What Is a Missouri Promissory Note?

A Missouri promissory note is a legal document that outlines the terms of a loan between a lender and a borrower. It includes details such as the loan amount, interest rate, repayment schedule, and penalty fees for late payments. If applicable, both parties and a co-signer must sign the note.

If the borrower defaults, the lender may use the note to take legal action. State law requires lenders to provide borrowers with receipts for each payment, and upon full repayment, the lender must mark the note as paid and return it to the borrower.

Laws: Title XXVI Trade and Commerce, § 400.9-408 of the Missouri Revised Statutes govern the creation and implementation of promissory notes.

Statute of Limitations: Ten years. (§ 400.3-118)

Types of Missouri Promissory Notes: Secured vs. Unsecured

In Missouri, promissory notes come in two types: secured and unsecured. A secured note adds extra protection with collateral, while an unsecured one is built on trust and clear terms.

Secured Missouri Promissory Note

Obtain a loan by pledging a valuable asset as security.

Unsecured Missouri Promissory Note

Use good credit or personal connections as a guarantee to obtain a collateral-free loan.

Usury Laws and Interest Rates in Missouri

Promissory notes must comply with Missouri’s usury laws, which you can find in the Missouri Revised Statutes Title XXVI, Chapter 408:

- With a Contract (§ 408.030): 10%, the interest charged cannot be more than the market rate unless the interest rate exceeds 10%. The parties may also choose to pay a $10 fee instead of interest (§ 408.031).

- Without a Contract (§ 408.020): 9% per annum

- For Judgements (§ 408.040(3)): Federal Funds Rate + 5% in tort actions; 9% in non-tort actions unless a contract sets a higher rate.

- In General (misdemeanor) (§ 408.095): It is a misdemeanor to collect interest at an amount greater than 2% per month.

- For Secured Personal Credit Loans (§ 367.021(2)): 2% per month

-

Loans without Interest Limit (§ 408.035):

- Loan to a corporation, GP, LP, LLC;

- Credit extensions for agricultural, business, or commercial purposes;

- Non-residential real estate loans; or

- Loans secured solely by stocks, bonds, bills, CDs, or receipts over $5,000.

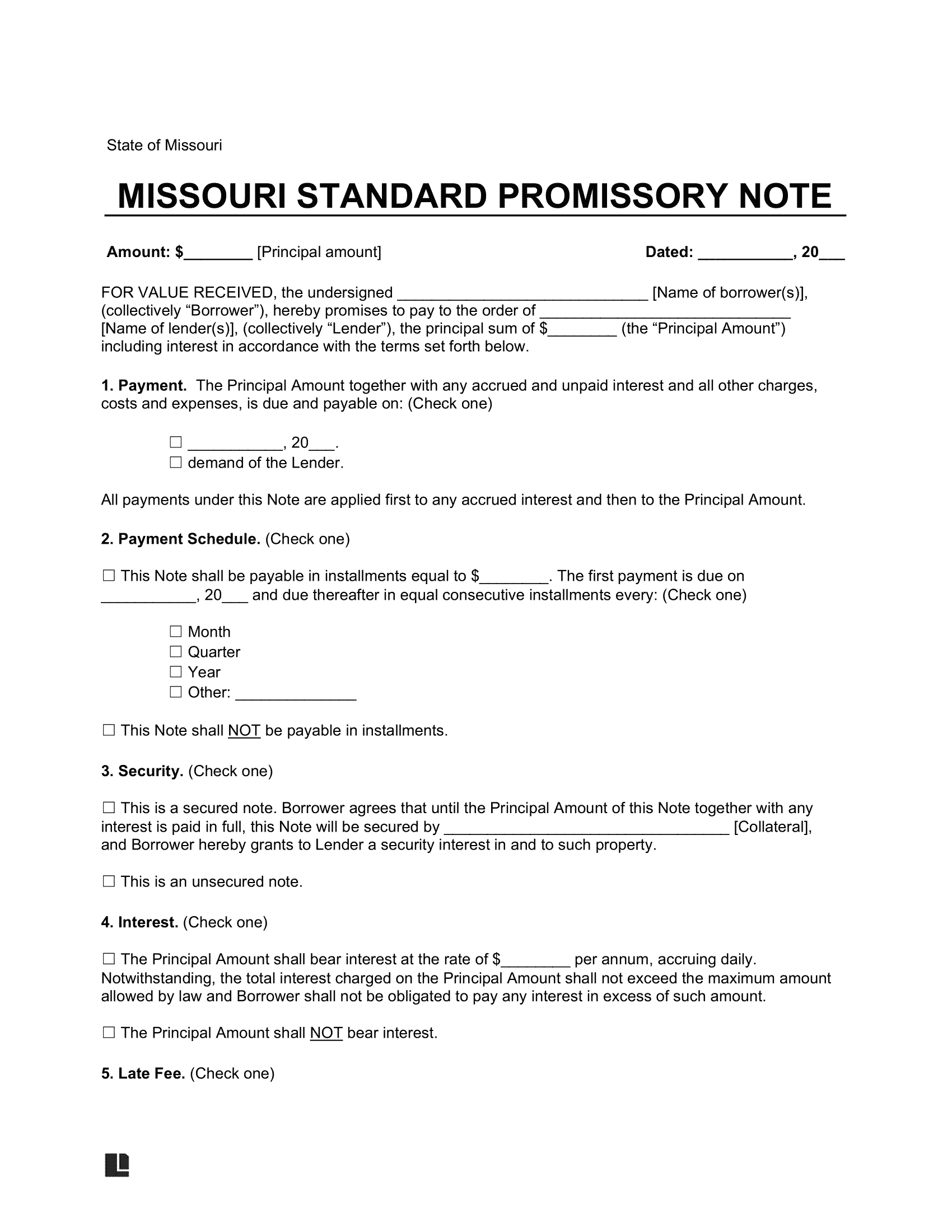

Sample Missouri Promissory Note

View an example of a Missouri promissory note to understand its format. Create your own via our document editor and download it in PDF or Word format.