What Is a Delaware Promissory Note?

A Delaware promissory note documents a loan between a lender and borrower and is aimed at facilitating the timely repayment of the loan balance. The form requires specific details for validation, including the parties’ names and addresses, interest rates, and payment terms.

Additional clauses, such as prepayment, acceleration, payment allocation, severability, and notice, may also be included. This type of document can be issued by individuals, companies, or financial institutions and is commonly used for lending smaller amounts of money.

Laws: While there isn’t a specific statute dedicated solely to promissory notes in Delaware, several articles apply to their interpretation and enforcement. These include Article 3 of the Uniform Commercial Code, which contains provisions regarding such negotiable instruments, and Article 9, which references secured promissory notes.

Statute of Limitations: Six years (§ 8109).

Types of Delaware Promissory Notes: Secured vs. Unsecured

Delaware promissory notes can be either secured with collateral or unsecured, offering different levels of protection and risk for the lender.

Secured Delaware Promissory Note

Provides protection against financial loss by securing the borrower's valuable possessions in the event of a default on the loan.

Unsecured Delaware Promissory Note

Since there is no security in the event of a default, the lender should verify the borrower's reputable credit and trustworthiness.

Usury Laws and Interest Rates in Delaware

Promissory notes must adhere to the state’s usury laws in the Delaware Code, Title 6, Chapter 23.

- Loans Insured by the Federal Housing Association (§ 2301(a)): Not more than 5% over the Federal Reserve discount rate.

- For Unsecured Loans Over $100,000 (§ 2301(c)): No maximum.

- For Life Insurance Policy Loans (§ 2911(b)(1)): Not more than 8% per annum or an adjustable legal maximum if there is a provision in the contract.

- For Secured Pawnbroker Loans (§ 2316): Not more than 30% per month.

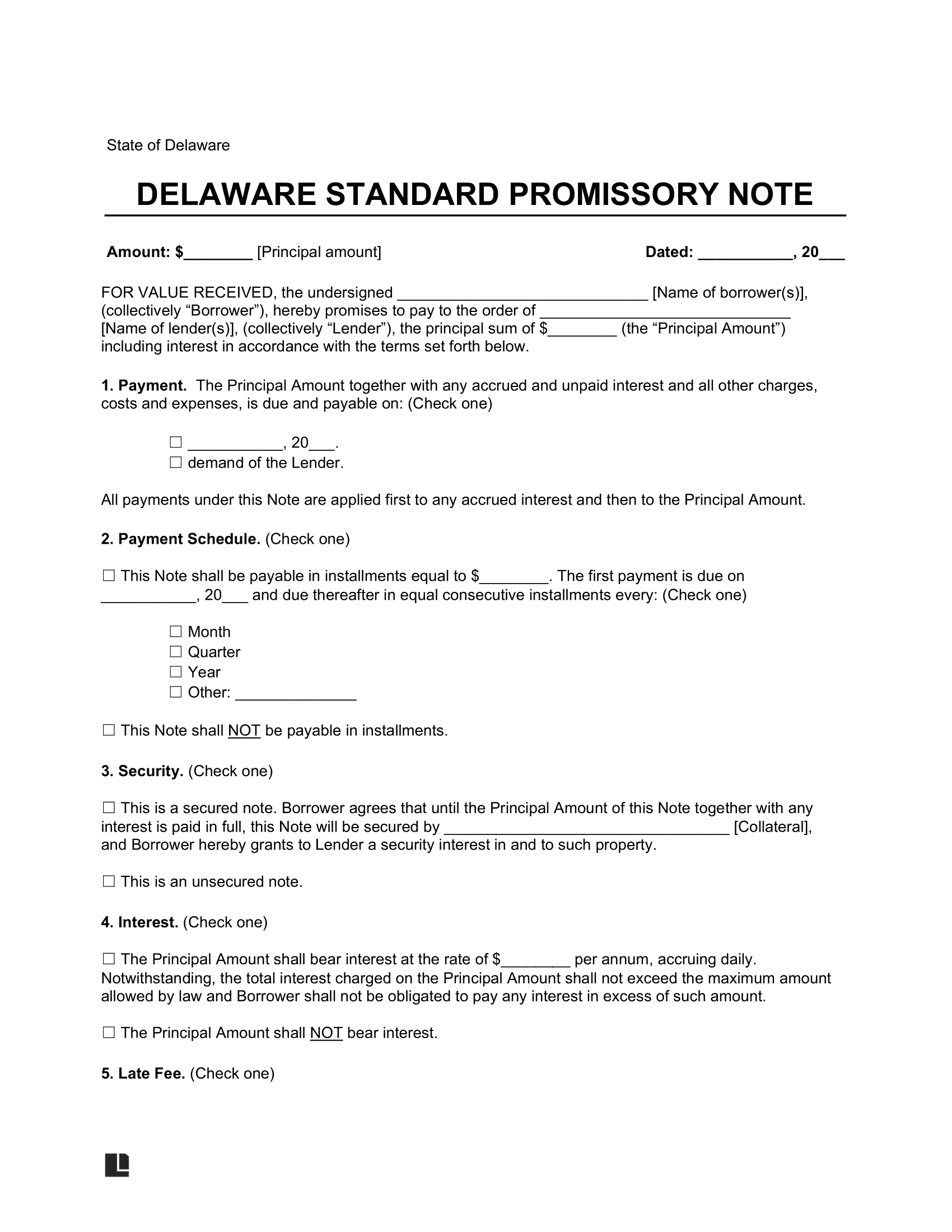

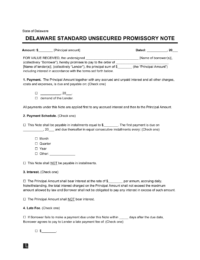

Sample Delaware Promissory Note

Below, you can see what a Delaware promissory note looks like. You can customize this template using our document editor and then download in PDF or Word format.