What Is a 50/50 Partnership Agreement?

A 50/50 partnership agreement is a legally binding document that outlines the terms of a business partnership where each partner shares ownership, responsibilities, profits and losses equally.

This type of agreement is common among entrepreneurs and small business owners who want to:

- Establish clear roles and expectations.

- Avoid misunderstandings about decision-making.

- Protect both partners if disputes arise.

When to use a 50/50 partnership agreement:

- You and another individual are starting a business together with equal investment and shared risk.

- You want a simple way to define each partner’s duties, contributions, and profit distribution.

- You aim to formalize your arrangement to avoid personal liability issues.

How to Write a 50/50 Business Partnership Agreement

Creating a thorough 50/50 partnership agreement ensures both partners understand their obligations and how to handle situations if a dispute arises. Our template makes it easy and covers all of the below. Here’s what to include in your agreement:

1. Basic Details

List the names and addresses of each partner and your business. Specify your business’s name, type (e.g., LLC, general partnership), its date of creation, and purpose.

2. Capital Contributions

Detail what each partner is contributing. This might be:

- Cash investments

- Equipment or property

- Services or intellectual property

State that these contributions result in equal 50/50 ownership.

3. Profit and Loss Sharing

Explain that profits and losses will be split 50/50 between partners. Specify how and when profits will be distributed.

4. Roles and Responsibilities

Outline each partner’s day-to-day duties and decision-making powers. Even in a 50/50 arrangement, partners may handle different aspects of the business.

5. Decision-Making and Disputes

Explain how decisions will be made. Common approaches include:

- Unanimous agreement: Both partners must agree.

- Designated authority: Each partner handles different types of decisions.

Include a process for resolving disputes, such as mediation or arbitration.

If disputes become serious, you may want to dissolve the partnership. Use our partnership dissolution agreement to establish a clear process to wrap things up. Without an agreement, dissolution will depend on your state’s default laws.

If you ever need to modify your partnership, a partnership amendment template is the proper tool to update your terms.

6. Banking and Records

Clarify how business accounts will be managed and who can sign checks. Require accurate records and set a schedule for reviewing finances.

7. Duration and Exit Terms

Define how long the partnership lasts (often “until terminated by mutual agreement”) and outline what happens if one partner wants to leave or if the business closes. Include buyout provisions.

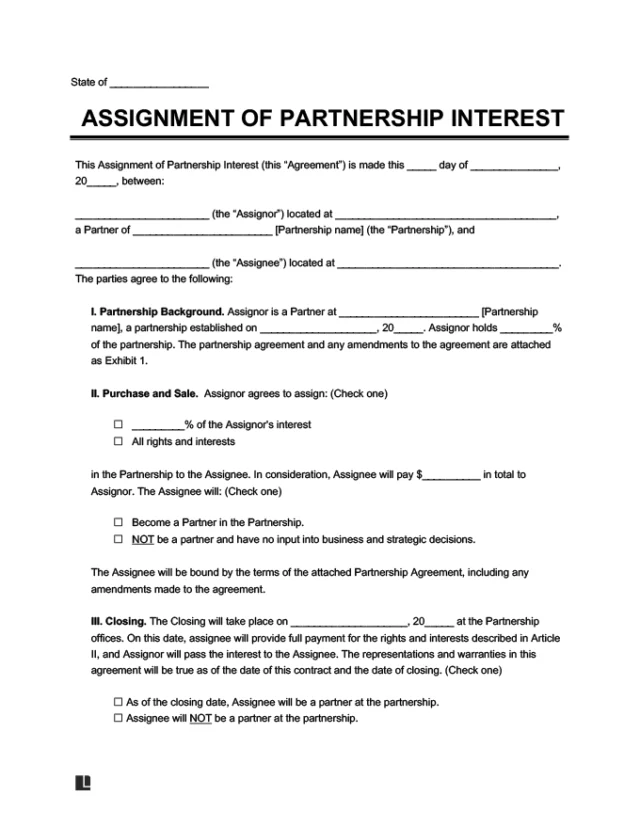

If one partner transfers their interest, protect the business with an assignment of partnership interest agreement.

8. Signatures

Both partners must sign and date the agreement. Notarizing your signatures can add an extra layer of protection. Use a notary acknowledgment form to confirm identities and signatures.

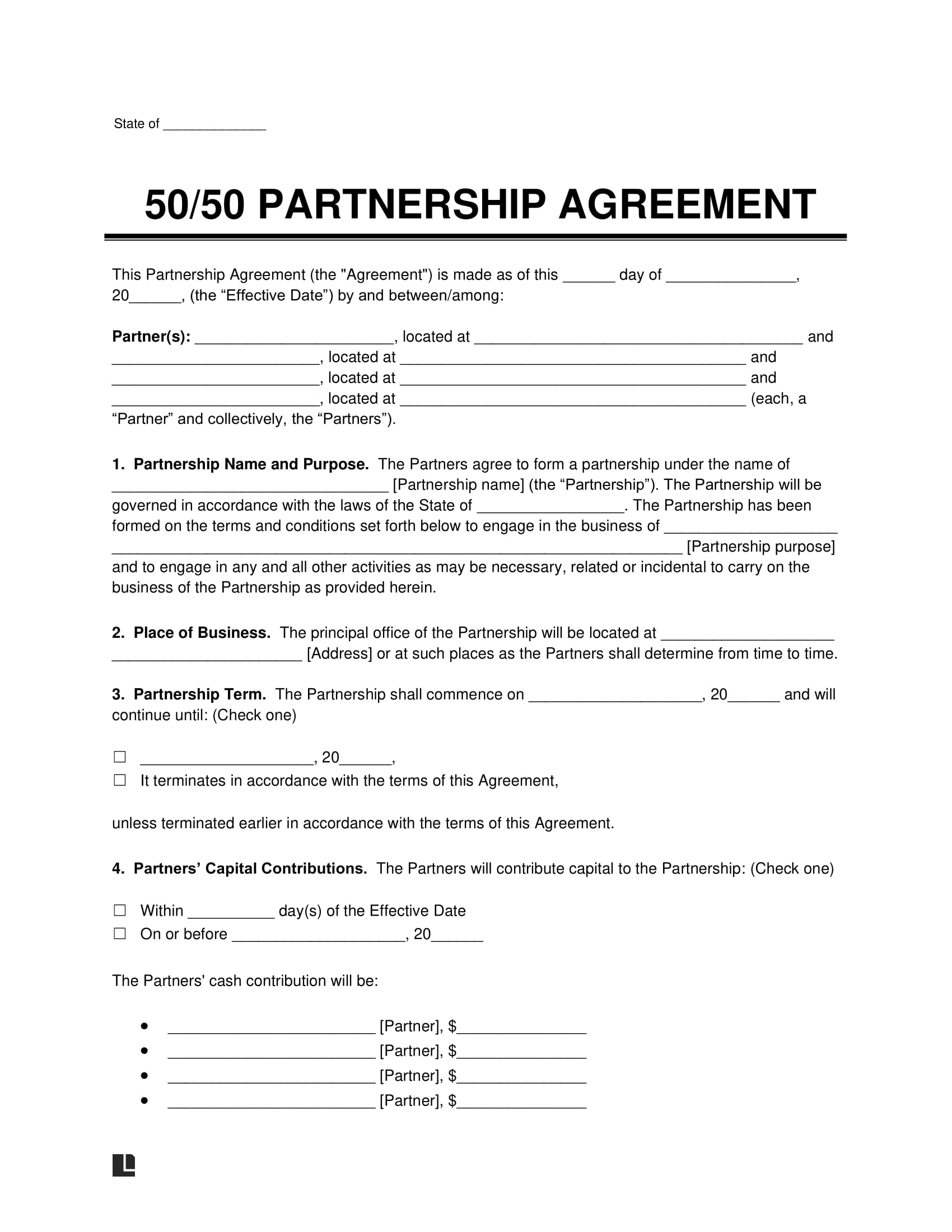

Partnership 50/50 Agreement Sample

If a partnership seems like the correct form of organization for your business, you can use our 50/50 partnership agreement template: