A Rhode Island quitclaim deed is a legal document conveying a property title from a grantor to a grantee, but the grantor promises only to defend any claims that originate from the grantor. The grantee must resolve all other claims against the title because this type of deed absolves the other former owners of any responsibility.

How to File

Filing a quitclaim deed in Rhode Island is straightforward with the right preparation. Completing and recording the deed properly helps make the transfer official.

Step 1: Get the Deed

Ask the current owner for a copy of the original deed. If the original deed is unavailable, you can obtain a copy from your city or town property recorder’s office. You may need to consult a title office or a property law attorney to confirm the document is accurate.

Step 2: Verify the Property Description

Refer to the original deed to verify a match between the deed’s property description and the legal description of the property in the recorder’s office.

Step 3: Complete the Form

Write all necessary details, including both parties’ names, the grantee’s full address, and the property’s legal description.

Ask a lawyer for advice or assistance if you have questions about your unique situation.

Step 4: Sign Before a Notary

Sign the form in front of a notary public with proper identification. The Rhode Island Department of State has resources for finding a notary public if you need help locating one.

Step 5: Fill Out a Property Disclosure Statement

Write a property disclosure statement to reveal any material defects, ensuring to abide by RI Gen. Laws § 5-20.8-2. This way, the grantee will know the condition of the property they plan to accept.

Step 6: File the Documents and Pay

File the documents at the recorder’s office in the appropriate city or town. Pay the associated real estate conveyance tax and filing fees. While there are standard state fees that everyone has to pay, you may pay additional fees depending on your city or town’s guidelines.

Step 7: Wait for the Recorder’s Office

The recorder’s office will issue the deed to the grantee when they finish the recording process. The grantor should obtain and keep a copy for their records.

Costs and Fees

In Rhode Island, quitclaim deed transactions often require paying recording fees along with a transfer tax. Understanding these costs will help you budget properly for your property transfer.

Filing Fees

It costs $84 to file the first page and an additional $1 for every subsequent page (RI Gen. Laws § 34-13-7 and RI Gen. Laws § 42-8.1-20).

Taxes

State- and federal-level taxes may apply when using a quitclaim deed.

1. Real Estate Transfer Tax

The real estate transfer tax applies to every deed or other instrument that conveys an interest in real estate. The grantor must pay $2.30 per $500 or each fraction thereof (RI Gen. Laws § 44-25-1). The tax is $1.40 per $500 for mobile or manufactured homes.

Who Pays the Transfer Tax?

The seller or grantor must pay the tax unless there is a contrary agreement with the purchaser or grantee.

Exemptions to the Transfer Tax

The grantor doesn’t have to pay transfer tax for a quitclaim deed in the following circumstances:

- The grantor gives the deed to secure a debt.

- The grantor is the United States, Rhode Island, or a political subdivision thereof.

- There is a qualified sale of a manufactured or mobile home community to a resident-owned organization (outlined in RI Gen. Laws § 31-44-1).

- The transfer occurs among partners, members, or owners in a real estate company with respect to an affordable housing development (only relevant when specific conditions are met).

2. US Gift Tax

The grantor pays gift taxes (Form 709) on any property transfer involving zero consideration. The gift tax will apply even if the grantor didn’t intend the transfer to be a gift, such as an inheritance. The grantor typically pays the tax, but the grantee may pay if the parties agree. Properties may be subject to partial exclusion.

3. Capital Gains Tax

Both state and federal governments may impose taxes on property transfers via quitclaim deeds. The tax is assessed at the sale of the property by the grantee and could be substantial, depending on their basis and the sale price.

Rhode Island treats capital gains tax as ordinary income, so individuals can expect to be taxed between 3.75 and 5.99% (RI Gen. Laws § 44-30-2.6).

Additionally, federal capital gains taxes may apply. The IRS outlines capital gains tax information in Topic No. 409. The grantor must pay any associated capital gains tax if they sell the property for more than what they acquired it for. Grantees must pay capital gains tax if they later sell the property acquired through a quitclaim deed.

Rhode Island Quitclaim Deed Requirements

Rhode Island has certain legal guidelines that quitclaim deeds must meet to be valid and enforceable. Getting the details right can help you complete your property transfer without setbacks.

Legal Framework

A quitclaim deed transfers the grantor’s title interest without warranty as to title. That is, the grantor does not guarantee they have any claim to the title they’re conveying. Quitclaim deeds are useful when the grantee knows that the grantor does own the title they are transferring, such as a divorce in which one spouse transfers ownership of a house or property to the other.

The language for a quitclaim deed is present in RI Gen. Laws § 34-11-12. Your document must contain specific language conveying the title from the grantor to the new owner. It may also include a quitclaim covenant, which lets the grantor promise to defend the new owner against any claims that originate from the grantor only (RI Gen. Laws § 34-11-18).

Legal Description

The grantor must include an accurate legal description of the property for their quitclaim deed to be valid. Rhode Island has no specific requirements for this description in its statutes, but it should include metes and bounds, lot and block, and references to other public records.

Consult a title company, attorney, surveyor, or another professional in your city or town to improve the accuracy of the property’s legal description.

Signing

In Rhode Island, the grantor must sign the document before a notary public (RI Gen. Laws § 34-11-1.1). Without the notary present, the quitclaim deed won’t be enforceable.

Filing

Rhode Island does not have a county recorder’s office. Grantors file quitclaim deeds and all other property transfer documents in the city or town recording office where the property is situated (RI Gen. Laws § 34-11-1). The respective office will return the document to the grantee upon recording.

For recording, a document must:

- Be an original document with all original signatures and seals.

- Have the grantor’s signature notarized.

- Have the grantee’s complete address.

If there is no consideration, the deed must contain the language “Consideration is such that no documentary stamps are required.”

When the consideration is over $100, the conveyance tax rate is $2.30 for every $500, rounded to the nearest $500 (RI Gen. Laws § 44-25-1). Refer to the Rhode Island Conveyance Tax page for the tax due.

Validity Requirements

A valid quitclaim deed appears in writing and meets all of the requirements for recording. A document that doesn’t meet recording requirements is not invalid but may not be recorded, which defeats the purpose of a quitclaim deed.

A testamentary quitclaim deed between a grantor and their heir is valid and legally binding even when not recorded or acknowledged. Such deeds are considered titles regardless of their recording status.

Failure to comply with signing requirements won’t deem the deed invalid, but the instrument’s recording fee will increase by $2 (RI Gen. Laws § 34-11-1.1).

Content Requirements

A quitclaim deed must include the following requirements at a minimum:

- The names of the grantor and the grantee.

- Information about the property being transferred, including the physical address, parcel, and legal description.

- The amount of consideration (purchase price) or a statement saying the grantee didn’t provide consideration.

- The signatures of the parties.

- The signature and stamp of the notary.

Quitclaim Deeds vs. Other Property Transfer Methods in Rhode Island

| Quitclaim Deed | Transfers the grantor's interest to the grantee without any warranties. It may include a quitclaim covenant, allowing the grantor to promise the grantee to defend against claims originating from the grantor. |

| General Warranty Deed | Provides greater protection by transferring the grantor's interest to the grantee and confirming that the title is clear. |

| Deed of Executor, Administrator, Trustee, Guardian, or Conservator | Refers to a type of deed used when an individual transfers property and acts in one of the titular fiduciary capacities. |

| Assignment of Mortgage | Transfers a mortgage loan associated with a property from one lender or mortgage holder to another. |

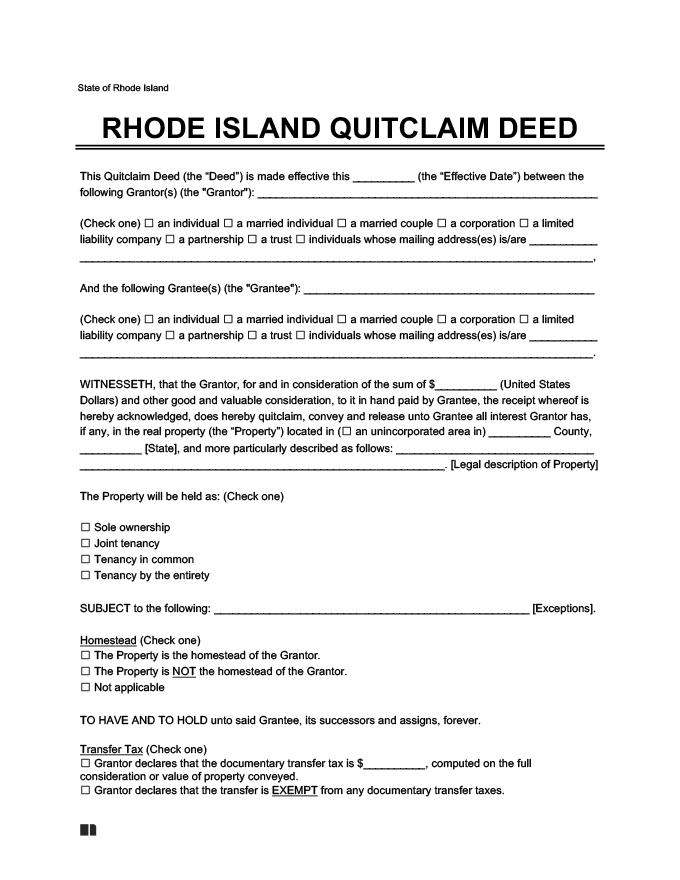

Sample Rhode Island Quitclaim Deed

View our free sample Rhode Island quitclaim deed below. You can easily fill it out and download it as a Word or PDF file.

Frequently Asked Questions

Does a quitclaim deed absolve me of my mortgage obligations in Rhode Island?

A quitclaim deed only transfers the property’s title. Any debts or obligations you have, whether you have them by yourself or with a spouse, are still your responsibility.

Are quitclaim deeds public record in Rhode Island?

Yes. Filing your quitclaim deed at your town or city’s recorder’s office makes the document part of the public record.

How long does it take to record a Rhode Island quitclaim deed?

It depends on the town or city’s population, processes, and procedures. Some recorder’s offices may be able to record it within a couple of weeks, while others may take up to a month or longer.