unsecured

California promissory notes may be secured by assets or remain unsecured, depending on how the borrower and lender structure their agreement.

Secured California Promissory Note

Requires that the borrower provide personal assets that the lender receives in case of default.

Unsecured California Promissory Note

Preferred among close friends or family, as the loan recipient is not obligated to provide any collateral.

Usury Laws and Interest Rates in California

Promissory notes must comply with the state’s usury laws as detailed in CONS Article XV.

- Contracts For The Sale of Goods For Personal, Family, or Household Purposes (CONS Article XV (1)): No more than 10% per annum.

- For Any Other Type of Contract (CONS Article XV): No more than 10% per annum or no more than 5% plus the prevailing rate of the Federal Reserve Bank of San Francisco’s discount rate, whichever is higher.

- For Money Judgment (CCP § 685.010): 10% per annum on the principal amount of the judgment.

- For Judgment for Damages Against A Public Entity (CIV § 3287(c)): At a rate equal to the weekly average one-year Treasury Yield but not more than 7% per annum.

- For Pawn Brokers (CIV § 21200): Not more than 3% per month on the unpaid principal of the loan.

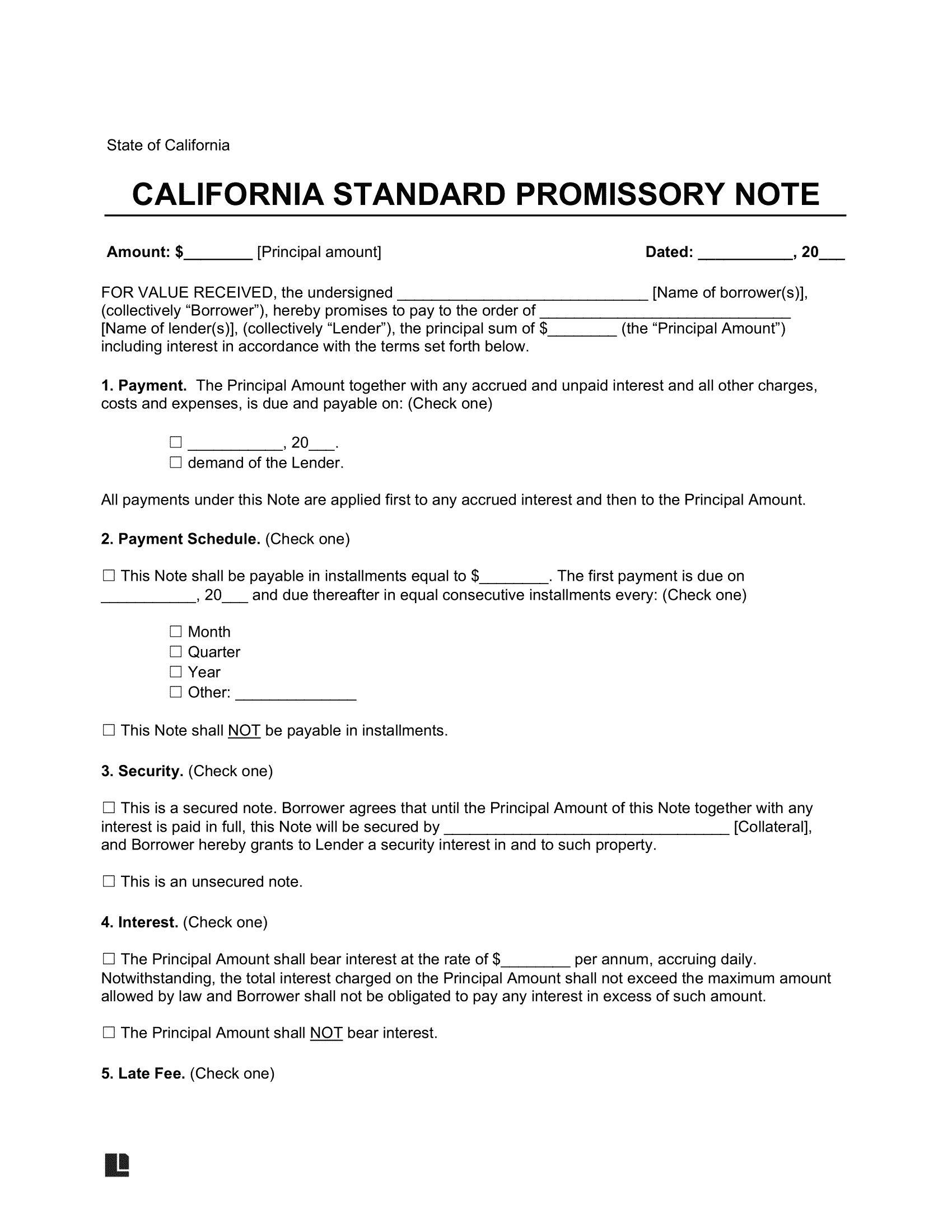

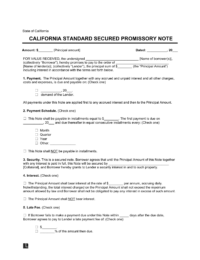

Sample California Promissory Note

Below, you can see what a California promissory note looks like. You can customize this template using our document editor and then download it in PDF or Word format.