What Is a Nevada Promissory Note?

A Nevada promissory note formalizes the loan process by stating the borrower’s commitment to repay the loaned amount plus interest by a set date, with signatures from all parties for legal validation.

Although less detailed than a loan agreement and seldom used by banks, it legally binds the borrower, allowing the lender to sue if repayment terms are breached, and may include co-signers or collateral for added security.

Laws: Promissory notes fall under Nevada Revised Statutes Chapter 99.

Statute of Limitations: Six years (§104.3118).

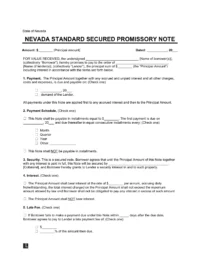

Types of Nevada Promissory Notes: Secured vs. Unsecured

Choosing the right promissory note in Nevada helps you align the loan’s structure with the risks involved. It can either be secured or unsecured.

Secured Nevada Promissory Note

Allows the lender to keep a valuable asset if the borrower does not fulfill the loan repayment terms.

Unsecured Nevada Promissory Note

Often accessible to those with good credit or close contacts, this choice doesn't require collateral.

Usury Laws and Interest Rates in Nevada

The promissory note must adhere to Nevada’s usury laws as outlined in Chapter 99:

- With a Contract (§ 99.050): Unlimited, but cannot exceed the lesser of 36% per annum, or the lowest annual rate for consumer credit to service members or dependents.

- Without a Contract (§ 99.040):Prime rate plus 2% at Nevada’s largest bank.

- For Judgments (§ 17.130(2)): Prime rate plus 2% at Nevada’s largest bank if no rate is specified by contract or law.

- For Pawnbrokers (§ 646.050): Monthly rate of 13%.

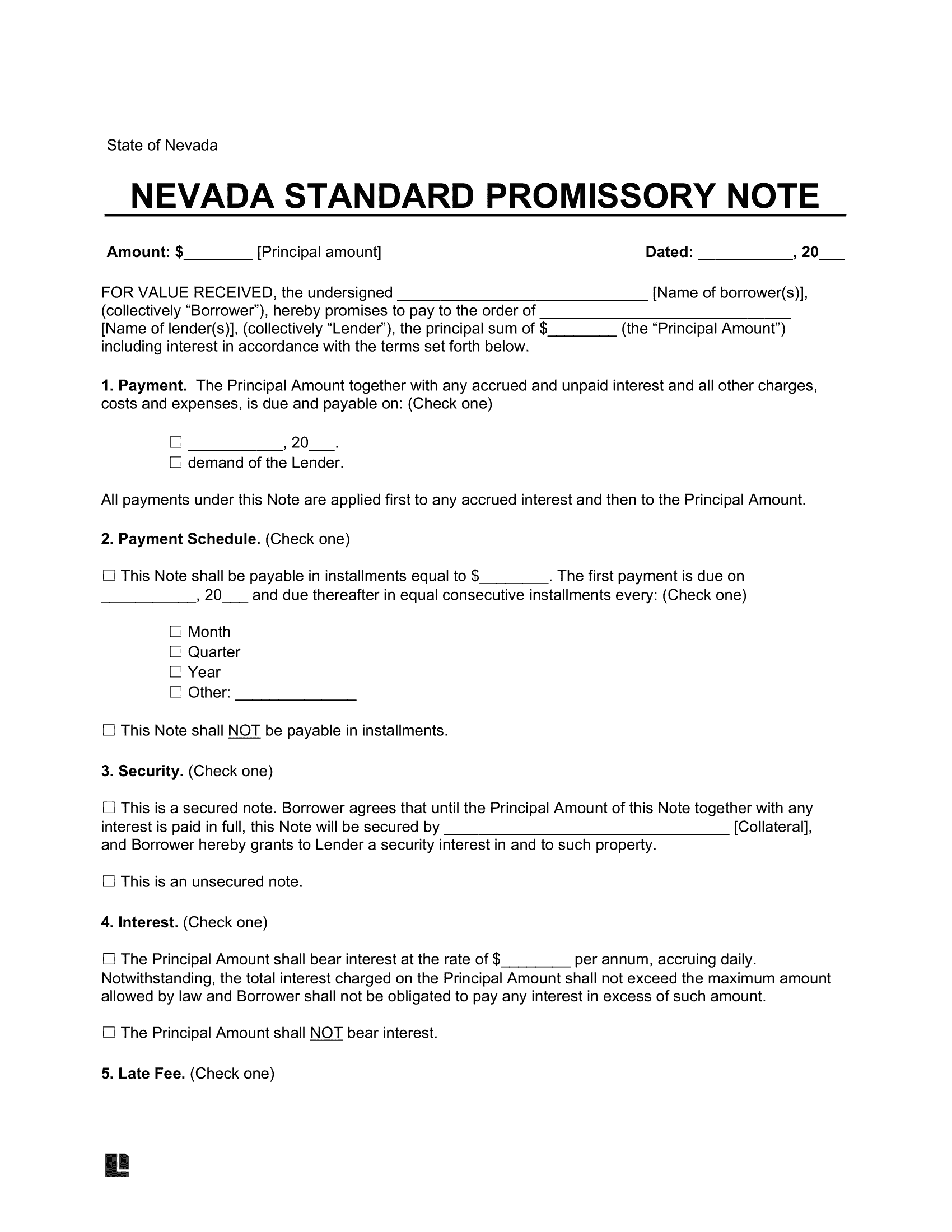

Sample Nevada Promissory Note

View a free sample Nevada promissory note to see what it looks like. When you’re ready to create your own, you can use our document editor to finalize your document. It is available in PDF and Word formats.