What Is an Indiana Promissory Note?

An Indiana promissory note is a legal agreement between a lender and borrower for a loan. It outlines the amount borrowed, interest rates, late fees, and repayment schedule.

It contains specific terms for loan repayment and may require a co-signer for borrowers with low income or poor credit. A promissory note is a legally binding document that protects both parties in the lending process.

Laws: Title 24, Art. 4.5, Ch. 3 governs the creation and implementation of promissory notes.

Statute of Limitations: Six years. (IC 34-11-2-.9)

Types of Indiana Promissory Notes: Secured vs. Unsecured

Indiana promissory notes may be secured with valuable assets to reduce lender risk or unsecured, depending on the trust and agreement between the parties.

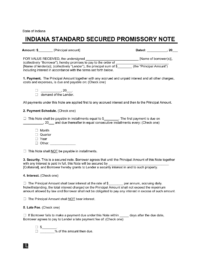

Secured Indiana Promissory Note

Use a valuable asset as security to obtain a loan.

Unsecured Indiana Promissory Note

Use good credit or personal connections as a guarantee to obtain a collateral-free loan.

Usury Laws and Interest Rates in Indiana

Promissory notes must comply with Indiana’s usury laws, which you can find in the Indiana Code at IC 24-4.5-3-201:

- For Unsupervised Loan (IC 24-4.5-3-201(1)): 25% per annum

- For Supervised Loans (IC 24-4.5-3-508(2)): 15%-36% depending on the loan amount.

- For Monetary Judgments Based on Contract (IC 24-4.6-1-101): Not to exceed 8% per annum

- For Monetary Judgements in Absence of Agreement (IC 24-4.6-1-102): 8% per annum

- For Monetary Judgements Against State (IC 34-54-8-5): 6% starting on the forty-fifth (45th) day after judgment.

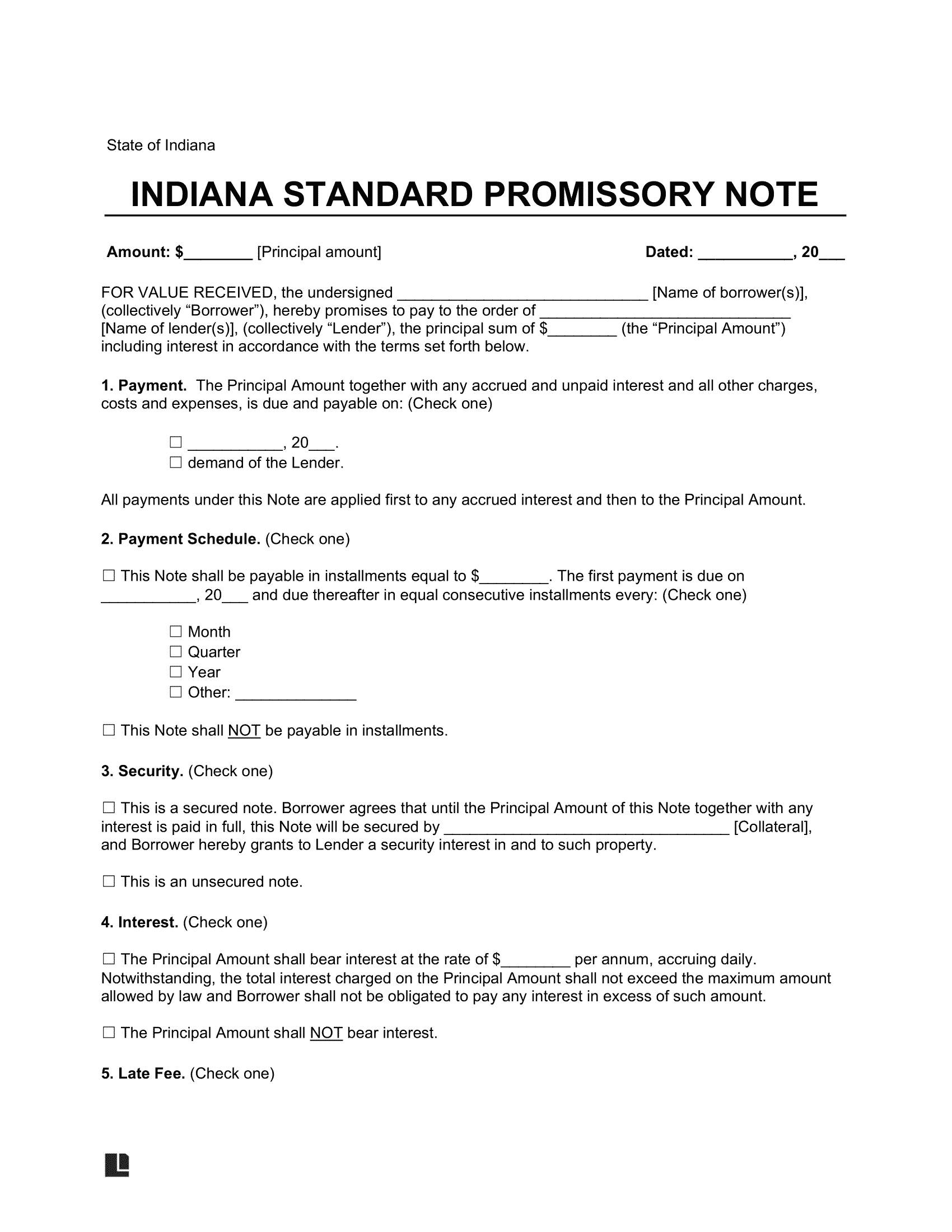

Sample Indiana Promissory Note

Here’s a sample Indiana promissory note to guide you. You can modify the terms using our online editor and download them instantly in Word or PDF format.