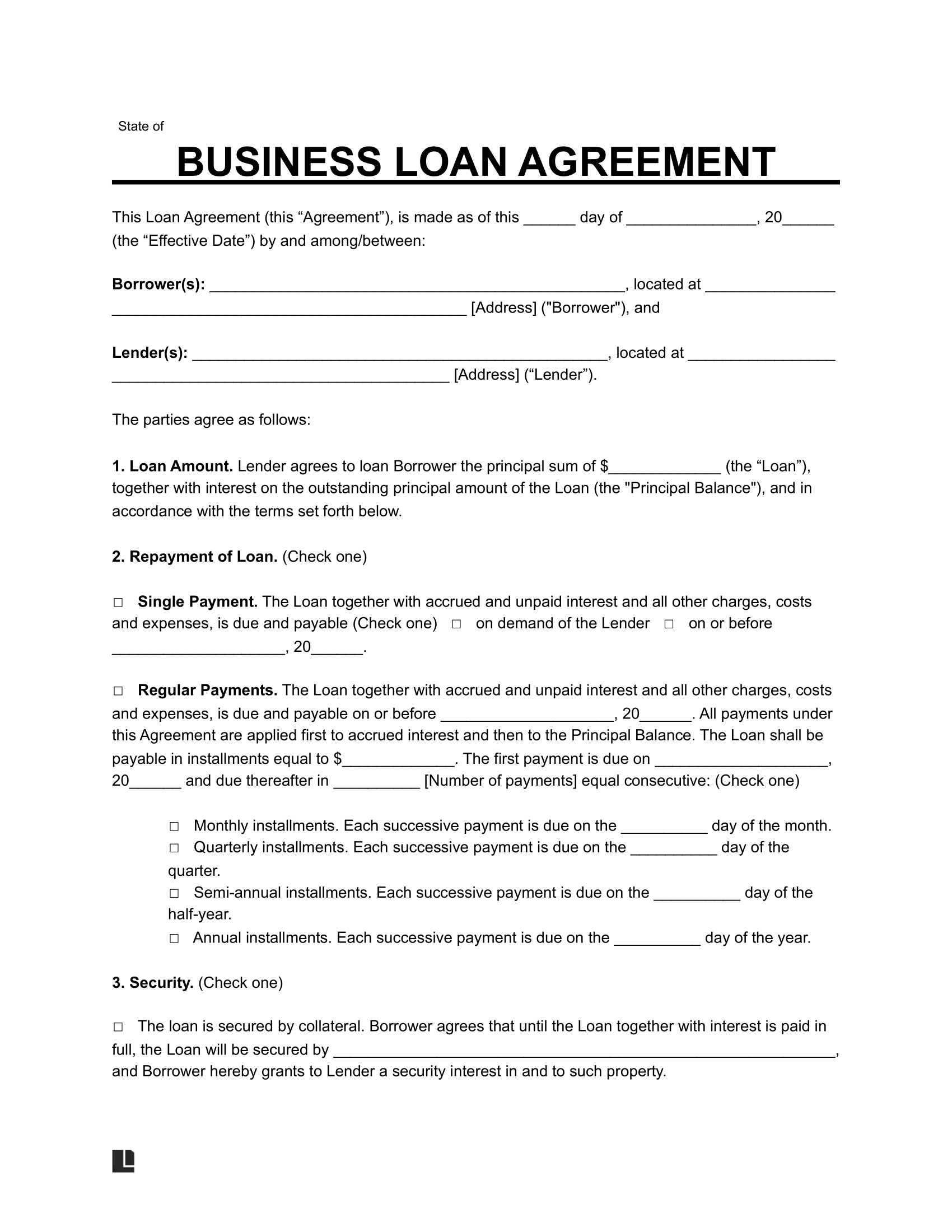

What Is a Business Loan Agreement?

A business loan agreement is a contract between a lender and a business borrower that outlines the terms of a loan. It lays out how much is being borrowed, when and how it will be repaid, and what happens if payments are missed. Whether you’re lending or borrowing money, this document protects both parties and sets clear expectations.

Use a business loan agreement whenever:

- A private investor or financial institution lends money to a business

- You’re loaning funds to a friend or partner’s business and want a clear repayment plan

- Your business needs funding for equipment, expansion, or managing cash flow

Having everything in writing helps prevent disputes and ensures both sides understand the terms.

Most lenders expect a solid business proposal or business plan as part of your loan application.

How to Write a Business Loan Agreement

Use our business loan agreement template to start writing your contract today. Simply follow the steps below to create a clear and concise loan agreement:

1. Set the Effective Date

Start by adding the date the loan agreement takes effect. This is usually the day both parties sign the document.

2. Identify the Lender and Borrower

Include the full names, business names (if any), addresses, and contact info for both parties. If someone’s signing on behalf of a company, add their name and role.

Lenders often review both personal and business credit reports, which can be accessed through agencies like Experian or TransUnion.

3. Add Cosigner or Guarantor Details (if applicable)

If someone is guaranteeing the loan personally, add their full name and contact details. This person agrees to take responsibility if the borrower doesn’t repay. The business owner may also personally guarantee the loan in order to provide an extra layer of security if the business later fails.

4. State the Loan Amount

List the total amount being loaned; this is the principal. Make sure the number is accurate and written in both words and numerals.

5. Specify the Purpose of the Loan (optional)

You can include how the borrower plans to use the money, such as for buying equipment, covering payroll, or starting a new venture.

If you’re using a loan to buy a business, consider attaching a letter of intent to explain your purchase plans.

6. Define the Interest Rate

State whether the interest is fixed (stays the same) or variable (can change). Also include the annual percentage rate (APR).

7. Create a Repayment Schedule

List when the borrower will make payments (monthly, quarterly, etc.) and how much each payment will be. Include the loan’s start and end dates.

8. Include Amortization Details (if applicable)

If the loan includes fixed payments over time, you should attach an amortization schedule showing payment breakdowns. Include acceleration clauses if desired, stating future events that will cause the entire loan to become due at once, such as a breach of the agreement’s terms.

9. Identify Collateral or Security

Note any property or assets the borrower is putting up as collateral. This gives the lender a claim to those assets if the borrower defaults.

If the loan is tied to specific assets, include an asset purchase agreement.

10. Outline Default Conditions

Explain what counts as a default (such as missing one or more payments), and what the lender can do if that happens, including demanding immediate full repayment. Include whether there will be a grace period to make any missed or late payments before default occurs.

In case of missed payments, a lender might issue a demand for payment letter before pursuing legal action.

11. Add Late Payment Terms and Penalties

State any late fees or penalties if payments aren’t made on time. You can also include grace periods if allowed.

12. Determine Prepayment Conditions

Decide whether the borrower can pay off the loan early, and whether there’s a penalty or discount for doing so.

13. Choose Governing Law and Jurisdiction

Specify which state’s laws apply to the loan agreement and where any legal disputes will be handled.

14. Set Dispute Resolution Method

Include how disputes will be handled, such as through court, mediation, or binding arbitration. You may also wish to include language regarding payment of the prevailing party’s legal fees in the event of a dispute.

15. Include Signature Lines for All Parties

Each party must sign and date the agreement. Make it clear who is signing on behalf of a business and who is signing as a personal guarantor.

16. Add Notary or Witness Section (if needed)

In some cases, a notary or witness signature may be required for extra legal assurance.

Business Loan Agreement Sample

Below is an example of a completed business loan agreement. When you’re ready, you can customize our simple business loan agreement template. Simply fill out each section and then download in PDF or Word format.