When you file a quitclaim deed in Oklahoma, you may be asked to pay recording fees and transfer taxes at the time of recording. Depending on the details of your transaction, you may also owe state and federal taxes for gifts and capital gains when you file your annual income tax return.

Filing a quitclaim deed in Pennsylvania can mean considerable associated costs and fees for both the grantor and the grantee. Make sure you are prepared for the financial considerations associated with the property transfer.

Filing Fees

Each county in Pennsylvania has the right to set its own fees for filing a quitclaim deed. In Elk County, for example, the filing fee is $78.75. On the other hand, the base fee for a deed in York County is $85.25. Always check your county for any expected fees.

Taxes

The taxes associated with a real estate transfer are essential to the financial obligations related to selling or gifting a property.

Real Estate Transfer Tax

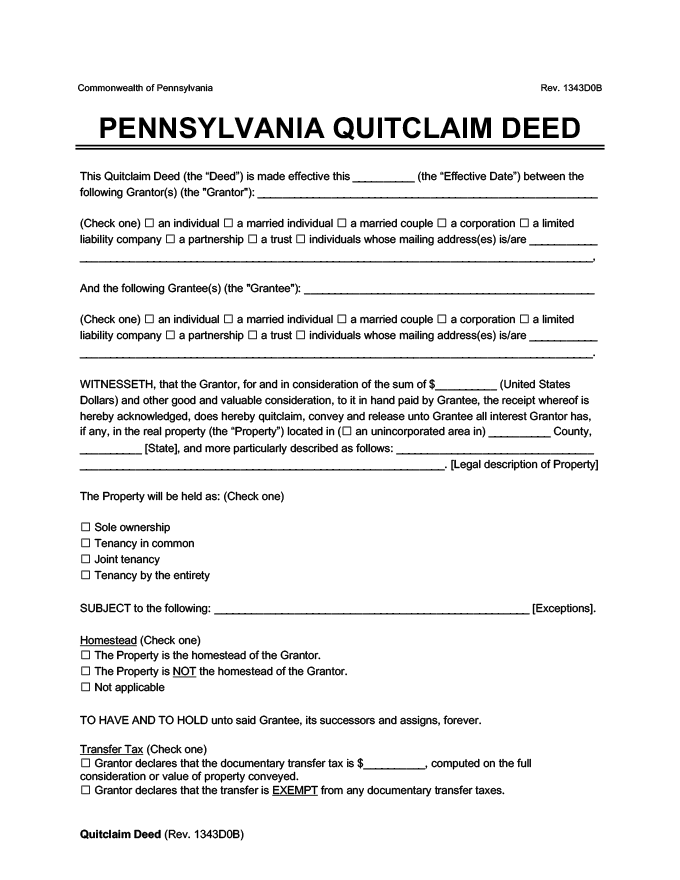

Pennsylvania has a 1% transfer tax for real estate transactions.

Exemptions to the Transfer Tax

There are several exemptions to the transfer tax in Pennsylvania, including:

- Easements for agricultural, preservation, or conservation transferred to or from the commonwealth, a county, a local government unit, or a conservancy

- Historic easements

- Transfers to or by land banks

- Transfers to or from the United States government or the Pennsylvania Commonwealth

- Part of a bankruptcy plan

- Transfers between husband and wife

- “Lineal ascendants and descendants,” including transfers between parents, grandparents, grandchildren, etc, and their spouses

- Transfers between siblings

- Individuals and siblings’ spouses

- Previously married individuals who owned the property together during their marriage

- Transfers into or out of trusts

If you believe you may not be subject to a transfer tax under the requirements of P.A. Statute § 91.191, consult an accountant or tax professional to ensure you follow those mandates.

US Gift Tax

The United States gift tax applies to gifts of substantial financial value, including real estate. Because of the significant value of many real estate transactions, including those managed by a quitclaim deed, the grantor should consider the cost of a gift tax when gifting real estate.

While there are exemptions to the gift tax of up to a set amount each year, real estate gifts frequently exceed the exempt amounts. Pennsylvania does not assign a separate gift tax.

Capital Gains Tax

The capital gains tax imposes a tax on the amount the value of the property has increased between the time the current owner bought the property and the time they sell it. The IRS imposes a federal capital gains tax on many property sales, including real estate transactions.

However, exemptions may apply when the grantor has used that property as their primary residence, living there at least two out of the last five years.

Pennsylvania assesses a tax on all income, including capital gains. The state does not consider capital gains separate from ordinary income, so real estate sales will be included under the grantor’s state income for the calendar year in which the property is sold.