What Is a North Carolina Promissory Note?

A North Carolina promissory note is a flexible, binding document outlining loan repayment terms between a lender and borrower, including due date, interest rate, installment schedule, and collateral. It is more detailed than an IOU but simpler than a standard loan agreement.

Laws: Promissory notes fall under the North Carolina General Statutes Chapter 24 – Uniform Commercial Code.

Statute of Limitations: Six years (NC. Gen. Stat. §25-3-118).

Types of North Carolina Promissory Notes: Secured vs. Unsecured

The right North Carolina promissory note ensures your loan arrangement matches the level of trust and the value of what’s at risk. Choose from either a secured or an unsecured promissory note template.

Secured North Carolina Promissory Note

Ensures the lender's protection by pre-determining collateral items for security in the event of a borrower's default, prior to finalizing the agreement.

Unsecured North Carolina Promissory Note

Removes the requirement for the borrower to provide collateral to the lender.

Usury Laws and Interest Rates in North Carolina

The promissory note must adhere to North Carolina’s usury laws as outlined in Chapter 24:

- With contract (NC Gen. Stat. § 24-1.1(a)): Loans under $25,000: Interest rate set monthly by the North Carolina Association of Banks on the 15th (consistently 16% since 1984). Loans over $25,000: No interest rate limit.

- Without contract (NC Gen. Stat. § 24-1): 8%.

- For Monetary Judgments (NC Gen. Stat. § 24-5(a)): The contract rate applies, or 8% per annum, on the unpaid balance, if no rate is specified.

- In case of default, the borrower might have to pay legal fees, capped at 15% of the loan balance at the time of default by NC Gen. Stat. § 6-21.2(1).

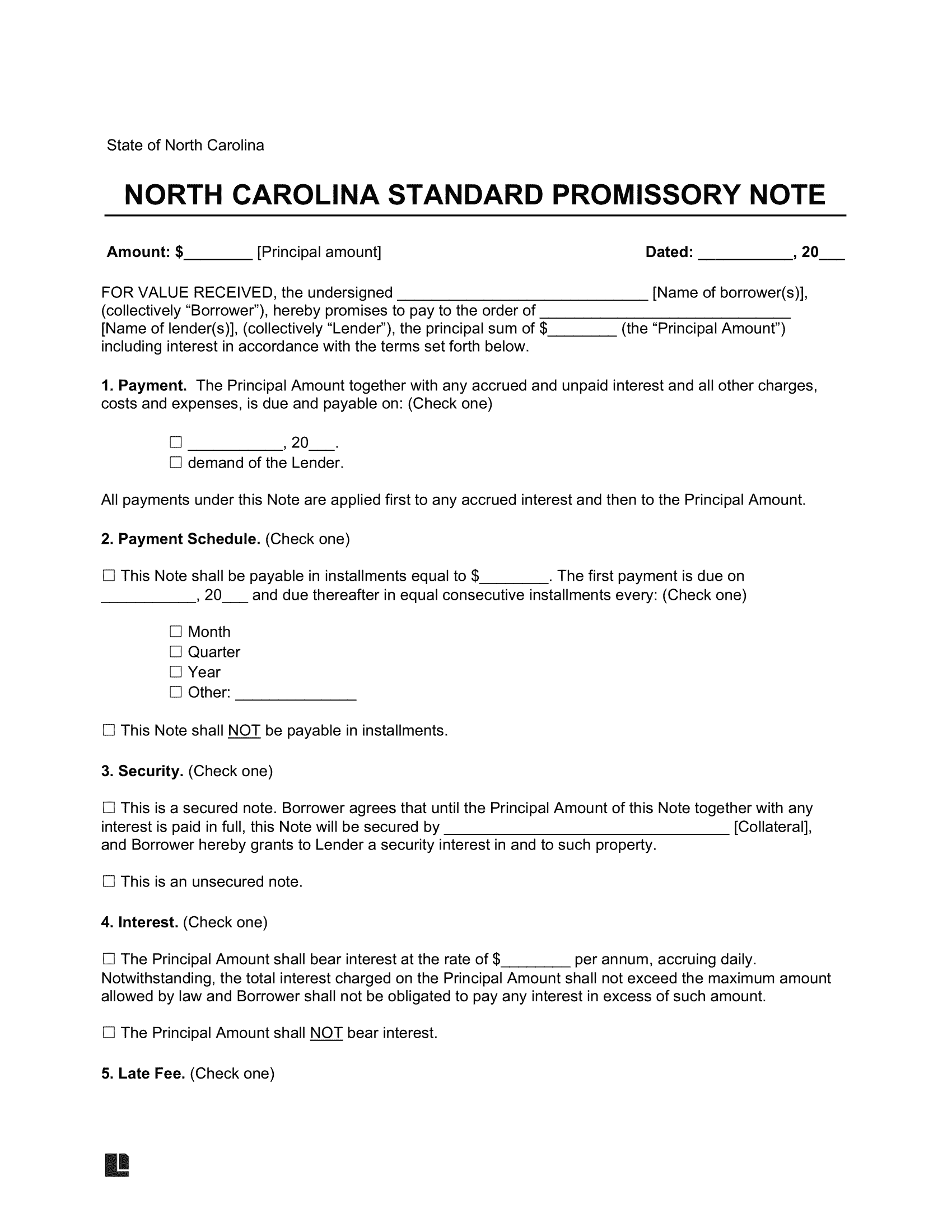

Sample North Carolina Promissory Note

View a free sample of a North Carolina promissory note to learn its format. Customize your own using our document editor and download the final version in PDF or Word format.