What Is a Deed of Reconveyance

A deed of reconveyance is a legal document that confirms you’ve fully paid off your home loans and now own the property outright. When you first buy a home with a loan, your lender keeps a legal claim, known as a lien, on your property until the loan is fully paid. In some states, a neutral third party, known as a trustee (for example, a title company or attorney), holds the title to your home during that time.

After your last payment, the lender tells the trustee that the loan is paid off. The trustee then signs and records the deed of reconveyance. This removes the lender’s claim and transfers the property back to you. In other words, while a conveyance transfers property to a new owner, a reconveyance transfers it back to you after your debt is paid.

You should record your deed of reconveyance with your county recorder’s office. This updates public records to show you as the full owner. Recording the deed helps protect your ownership and avoids problems if you sell or refinance later.

Deed of Reconveyance vs. Satisfaction of Mortgage

Depending on your state, this document might have a different name:

- Satisfaction of Mortgage: Used in mortgage states such as Florida or New York. The lender records this document once the loan is paid off, thereby removing their claim on the property.

- Full Reconveyance: Used in trust deed states such as California or Arizona. The trustee records this document after confirming the loan is fully paid to transfer the title back to you.

Both documents show that your loan is fully paid and that your home is officially yours.

What Is the Purpose of a Deed of Reconveyance

You might need a deed of reconveyance in any of the following situations:

- Completion of Mortgage Payments: Once your loan is fully paid, the lender or trustee must record the deed of reconveyance to remove the lien and transfer full ownership back to you. Some states have specific deadlines for this. For example, under a deed of trust in California, the trustee is required to record the reconveyance within 21 days of receiving a written request from the lender (California Civil Code § 2941).

- Private Lending Situations: If you lent money for a property purchase and the borrower has repaid you, the deed of reconveyance ends your legal claim and confirms that the borrower owns the property outright.

- Refinancing a Mortgage: The previous lender must issue a deed of reconveyance to remove their lien before the new lender’s lien is recorded. This step keeps your title clean and prevents any overlapping.

- Trustee Sale or Foreclosure: Recording a deed of reconveyance clears old liens and confirms that the property ownership has been updated.

- Title Disputes and Legal Settlements: This deed can also help settle ownership questions by showing that the lender’s claim has been removed and the title is clear.

The deed of reconveyance acts as proof that your loan is paid off and your title is clear, protecting you from ownership or financing problems.

Reconveyance in Different States

Some states use a deed of reconveyance, while others use a satisfaction of mortgage. Both documents prove that the loan has been paid in full and remove the lender’s claim from the property. Each state may handle property transfers differently. To learn more about other kinds of real estate deeds and how they work, read our guide to different types of deeds.

| State | Document |

|---|---|

| Alabama | Deed of Reconveyance and Satisfaction of Mortgage |

| Alaska | Deed of Reconveyance |

| Arizona | Deed of Reconveyance and Satisfaction of Mortgage |

| Arkansas | Deed of Reconveyance and Satisfaction of Mortgage |

| California | Deed of Reconveyance |

Who Prepares and Signs the Deed of Reconveyance

Preparing a deed of reconveyance involves several key players, each with their own specific responsibilities.

Trustee’s Role

The trustee prepares and signs the deed of reconveyance after the lender confirms that the loan has been fully repaid. This document officially releases the lender’s lien and transfers full ownership rights back to the borrower.

If the original trustee is no longer available, the lender must first file a substitution of trustee to appoint a new one before the deed can be signed or recorded. Once the correct trustee is in place, they sign the deed of reconveyance and ensure it is recorded with the county recorder’s office where the property is located.

Lender’s Role

The lenders, also referred to as the beneficiary, must notify the trustee that the loan has been fully repaid. This gives the trustee permission to prepare and file the deed of reconveyance. State laws often require lenders to act within a specific timeframe. Delays can impact a borrower’s ability to demonstrate clear ownership of their property.

Borrower’s Responsibility

The borrower does not sign the deed of reconveyance, but they still play an important role in ensuring it’s handled correctly. After the deed is recorded, the borrower should confirm it appears in public records under their name.

How to Create and File a Deed of Reconveyance

Once your loan is paid off, it’s important to record your deed of reconveyance quickly to clear the lender’s claim from the property title. Follow the steps below to make sure your deed is prepared and filed correctly.

Step 1 – Confirm the Loan Is Fully Paid Off

Before creating the deed, ensure that your loan balance is fully paid and that the lender has confirmed receipt of the final payment. Usually, the lender will send a written notice that the loan has been paid in full. The lender must send a request for reconveyance to the trustee to start the process.

Step 2 – Identify the Parties Involved

List the full names, entity types (individual or company), and mailing addresses of each party, including:

- Trustee

- Borrower

- Lender

Step 3 – Add Recitals

You must include a short reference to the original deed of trust. This connects your new reconveyance document with the original loan. This section should clearly state:

- The date it was initially signed.

- The county and state where it was recorded.

- The book and page number or instrument number.

Step 4 – Sign and Notarize the Deed

The trustee must sign the deed of reconveyance in the presence of a notary public. Some states also require witness signatures, so be sure to check your local requirements. The notary will verify the identities of all signers and confirm that they signed willingly. Use a notary acknowledgment form for confirmation.

Step 5 – Record the Deed

File the signed deed with the local county recorder’s office where the property is located. The step makes the reconveyance official and updates the public records.

When to File a Deed of Reconveyance

Make sure your Deed of Reconveyance is recorded as soon as possible to avoid legal issues later. Some states require the lender or trustee to file this document with the county recorder within a specific timeframe, usually within 30 to 60 days after you’ve paid off your mortgage. Failing to record on time can delay a clear title or affect future sales or refinancing.

What Happens If a Deed of Reconveyance Isn’t Recorded?

If your deed of reconveyance isn’t correctly recorded with the county recorder’s office, it can cause legal and financial problems, even if your mortgage is fully paid off.

- Your title may still show a lien: Without a recorded deed, public records will continue to show that the lender has a legal claim on your home. This can prevent you from selling or refinancing because the title will not be considered clear.

- You may have trouble proving full ownership: Even if you have paid off your loan, missing paperwork can create confusion. While you might have documents showing the loan is paid off, those won’t be enough during real estate transactions. The payoff must be noted in the county land records.

- The lender could face penalties: In many states, the trustee or lender is required to record the deed of reconveyance within a specific timeframe after the mortgage is paid off (typically 21 to 60 days). If they fail to meet this deadline, they may face fines or legal action depending on the state law.

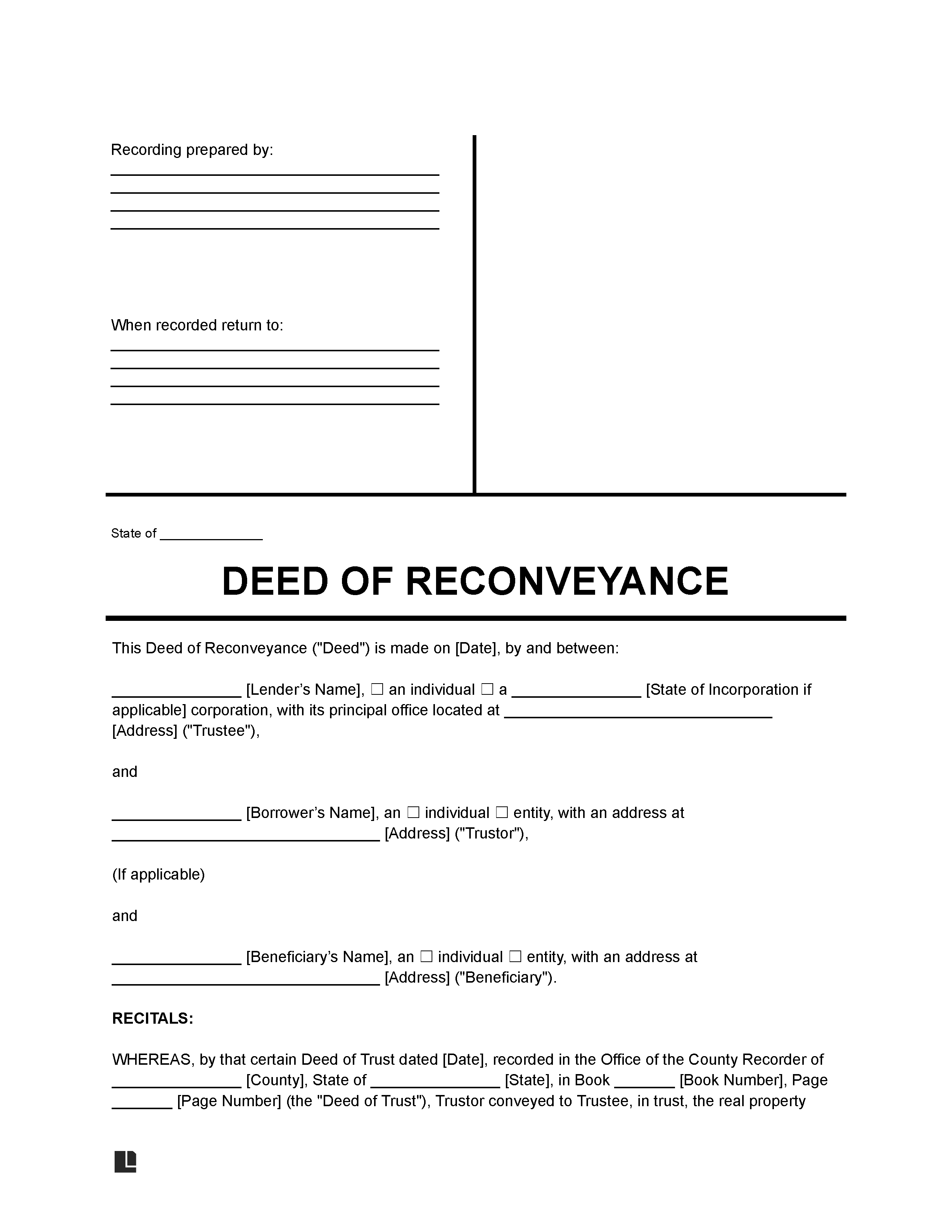

Sample Deed of Reconveyance

View our sample Deed of Reconveyance template to see how to properly complete each section with the correct loan and property details. Use our step-by-step questionnaire to fill out the form, then download your Deed of Reconveyance as a PDF or Word file.