Navigating the commercial lease process can initially seem challenging, but this guide simplifies it, offering clear, actionable advice for securing the right space for your business. It covers everything from identifying your business’s specific needs to finalizing the lease and preparing for move-in, tailored for anyone looking for office, retail, or industrial spaces.

How to Lease a Commercial Property (as a Tenant)

A commercial lease agreement is a legally binding contract between a landlord and a business tenant, allowing the latter to operate a business from the property.

Whether renting an office, retail space, or healthcare service, you should know the necessary steps to identify, negotiate, and sign a commercial lease.

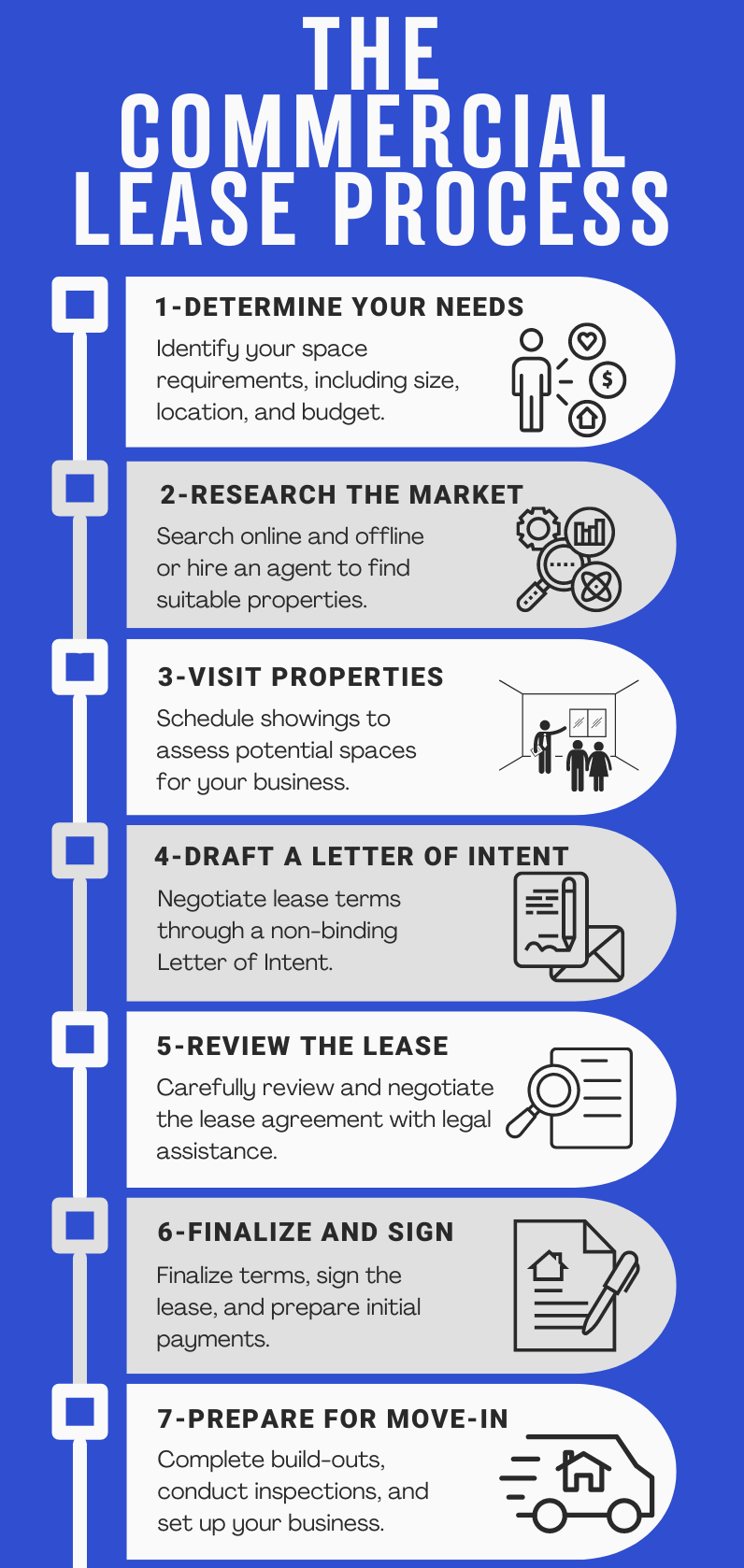

Step 1: Determine Your Needs

Before you start searching for commercial space, it’s crucial to narrow down your specific requirements. Understanding these will help you focus on properties that best suit your business.

- Size of Space: Specify the space required for current and future needs (e.g., a retail store might need 2,000 square feet for product displays and customer flow, while an office might require 1,500 square feet to accommodate desks and meeting rooms).

- Location: Choose a location based on customer proximity, accessibility, parking, and competition (e.g., a restaurant benefits from being in a high foot traffic area with ample parking, while a tech startup might prefer a location near public transportation for employee convenience).

- Type of Space: Match the property type to your business needs (e.g., a medical clinic requires exam rooms and specialized plumbing, while an office space typically needs open work areas and conference rooms).

- Budget: Outline all related costs, including rent, utilities, taxes, insurance, and potential build-out expenses (e.g., a full-service lease might cover utilities and maintenance, while a net lease could require additional costs like property taxes and repairs).

- Accessibility: Ensure the space meets accessibility standards, such as ADA compliance (e.g., a retail store must have ramps and wide aisles for wheelchair access, while an office may need accessible restrooms and elevators).

Step 2: Research and Explore the Market

Once you’ve outlined your needs, it’s time to research the market.

- Online and Offline Searches: To find suitable listings, utilize real estate websites, Google, and print ads. Search for “retail space for rent near me” or “office space near me.”

- Engage a Commercial Real Estate Agent: A commercial real estate broker provides extensive listings, including off-market deals, negotiates for you, offers market insights, and assists with financing options.

Step 3: Visit and Assess Properties

After identifying potential spaces, the next step is to visit these properties to evaluate them against your needs.

- Schedule Showings: Arrange property tours with the listing agent or landlord. Bring your real estate agent or a knowledgeable team member to ask the right questions about the property’s condition, amenities, and terms.

- Property Evaluation: During the visit, assess the property’s suitability for your business. Check the layout, building condition, and any necessary modifications. Consider how the space can be adapted to fit your operational needs.

Step 4: Draft a Letter of Intent

Before committing to a lease, you should negotiate the major terms through a letter of intent (LOI) for real estate.

- Purpose of LOI: An LOI outlines the basic terms of the lease, such as rent, lease duration, and any tenant improvements or allowances. It’s not legally binding but serves as a foundation for drafting the lease agreement.

- Negotiation: Use this opportunity to negotiate favorable terms. You can discuss the lease rate, rent increases, length of the term, and other key aspects like a tenant improvement allowance.

Step 5: Review and Negotiate the Lease Agreement

Once the LOI is finalized, the landlord will draft a lease agreement that includes all the terms agreed upon.

- Lease Review: Carefully review the lease document, paying attention to details like the rent amount, lease length, maintenance responsibilities, and any restrictions on how the space can be used.

- Legal Counsel: It’s highly recommended to have a real estate attorney review the lease. This step ensures that the lease is fair and that you understand your obligations and rights.

- Final Negotiations: If there are any terms you’re not comfortable with, now is the time to negotiate. This might include rent adjustments, maintenance duties, or lease renewal options.

Step 6: Finalize and Sign the Lease

After all negotiations are settled and both parties agree on the terms, it’s time to sign the lease.

- Final Checks: Before signing, double-check all details, including financial obligations, the commencement date, and any build-out timelines.

- Security Deposit and Initial Payment: Be prepared to make an initial payment, which often includes a security deposit and the first month’s rent. These terms should have been negotiated earlier and should be clearly outlined in the lease.

Step 7: Prepare for Move-In

With the lease signed, it’s time to prepare to move in and set up your business.

- Build-Outs and Modifications: If tenant improvements were part of your lease negotiation, coordinate with contractors to ensure the space is ready by your target move-in date.

- Final Inspections: Before moving in, conduct a final walk-through with the landlord to ensure all agreed-upon improvements have been completed.

- Moving In: Once the space is ready, you can start the process of moving in, setting up your business operations, and preparing to open your doors.

Conclusion

Navigating the commercial lease process may seem complex, but by clearly identifying your needs and following these steps, you can secure the right space for your business.

This approach helps you make informed decisions, from assessing properties and negotiating terms to finalizing the lease and preparing for move-in. It ensures that your new location supports your business’s success.