What Is a Hawaii Promissory Note?

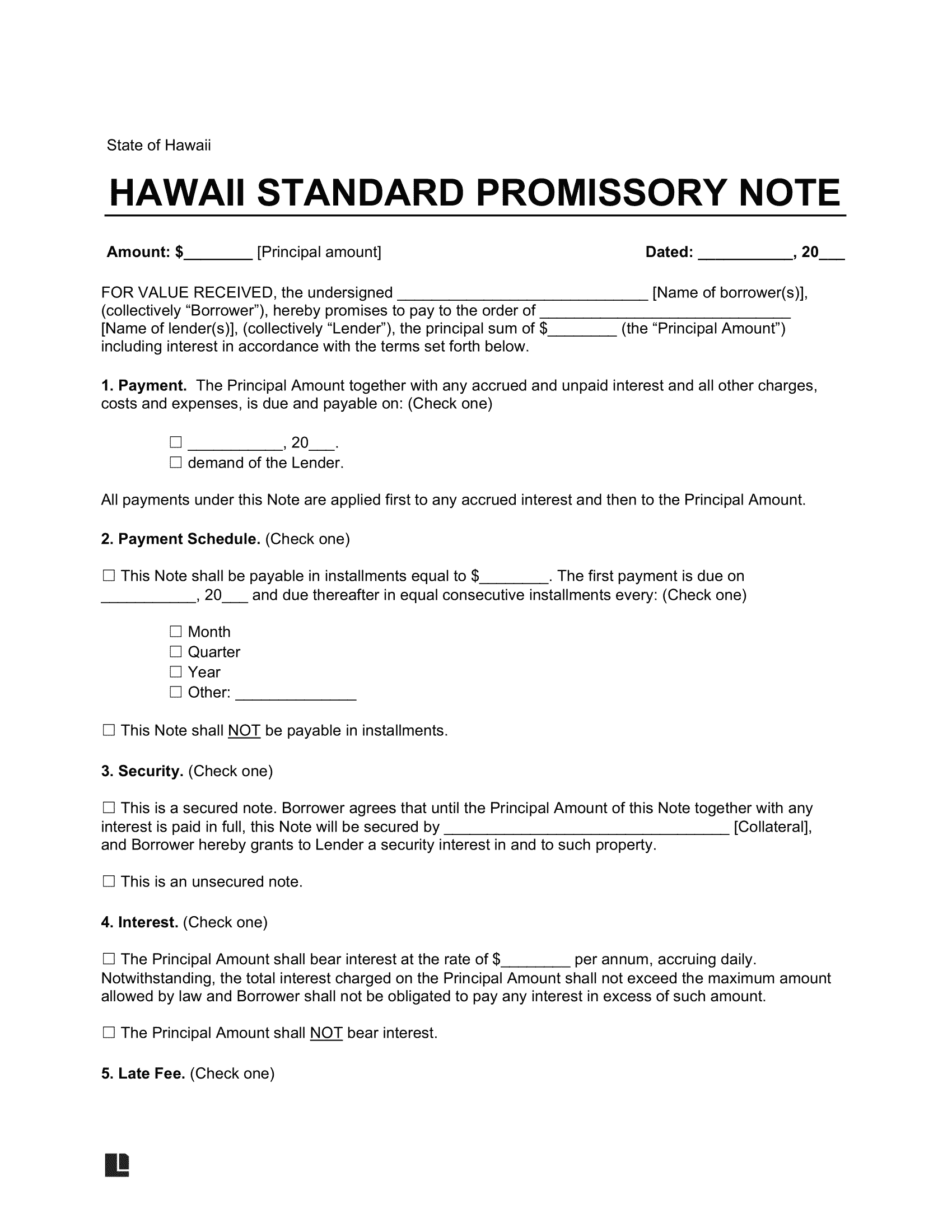

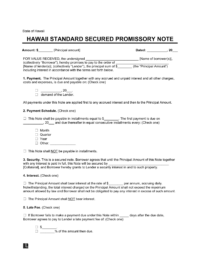

A Hawaii promissory note is a formal agreement delineating the repayment terms for a debt owed to a lender. Upon signing, the borrower commits to repaying the lender by a specified deadline, including accrued interest, as outlined in the note.

This legally binding document defines loan particulars, covering payment plans and penalties for late or missed installment payments. It can be structured as either secured or unsecured, offering adaptable options to suit the needs of both parties involved.

Laws: Commercial promissory notes in Hawaii are regulated by Article 3 of the Uniform Commercial Code (490:3) and Hawaii common law. Additionally, they are subject to regulations concerning collections and interest rates.

Statute of Limitations: Six years (§ 657-1(1)).

Types of Hawaii Promissory Notes: Secured vs. Unsecured

In Hawaii, a promissory note may include collateral for added lender protection or be issued without it, depending on the terms of the agreement.

Secured Hawaii Promissory Note

Provides lender security in case of borrower default by agreeing on collateral items before the agreement is signed.

Unsecured Hawaii Promissory Note

Doesn't require the borrower to offer collateral to the lender.

Usury Laws and Interest Rates in Hawaii

Promissory notes must comply with the state’s usury laws defined by the Hawaii Revised Statutes, Title 26, Chapter 478.

- In General (§ 478-2): 10%, unless a written contract establishes a different rate, in which case the interest rate cannot surpass the contract rate.

- For Judgments (§ 478-3): 10% for civil suits.

- For Home Business Loans (§ 478-4): *1% per month or 12% per year unless the creditor is regulated by state law, then not to exceed 2% per month or 24% per year.

- For Consumer Credit Transactions (§ 478-4): *1% per month or 12% per year, with the exception of credit card agreements.

*When the lender is a financial institution other than a credit union or trust company, the highest permissible interest rate is 2% per month or 24% per year.

Sample Hawaii Promissory Note

Below, you can see what a Hawaii promissory note looks like. You can customize this template using our document editor and then download in PDF or Word format.