Using a quitclaim deed to transfer property in Illinois does carry some fees that you should expect as part of the property transfer.

Filing Fees

When you file your document, you should expect to pay a fee to have the deed transferred. Those fees may vary by county, so consult the County Recorder’s Office for more information.

Taxes

In addition to filing fees, you should expect to pay some state and federal taxes on the property.

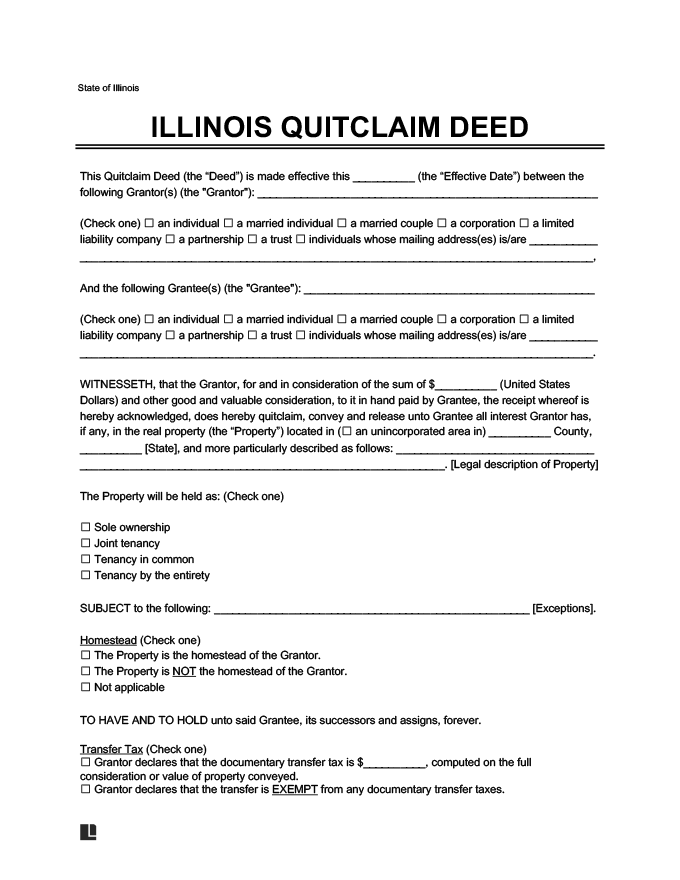

1. Transfer Tax

Transfer taxes in the state are assessed at the County Recorder of Deeds. You will need to purchase Department of Revenue Stamps equal to the tax amount. As laid out in 35 ILCS 200/, state transfer taxes are $.50 per $500 of value noted in the Transfer Tax Declaration.

Who Pays the Transfer Tax?

Most of the time, the grantee, or the new owner of the property, will pay the transfer tax. However, in some cases, the grantee may negotiate with the grantor to have the grantor pay. There are also several situations when the grantor may choose to include the transfer tax as part of a gift, especially in the case of a property transfer between family members.

Exemptions to Transfer Tax

Under 35 ILCS 200/31-45, there are several exemptions to the transfer tax. These include:

- Property transfers made before January 1, 1968, but recorded after that date.

- Trust documents executed before January 1, 1986, but recorded after that date.

- Government property transfers, including property acquired by or from any government entity or properties transferred between government bodies.

- Property acquired by or from charitable, religious, or educational organizations.

- Deeds that secure debt or obligations.

- Deeds issued to a mortgage holder in order to move forward with foreclosure proceedings.

- Deeds related to the purchase of a primary residence of a participant in a program created by the Home Ownership Made Easy Act.

- Cases in which the recipient paid less than $100.

2. U.S. Gift Tax (Form 709)

The United States imposes a gift tax when large gifts are given to another party. This tax is based on the assessed value: in this case, the value of the property.

Illinois does not have a separate gift tax.

3. Capital Gains Tax

A capital gains tax is applied to the value of the profit made on the sale of a large asset, including a property. If the property is sold at a profit from its original purchase price, the grantor may need to pay the tax on that increased value. However, the IRS does allow some exclusions to the capital gains tax.

Illinois also has its own capital gains tax.