What Is a Minnesota Promissory Note?

A Minnesota promissory note is a legal document that outlines the terms and conditions of a loan agreement between two parties. It ensures that the lender of the balance is reimbursed the total amount of the note plus accumulated interest.

This document defines provisions such as the loan maturity date, repayment method, and collateral that the borrower must put up to secure the loan. Both parties agree to the terms, and legal action may be taken if the debt is not repaid on time.

Laws: § 336.9-204 Minnesota Statutes govern the creation and implementation of promissory notes.

Statute of Limitations: Six years.

Types of Minnesota Promissory Notes: Secured vs. Unsecured

Minnesota promissory notes are available in secured form, backed by collateral, or unsecured, relying solely on the borrower’s commitment to repay.

Secured Minnesota Promissory Note

Obtain financing by providing collateral in the form of an asset.

Unsecured Minnesota Promissory Note

Secure a loan without collateral by demonstrating good credit or strong personal connections.

Usury Laws and Interest Rates in Minnesota

Promissory notes must comply with Minnesota’s usury laws, which you can find in Chapter 334:

-

With a Contract (§ 334.01 Subd. 2): 8%

- Contracts over $100,000: No maximum, except for mortgage loans (§ 47.20 Subd. 4a.(a)) and mortgage prepayment penalties (§ 58.137 Subd. 2(a)(4)).

- Without a Contract (§ 334.01): 6% per year

- For Business or Agricultural Loans (less than $100,000) (§ 334.011 Subd. 1): 4.5% above the 90-day commercial paper discount rate.

- For Loans by Charitable Organizations (less than $10,000) (§ 334.011 Subd. 5): 16%

- For Loans Secured by Savings Account (§ 334.012): 2% over the interest rate payable on the account.

-

For Monetary Judgments* (§ 549.09):

- Judgments under $50,000: Interest will be calculated based on the secondary market yield of one (1) year US Treasury bills as per 549.09(c)(1)(i).

- Judgments over $50,000: 10%

*Except for child support awards in judgments of less than $50,000, this does not apply to family court judgments.

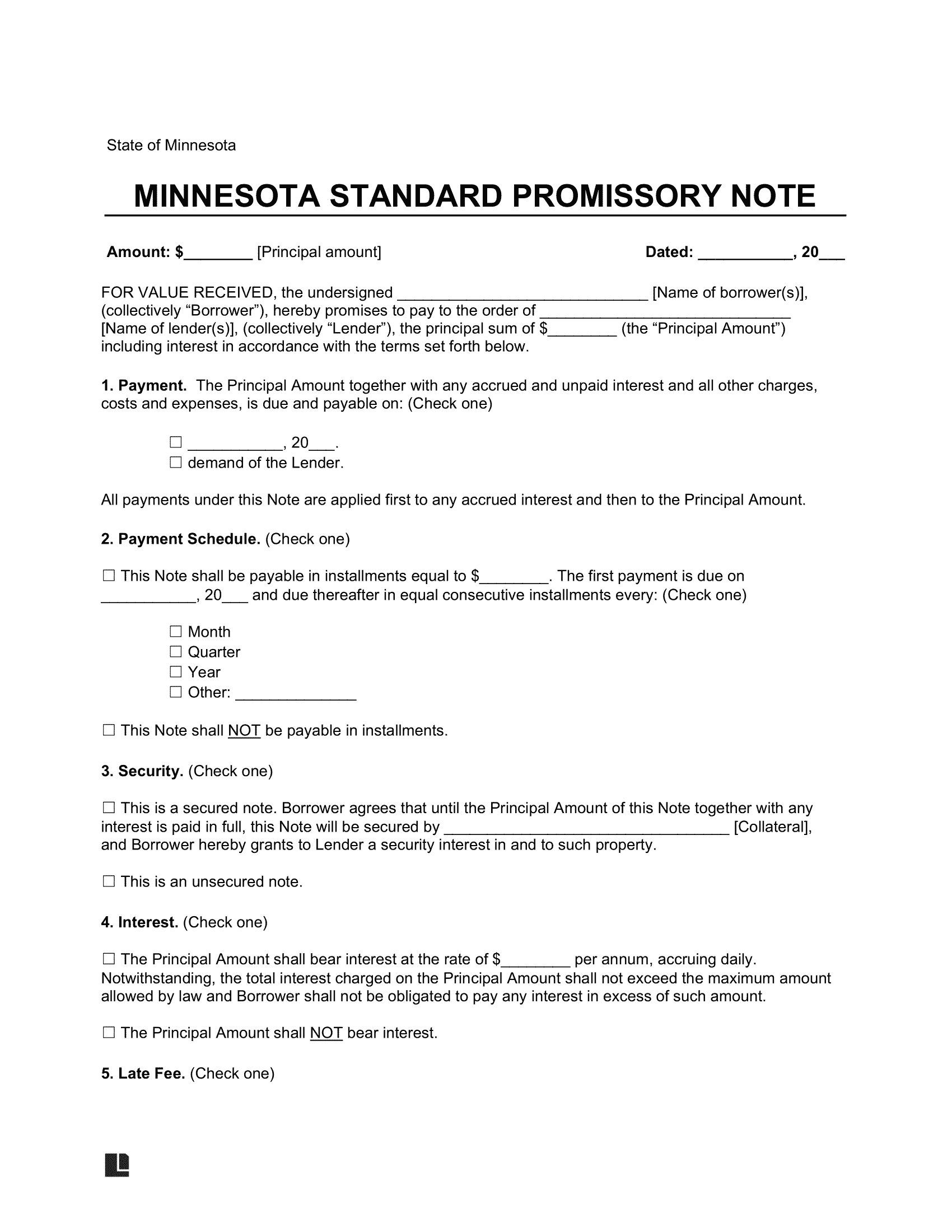

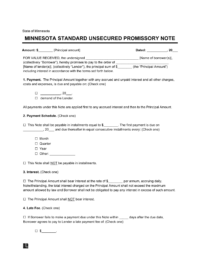

Sample Minnesota Promissory Note

Check out this example of a Minnesota promissory note. Use our online editor to personalize it for your situation, then download it in PDF or Word format.