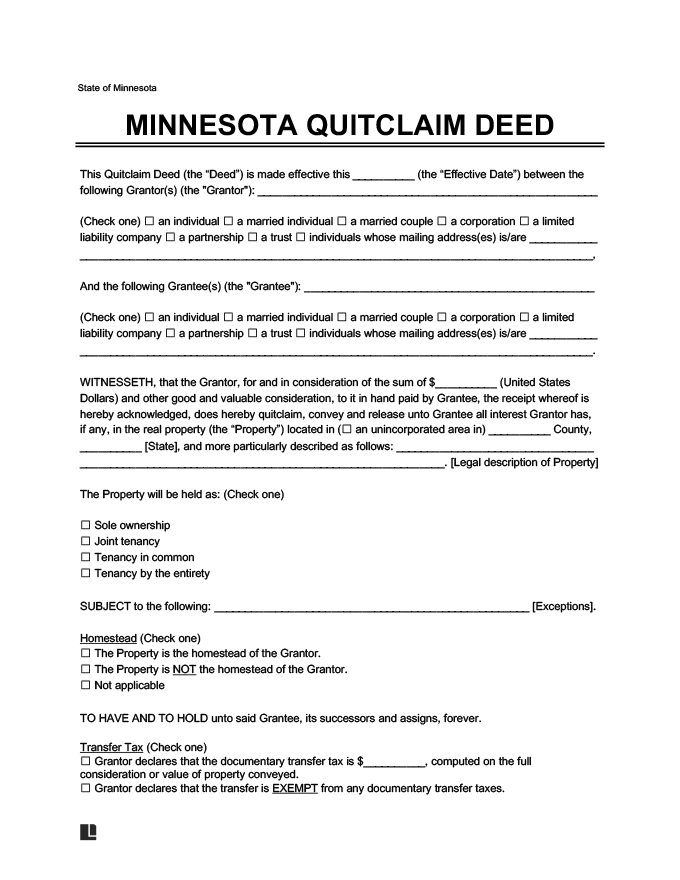

What Is a Minnesota Quitclaim Deed?

A Minnesota quitclaim deed is a document used to transfer property ownership from the grantor to the grantee without providing any guarantees or warranties on the property title. Per MN Stat § 507.06, a quitclaim deed is just as effective as a deed of bargain and sale, but it only passes whatever interest the grantor actually has. It does not guarantee they actually own the property.

An MN quitclaim deed goes into effect when it’s properly recorded. It doesn’t expire, so the ownership interest remains with the grantee indefinitely. The deed may be challenged if

Need to Quitclaim Property to Certain Parties?

No matter who you’re quitclaiming property to, Legal Templates’s form can accommodate the transfer. Our template works for the following property conveyances:

- Individual to individual

- Individual to business

- Business to individual

- Business to business

What to Include in a Minnesota Quitclaim Deed

MN Stat § 507.07 provides the statutory language for a quitclaim deed. As long as your MN quitclaim deed is substantially similar to it, it will likely be legally enforceable. Here are the key elements your quitclaim deed should include:

- Grantor’s name and place of residence

- Grantee’s name and place of residence (and address for property tax statements per MN Stat § 507.092)

- Deed preparer name and address (MN Stat § 507.091)

- Consideration for the property

- Statement of conveyance (“conveys and quitclaims”)

- County of the property being conveyed

- Legal description of the property being conveyed

- Date of conveyance

- Grantor’s signature

- Statement of deed tax owed or exemption (MN Stat § 287.241)

- Designated transfer statement, if applicable (MN Stat § 272.115.6)

- Well disclosure statement, if applicable (MN Stat § 103I.235)

Sample Minnesota Quitclaim Deed

View an example of a Minnesota quitclaim deed so you can learn how it’s structured. Then, write your own by using Legal Templates’s guided form. Download it in PDF or Word format.

Formatting Requirements for a Minnesota Quitclaim Deed

MN Stat § 507.093 outlines formatting standards for recorded documents, including quitclaim deeds. To avoid filing delays or additional fees, your deed should meet the following guidelines:

- Printed, typed, or computer-generated in black ink in no smaller than 8-point font

- Printed on white paper of at least 20-pound weight, no larger than 8 ½ in. x 14 in.

- Blank 3 in. space at the top of the first page

- ½ in. margins for the rest of the document

- The document title is prominently displayed below the blank space on the first page

- No additional affixed or attached sheets obscuring the form

- Sufficiently legible to create a readable copy using the county recorder’s chosen method

How to File a Quitclaim Deed in Minnesota

Filing a quitclaim deed in Minnesota requires more than just filling out a form. From locating the property’s legal description to completing disclosures and submitting the deed with the county recorder, each step helps ensure a smooth and valid transfer.

Step 1 – Obtain the Original Deed

Obtain a copy of the current owner’s deed for the property being conveyed. You will need the information from this document to proceed, whether you are transferring property or updating an existing deed.

If you cannot obtain a copy from the current owner, contact the county recorder in the county where the property is located to request a copy.

Step 2 – Fill out the MN Quitclaim Deed Form

When drafting your deed, follow the formatting and content requirements noted above. You can use Legal Templates’s form to get started.

Step 3 – Complete the Certificate of Value Form and Necessary Disclosures

Quitclaimed properties transferred for consideration over $3,000 are assessed a deed tax (MN Stat § 272.115). You must pay the tax and complete an electronic certificate of value (eCRV) form. The county auditor will then provide an acknowledgment for you to submit with your deed. Exemptions under MN Stat § 287.22 should be noted on the face of the deed in lieu of the certificate of value acknowledgment.

MN Stat § 103I.235 also requires disclosure of the status and location of wells. For owners unaware of any wells on the property, the following disclosure should be noted on the quitclaim deed: “The Seller certifies that the Seller does not know of any wells on the described real property.”

Step 4 – Sign Before a Notary

Per MN Stat § 507.24.2, a quitclaim deed must include the original signature of the grantor and an acknowledgment from a notary or other approved officer under MN Stat § 507.24.1. If the grantor is married and conveying homestead property, the grantor’s spouse must also sign the quitclaim deed (MN Stat § 507.02). The county recorder may accept electronic signatures (MN Stat §§ 507.0941 to 507.0948).

Step 5 – Record With the County Recorder’s Office

To fulfill requirements under MN Stat § 507.34, you must register your form with the county recorder’s office in the county where the property is located. Properties that exist in multiple counties must be registered in each county.

At the time of registration, the recorder may charge deed tax, consistent with MN Stat § 287.21. Depending on the county, they may also charge a land preservation fee (MN Stat § 40A.152).

How Much Does a Minnesota Quitclaim Deed Cost?

Quitclaim deeds in Minnesota come with predictable recording fees and a deed tax based on the value of the transfer. Knowing which exemptions apply—and what additional costs may arise—can help you avoid delays and stay on budget.

Recording Fees

The basic recording fee is $46.00 for the document (MN Stat § 357.18). If the property requires a well disclosure, the county recorder may also assess a $50.00 fee (MN Stat § 103I.235).

Taxes

Parties who use a quitclaim deed to transfer property in Minnesota may be subject to certain taxes, including a deed tax, gift tax, and capital gains tax.

1. Deed Tax

MN Stat § 287.21 establishes the amount of tax imposed on deeds transferring property.

Who Pays the Deed Tax?

The current owner, or grantor, typically pays deed tax on the consideration they received for the property conveyed via a quitclaim deed. The parties may contract or agree for the receiving party to pay the tax if they desire.

Exemptions to Deed Tax

Per MN Stat § 287.22, the following real estate transactions are exempt:

- Deeds transferring cemetery lots

- Deeds transferring real estate from a personal representative to a beneficiary

- Deeds concerning foreclosures

- Deeds modifying, granting, terminating, or creating an easement

- Deeds transferring property pursuant to a divorce decree

- Deeds conveying property upon the death of the owner

- Deeds conveying property to or from the US government or any agency or instrumentality thereof

Tax Rates

The state deed tax varies depending on the details of the real estate transfer. The following real property transfers are subject to a $1.65 flat tax:

- Transfers for business consolidations, mergers, or designated transfers.

- Transfers for no consideration or consideration of less than $3,000.

A tax of .0033 of the net consideration is assessed for any transfers with consideration greater than $3,000.

The same tax rate of .0033 is retroactively imposed on the property’s consideration if it is conveyed through a non-designated transfer within six months of a designated transfer for which the flat $1.65 tax was assessed. The seller may also be subject to a penalty for willful evasion under MN Stat § 287.21.

2. Gift Tax

Typically, there is no state gift tax imposed. However, if the real estate property you convey exceeds the exclusion amount listed under MN Stat 291.016, your estate may be taxed. Speak with an estate planner or probate attorney to learn whether this tax will affect you.

The IRS charges gift taxes for those whose gifts exceed the annual exemption limit. If you are liable for gift tax, complete Form 709 with your annual tax return.

3. Capital Gains Tax

The state includes capital gains as part of the grantor’s total income tax filing. This means the profit you make by transferring property via a quitclaim deed is taxed at the standard tax rate for your annual income.

Additionally, the IRS charges for long- and short-term capital gains over a certain value. Federal capital gains tax is calculated using your annual income, your profit from the property conveyance, and the length of time you owned the real estate interest.