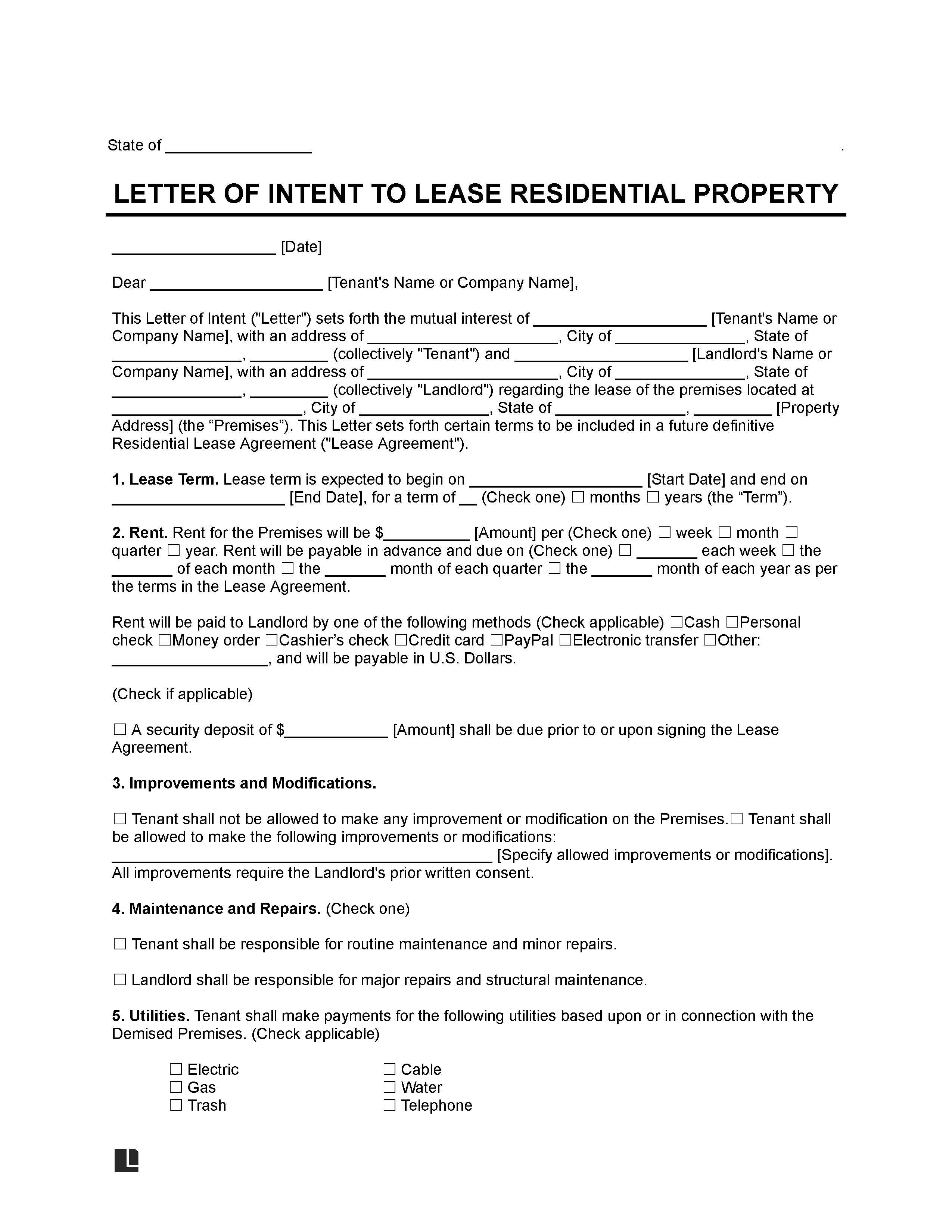

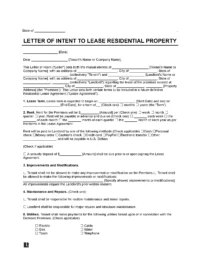

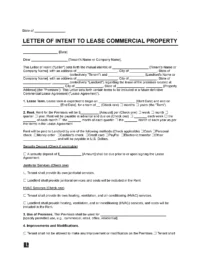

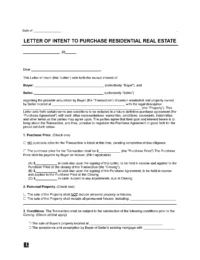

A real estate letter of intent (LOI) serves as a preliminary agreement between prospective buyers or tenants and property owners. This document outlines the fundamental terms and conditions of an offer for a property, facilitating a mutual understanding before formalizing the deal.

The letter signals the applicant’s desire to purchase or lease the property, initiating negotiations. Upon signing, both parties commit to making an effort to reach a final agreement.

Is a Letter of Intent Binding?

- Unlike a purchase agreement, a letter of intent is non-binding, providing flexibility during the initial stages of discussion.

- If the parties decide that the letter is legally binding, this status should be clearly stated in the document. Without this declaration, enforcing the agreement becomes difficult.

By Type

Residential Lease Letter of Intent

For residential property rentals.

Commercial Lease Letter of Intent

For commercial property rentals.

Residential Purchase Letter of Intent

For residential property purchases.

Commercial Purchase Letter of Intent

For commercial property purchases.

When to Use

A real estate letter of intent documents agreed-upon terms without committing to the sale or lease, providing flexibility and room for further negotiation before entering into a binding agreement. It’s commonly used in:

Residential Real Estate: Particularly for high-value residential transactions or scenarios anticipating complex negotiations when leasing property.

Commonly Used Before

Commercial Real Estate: Before finalizing a purchase agreement or entering into a lengthy or complex commercial leasing process.

Commonly Used Before

How Does a Letter of Intent Work?

A real estate LOI serves as a crucial tool for initiating negotiations and formalizing agreements in property transactions. Here’s a guide on how to effectively use one to buy or lease real estate:

Step 1: Property Assessment

The buyer or tenant initiates the process by conducting a thorough property inspection. This involves examining various aspects such as appliances, plumbing, windows, heating systems, and structural integrity for any visible defects.

Step 2: Negotiation Phase

After evaluating the property’s suitability, both parties engage in discussions, often touring the property together to assess its condition, amenities, and potential issues.

Once the assessment is complete, the buyer or tenant drafts an LOI outlining proposed transaction terms, including financial details, completion timelines, and other relevant specifics. Based on this initial offer, negotiations between parties can begin.

Step 3: Formal Agreement Formation

Once the parties have negotiated and reached mutual consent on the essential terms outlined in the LOI, a binding contract, whether a purchase or lease agreement, should be drafted to formalize the agreed-upon terms and conditions.

Purchase agreements typically include an inspection period, allowing buyers to evaluate the property’s condition thoroughly. If the property fails to meet standards or if issues arise during inspection, the buyer may have the option to renegotiate terms or back out of the agreement.

Step 4: Inspection Phase

The inspection period is a standard provision in purchase agreements, allowing buyers a set time to conduct a thorough property examination with the help of a qualified professional. If the property doesn’t meet expectations, buyers can withdraw or renegotiate terms. If satisfied or no inspection occurs, the buyer’s offer is accepted.

Step 5: Closing Process

When buying a commercial or residential property, the closing signifies the official transfer of ownership from the seller to the buyer. Depending on the jurisdiction, this phase may involve various parties, including notaries, escrow companies, and title insurance agents.

Benefits of an LOI

Using a letter of intent in real estate transactions offers several advantages for both buyers/lessees and sellers/lessors:

- Establishes Framework for Negotiations: Outlines the fundamental terms of the proposed agreement, including purchase or rental price, negotiation timeframes, and any essential contingencies. It sets the stage for further negotiations before entering into a binding agreement.

- Affirms Intentions: Demonstrates the seriousness of the buyer’s/lessee’s interest in the property. It solidifies their commitment and distinguishes them from other potential parties.

- Reduces Legal Risks: Clear delineation of terms helps minimize misunderstandings and disputes during the transaction process. It provides a roadmap for the subsequent formal agreement, reducing the likelihood of conflicts.

- Enables Cost-Effectiveness: LOIs are relatively simple documents, often prepared without the need for extensive legal assistance, reducing transaction costs.

How to Write a Real Estate LOI

Whether you’re a buyer, seller, lessee, or lessor, here’s a guide on how to draft a compelling and effective LOI:

Step 1: Define the Parties Involved

1. Begin by clearly stating the contact information of all parties involved in the transaction, including buyers, sellers, lessees, and lessors. If applicable, include details of any brokers representing the parties.

(State Name)

(Date)

(Buyer or Lessee)

(Seller or Lessor)

Step 2: Specify Property Details

2. Describe the property for sale or lease in detail, including the address, square footage, and any unique features or landmarks nearby. This helps ensure clarity and avoid confusion during negotiations. If the seller uses an agent to market the property and negotiate with buyers, a real estate listing agreement can define the agent’s services, commission, and authority before offers or LOIs come in.

Dear (Seller or Lessor Name),

This Letter of Intent (this “Letter”) sets forth the mutual interest of (Buyer or Lessee Details) and (Seller or Lessor Details) regarding the possible acquisition/lease by Buyer/Lessee (the “Transaction”) of certain real property owned by Seller/Lessor located at (Property Address) with the legal description (The precise location and Measurement of the “Property”).

Step 3: Outline Financial Terms

3. Clearly state the proposed purchase price for the property, if currently listed.

Purchase Price/Rent Amount (Check one)

☐ NO purchase price/rent amount for the Transaction is listed at this time, pending completion of due diligence.

☐ The purchase price/rent amount for the Transaction shall be (the “Purchase Price or Rent Amount”).

4. Specify the amount of any deposit and outline how it will be held in escrow, including the duration and conditions.

The Purchase Price or Rent Amount shall be payable by Buyer/Lessee as follows: (Fill if applicable)

(A) ($ amount) in cash due upon the signing of this Letter, to be held in escrow and applied to the Purchase Price at the closing of the Transaction (the “Closing”).

(B) ($ amount) in cash due upon the signing of the Lease or Purchase Agreement, to be held in escrow and applied to the Lease or Purchase Price at the Closing.

(C) ($ amount) in cash, subject to any adjustments, due at Closing.

5. Detail the type of personal property the transaction further includes.

Personal Property. (Check one)

☐ The sale/lease of the Property shall NOT include personal property or fixtures.

☐ The sale/lease of the Property shall include all permanent fixtures (List everything included).

Step 4: Establish Transaction Terms

6. List any conditions that must be met before the purchase of real property, such as property inspections, title searches, or zoning approvals.

The Transaction shall be subject to the satisfaction of the following conditions prior to the Closing: (Check all that apply)

☐ The sale of Buyer’s property located at (Address).

☐ The acceptance and assumption by Buyer of Seller’s existing mortgage with (Financial institution), dated (Date) with a present balance of $ (The existing balance).

☐ Buyer’s ability to obtain a firm commitment for a mortgage loan.

☐ An appraisal on the Property equaling or exceeding the Purchase Price.

☐ An inspection of the Property and Buyer’s satisfaction with the condition of the Property.

☐ Seller’s required disclosures to Buyer, including the disclosure of any known defects in the Property that materially affect the value of the Property.

☐ A title insurance policy in the name of Purchaser.

7. Define the timeframe for finalizing the transaction for the property, during which the buyer can assess the property’s condition and feasibility. For rentals, this would either be the start date of the term or occupancy date.

The Closing of the Transaction shall occur on or before (Closing Date). Seller shall pay the following costs associated with the Transaction (Detail costs). Buyer shall pay the following costs associated with the Transaction (Detail costs).

8. Include provisions related to exclusivity and maintaining the confidentiality of sensitive information exchanged during negotiations.

Seller or Lessor agrees that it will not negotiate directly or indirectly with any other party concerning the sale/lease of the Property (Check one) ☐ for a period of (No. of days) after the date of this Letter ☐ while this Letter is effective and shall immediately terminate any and all existing discussions or negotiations with any party other than Buyer/Lessee.

The parties agree to apply strict confidentiality to the existence and the contents of this Letter, including any information shared or obtained in accordance with this Letter.

Step 5: Determine Binding Status

9. Clarify whether the LOI is intended to be legally binding or non-binding. If certain sections are binding, explicitly state so within the document.

This Letter is intended only as a reflection of the intention of the parties, and neither this Letter nor its acceptance shall constitute or create any legally binding or enforceable obligation on any party, except with regards to paragraphs regarding Exclusivity of this Letter, Confidentiality, Governing Law and Termination hereof.

10. Set a deadline for the LOI’s validity, after which it will expire if no agreement is reached.

This Letter will automatically terminate upon the earliest of:

(A) the execution of the Purchase or Lease Agreement by the Parties

(B) the mutual written agreement of Buyer and Seller/ Lessor and Lessee

(C) (Specific Date)

(D) Other

Step 6: Consider Additional Provisions

11. Include any other terms or conditions relevant to the transaction that have not been addressed previously. Ensure that all aspects of the agreement are clearly defined and mutually understood.

12. Specify the jurisdiction and governing law that will apply to the transaction, particularly if the parties are located in different states or countries.

This Letter and all matters related thereto shall be governed by and construed in accordance with the laws of the State of (Name) without giving effect to its conflict of laws principles.

Step 7: Sign the Document

13. Provide signature lines for all parties involved, indicating their acceptance of the terms outlined in the LOI. Include printed names and dates alongside signatures to formalize the agreement.

Frequently Asked Questions

Can I use a letter of intent to express interest in multiple properties?

Yes, you can use a letter of intent to express interest in multiple properties simultaneously. Since LOIs are typically non-binding, they offer buyers and lessees the flexibility to explore multiple options concurrently without being legally committed to any single property.

However, it’s essential to customize each LOI to reflect the specific details and conditions relevant to each property. This allows buyers or lessees to tailor their offers and negotiate terms based on the unique characteristics of each potential transaction.

What happens after both parties sign the letter of intent?

Once the LOI is signed, the parties may engage in due diligence, where the buyer or lessee conducts further investigation into the property to ensure it meets their requirements and expectations.

During this period, the buyer or lessee may review financial records, conduct property inspections, and assess any legal or environmental issues associated with the property. Simultaneously, the seller or lessor may provide additional documentation and disclosures as required.

Can I back out of a real estate transaction after signing a letter of intent?

Generally, LOIs are considered non-binding agreements, meaning they do not legally obligate either party to complete the transaction. However, certain provisions within the LOI, such as exclusivity clauses or confidentiality agreements, may have binding effects.

It’s essential to carefully review the language and seek legal advice if needed to understand your rights and obligations. Additionally, if you wish to back out of the transaction after signing the LOI, it’s typically advisable to communicate your intentions with the other party promptly and in writing to mitigate potential misunderstandings and facilitate the resolution of any disputes that may arise.