A Quitclaim Deed is a legal document used to transfer ownership of real estate from an owner or seller (the “grantor”) to another person or party (the “grantee”).

However, quitclaim deeds do not include protections or guarantees for the person receiving the property. This means that they will only ever get what the seller owns, which may be nothing.

In this post, we’ll explore the key repercussions of a quitclaim deed to help you make informed decisions about property transfers.

Key Takeaways

- A quitclaim deed is used for amending or changing the title to real property.

- It is common for property transfers when no money is being exchanged, like those occurring between family members.

- It doesn’t guarantee the grantor’s ownership of a property; it simply says that if they do own it, they’re giving up those rights.

- General warranty deeds offer the highest level of buyer protection, while quitclaim deeds provide the least amount of protection.

What Is the Purpose of a Quitclaim Deed?

A quitclaim is used when a name has to be added or removed from ownership or no sale (transfer of money) is involved in the property changing hands. Here are some of the most common uses:

- Transferring real estate within a family

- Changing ownership after a divorce or marriage (remove or add a spouse to property title)

- Correcting property title issues or defects (missing signature, wording issues etc)

- Moving property into trusts and estates

- Moving property into business entities

- Avoiding the probate process when transferring property ownership before someone’s death

Example:

Let’s say John and Sarah are siblings, and they jointly inherited a piece of land from their parents. However, Sarah wants to give up her ownership interest in the property to John. In this case, Sarah would use a quitclaim deed to transfer her interest to John. The document includes names, legal description of the property, and signatures of both parties. No assurances are provided regarding the property’s title and the legal document has to be recorded with the county clerk to finalize the transfer.

The way a quitclaim deed works is that it does not guarantee the grantor has a full property ownership interest. That’s why buyers and sellers often use warranty deeds to transfer property. Knowing the differences between these and other deeds can protect you from risky property transactions.

Any new deed must be filed with the county clerk’s office in order to create a public record of the property transfer. This establishes ownership rights and prevents any disputes that may arise in the future.

Repercussions of a Quitclaim Deed

While a quitclaim deed can be effective in certain situations, it’s crucial to understand the potential repercussions that accompany its use.

1. Lack of Warranty Protection

One of the significant repercussions of a quitclaim deed is the absence of warranty protection. They offer no buyer protection and do not guarantee that the interest in the property is indeed valid.

A warranty deed, on the other hand, guarantees that the grantor has legitimate ownership and that there are no liens or encumbrances on the property. There are two types of warranty deeds:

- General warranty deed: The seller guarantees that they have the legal right to sell the property and that the buyer will receive a title free of debt, claims, or other legal encumbrances.

- Special warranty deed: The seller guarantees against issues or encumbrances in the property title that arose only during the ownership.

Quitclaim deeds offer no guarantees, so the new owner must assume all risks related to the property’s title when signing the quitclaim deed form, including any outstanding liens or legal issues.

2. Potential Title Issues

A quitclaim deed typically includes a legal description of the property and outlines the involved parties. Due to the lack of thorough real estate title searches or title insurance associated with quitclaim deeds, there is an increased risk of undiscovered property title issues.

This means the grantee may be responsible for addressing any existing liens, mortgages, or other claims on the property. If these exist, it could potentially lead to unanticipated financial obligations or legal disputes for the grantee. This is particularly relevant if the grantee decides to sell the real property in the future.

Example:

Alex used a quitclaim deed to transfer property to Sam. Years later, when Sam tried to sell the property, the title company found an unresolved lien on the house.

Sam tries to contact Alex for clarification, but Alex has since moved away and changed their contact information. Without Alex’s cooperation or documentation to prove the legitimacy of the initial transfer, the title company hesitates to provide title insurance to the new buyer. As a result, Sam faces significant challenges in completing the sale.

Therefore, it is imperative to complete due diligence and ensure the property has a clear title before accepting property through a quitclaim deed. Before signing a quitclaim deed, the grantee can choose to do a title search to avoid future problems.

In Texas, for example, title companies and insurers often refuse to insure quitclaim deeds because buyers are held responsible for any title defects, even undisclosed ones. This means a prior unrecorded transfer can supersede a quitclaim transfer without the buyer’s knowledge.

3. Inadequate Protection for Grantees

Although a quitclaim deed allows the grantor to transfer their interest in the property, the grantee (or buyer) receives little protection from it. The new property owner has limited legal remedy against the previous owner in cases of disagreements or title problems involving the property.

Quitclaim deeds are less suitable for real estate purchases because of the following risks:

- No guarantees of ownership

- No title insurance

- Undisclosed liens or encumbrances

- Limited remedies for grantees

As such, grantees should be cautious of using quitclaim deeds in any real estate transaction.

4. Mortgage and Financial Obligations

Transferring property through a quitclaim deed does not absolve the grantor of any existing mortgage or financial obligations tied to the property. Any unpaid loans or debts related to the property still fall under the grantor’s control following the transaction.

Both parties must properly communicate these commitments to prevent issues or misunderstandings as they transfer ownership from the current owner to the new owner.

If the grantor relies on the grantee to make mortgage payments after a quitclaim, they have no recourse if payments cease or the property is sold. To mitigate risks, the grantee can assume the mortgage (with lender approval) or refinance. In this case, a legally binding agreement can be drafted to protect the grantor’s interests.

Options for Removing the Grantor from a Mortgage

There are limited ways to remove the grantor from a mortgage without paying it off. One option is a Deed in Lieu, where the borrower transfers ownership of the property to the bank, and the lender removes the mortgage. However, this doesn’t guarantee protection from liens and encumbrances, so lenders are often hesitant to accept it.

Another method is through assumptions, which are allowed by lenders on FHA, VA loans, and adjustable-rate mortgages. The new borrower applies to take over the loan, and if accepted, the property can be deeded to them, removing the previous owner from both the mortgage and title. Assumptions were common in the 1980s, when interest rates were high, but not so much anymore.

5. Family and Relationship Dynamics

Quitclaim deeds are often used to transfer ownership from one family member to another or between parties with a certain level of trust. However, these transactions can have significant repercussions on family dynamics and relationships.

Conflicts can arise among family members when transferring property, especially if there are questions about the impact on finances or ownership.

Here are some factors that could contribute to family conflicts:

- Unequal Distribution: If one sibling receives the property through a quitclaim deed while the others do not, it may lead to feelings of inequality or unfairness among siblings regarding the distribution of assets.

- Financial Concerns: Other siblings might worry about the financial implications of transferring ownership, such as potential tax consequences or the impact on their inheritance.

- Communication Issues: Lack of communication about the decision to transfer ownership or the reasons behind it could create misunderstandings and resentment among family members.

- Emotional Attachments: Family homes often hold sentimental value, and decisions regarding their ownership can evoke strong emotions. Siblings may have differing opinions on what should happen to the property, leading to conflicts.

To reduce any repercussions, it’s crucial to approach such transactions with open communication, openness, and legal counsel with considerable experience in family law.

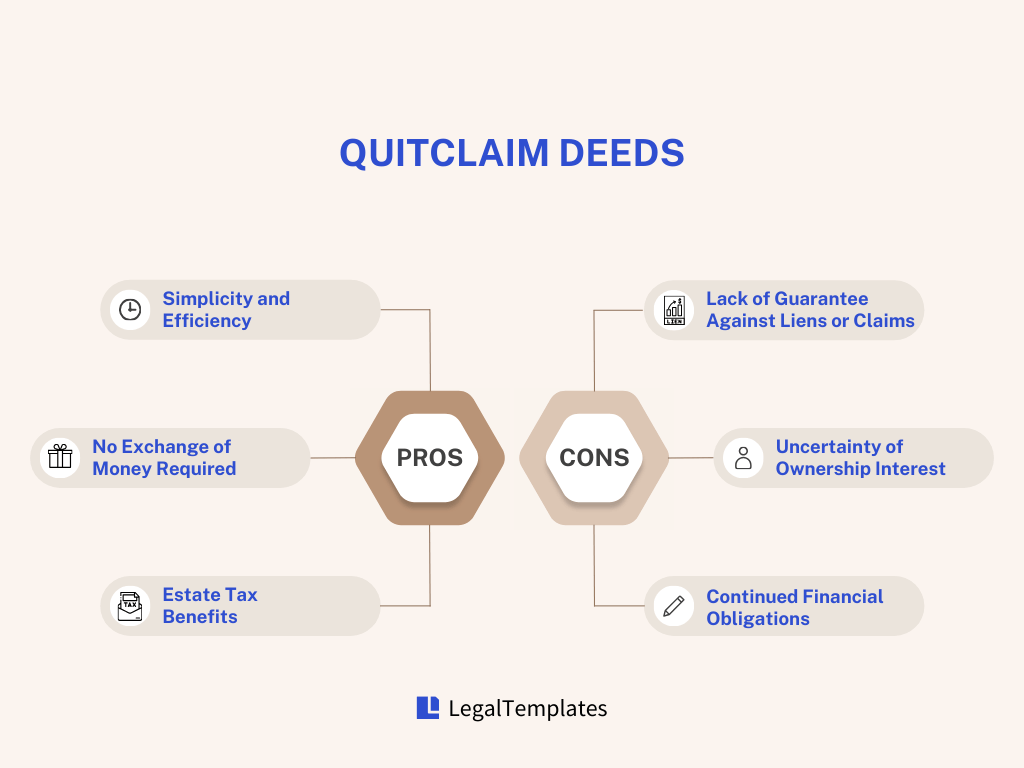

Quitclaim Deed: Risks and Benefits

Benefits:

- Simplicity and Efficiency: Using a quitclaim deed is a straightforward method to transfer ownership of a property from one party to another. Often, all that’s needed is the grantor’s signature and notarization, making the process faster and more cost-effective compared to other transfer methods.

- No Exchange of Money Required: Quitclaim deeds can be employed when transferring property without any monetary exchange. This flexibility is particularly advantageous for transferring ownership to family members or removing the name of a spouse from a property title during a divorce.

- Estate Tax Benefits: Transferring property via quitclaim deed is considered a gift, which can have implications for estate taxes. By transferring ownership as a gift, the value of the property is removed from the grantor’s estate, potentially reducing estate tax liabilities.

Risks:

- Lack of Guarantee Against Liens or Claims: A quitclaim deed offers no guarantee regarding the property’s freedom from liens or claims. Any existing encumbrances on the property will transfer to the new owner upon signing the deed.

- Uncertainty of Ownership Interest: Quitclaim deeds do not ascertain whether the grantor possesses any actual ownership interest in the property. Signing the deed does not transfer ownership if the grantor lacks rightful ownership, potentially leading to legal complications.

- Continued Financial Obligations: Importantly, signing a quitclaim deed does not absolve the grantor of financial responsibilities associated with the property, such as existing mortgages or debts. The grantor remains liable for any debts linked to the property, even after the deed is signed.

Should You Use a Quitclaim Deed?

A quitclaim deed is a simple method to release one’s interest in real property, though it doesn’t detail the specific nature of those rights and comes without any guarantees. Before opting for a quitclaim deed to transfer property, it’s important to understand potential risks and explore other legal documents, like warranty deeds.

If you’re transferring property ownership to a family member or trusted friend, a quitclaim deed might suffice. However, for real estate transactions involving strangers, it is advisable to opt for general warranty deeds or special warranty deeds, which offer more protection and assurances.