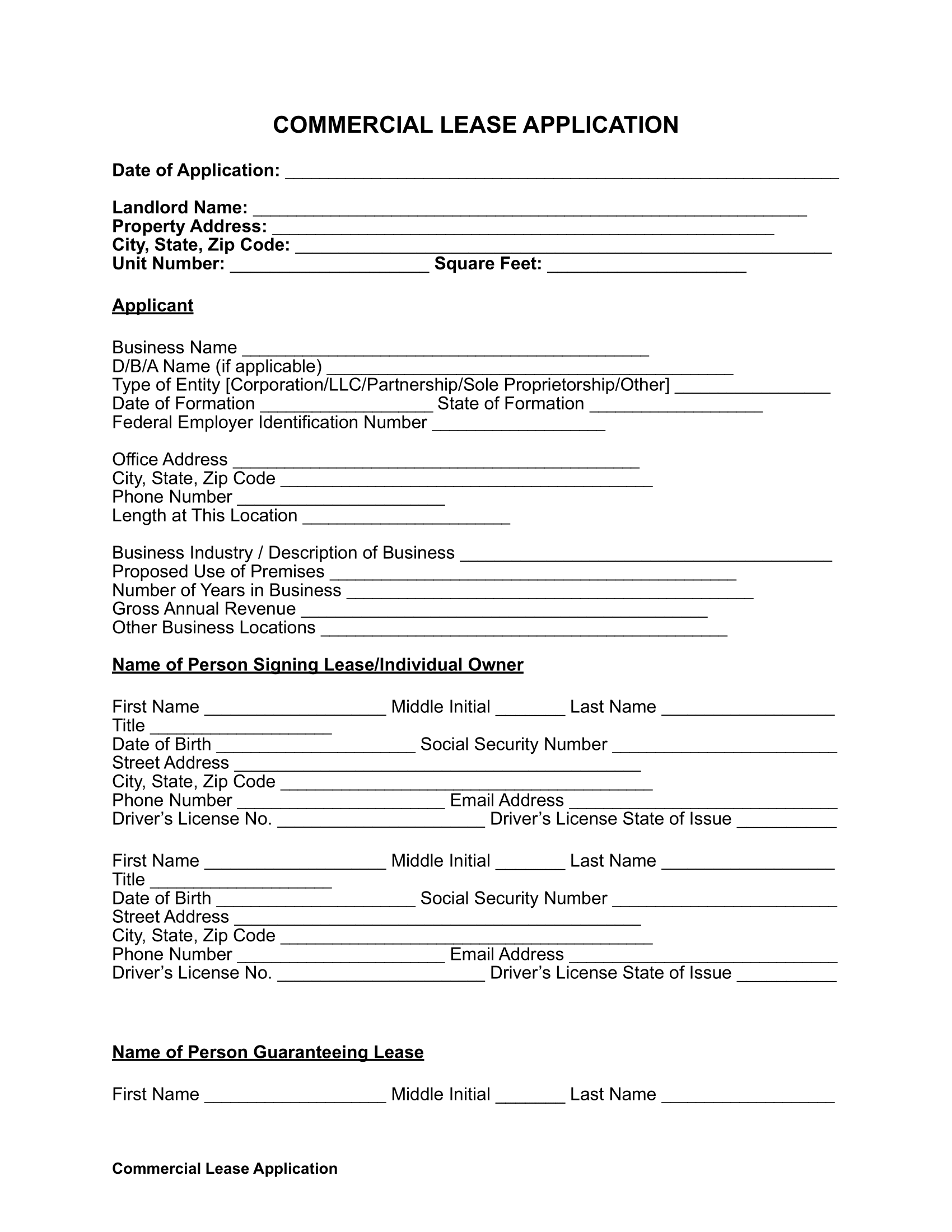

A commercial lease application is a document a landlord or property manager uses to screen applicants for a commercial rental property. It’s the first step in leasing a commercial property, and it can lead to a commercial lease agreement where the business tenant uses the property for income-generating activities under the landlord’s specific terms.

Commercial vs. Residential Lease Applications

Commercial rental applications focus on businesses’ suitability to rent a commercial space. In contrast, residential lease applications focus on individuals’ aptness to rent an apartment or private home.

What Is a Commercial Lease Application?

A commercial lease application helps the landlord or property manager screen businesses to evaluate and decide on a tenant for a commercial space. Applications for commercial leases also give insight into a business’s financials and rental history, which helps the landlord choose a suitable tenant and minimize risk.

A landlord usually asks a business entity’s representative or owner to fill out a commercial rental application form to lease commercial space before signing a commercial lease agreement.

Who Uses a Commercial Lease Application?

Commercial landlords use commercial lease applications to rent out space for business purposes. These landlords can be companies or individuals owning commercial properties such as the following:

- Manufacturing facilities

- Restaurants

- Warehouses

- Retail spaces

- Office buildings

- Strip malls

- Shopping malls

- High-rise buildings

- Factories

The application is an effective screening tool that helps commercial landlords choose qualified tenants with a good business track record, are financially stable, and will use the property responsibly.

What Can a Landlord Ask on a Commercial Lease Application?

As a landlord or property manager, there are limitations to what you can ask while screening commercial tenants. Reduce potential legal issues by limiting your inquiries to the following:

- The business name: Learn under what name the potential tenant conducts business. Use this information to search for customer reviews and complaints and determine whether the business has a good reputation.

- The business structure: Ask whether the tenant’s business is structured like a limited liability company (LLC), corporation, partnership, or sole proprietorship to determine who will pay rent and how the business will operate daily.

- The intended use of the space: Request details about the type of business the tenant intends to operate. Learn whether the owners will use the space in a manner consistent with legal and regulatory requirements. These details also let you determine if the space suits the business’s intended use.

- Previous rental information: Ask for details about the tenant’s prior rental history pertaining to commercial real estate, including their previous landlords’ contact information. References can help determine if your potential commercial tenant will be reliable and respectful.

- Business owner information: Request the business owner’s name and identifying information to conduct credit and background checks. This way, you’ll know more about who will be renting your space and whether they have any financial issues that could prevent them from meeting the lease terms.

- Business partners’ names: Obtain information about any partners the business tenant will work with during their lease term.

- Business banking information: Ask for the business’s banking details, including bank statements, tax returns, profit and loss statements, and a business plan. As the landlord, you have a right to investigate whether the business can meet the financial obligations of the agreement before you sign the lease.

- Credit references: Credit reports and references from banks, lending agencies, and businesses associated with your potential tenant can provide critical insights into the potential tenant’s financial stability and reliability.

- Authorization to perform a credit or background check: The Fair Credit Reporting Act (FCRA) requires you to obtain permission before performing a credit or background check on any applicant. To meet authorization requirements, use a background and credit check authorization form to request the applicant’s information. The form should include a signed and dated statement authorizing you to conduct the credit check.

How to Screen a Commercial Rental Applicant

Step 1 – Acquire the Rental Application

Acquire the completed rental application from the potential tenant. Ensure they provide all the requested details. Review their information to determine if they’d be a suitable candidate depending on their needs and the space you have available.

Proceed with the subsequent steps to verify the information the tenant provides.

Step 2 – Verify the Business with the State

All 50 states have a specific office, like a Secretary of State, with reputable businesses on file. Ensure your applicant’s business is in good standing with the state.

The resources below help verify a business’s status with its respective Secretary of State or equivalent office:

| Alabama | Alaska | Arizona |

| Arkansas | California | Colorado |

| Connecticut | Delaware | District of Columbia |

| Florida | Georgia | Hawaii |

| Idaho | Illinois | Indiana |

Step 3 – Look Up the Business’s Credit Score

Look up the business’s credit score, which is a risk and creditworthiness score a third-party company assigns to a business owner or principal.

Dun & Bradstreet is one of the most popular providers of business credit scores. The company created its own proprietary scoring system known as PAYDEX, which measures a business based on its past performance. The scoring system is as follows:

- 0-49. High risk of late payment (an average of 30 to 120 days beyond terms)

- 50-79. Medium risk of late payment (average of 30 or fewer days beyond terms)

- 80-100. Low risk of late payment (average of prompt to 30 days within terms)

Dun & Bradstreet is relatively affordable, as a report costs $61.99. Other providers of business credit scores include the following companies:

- Experian: $49.95 per report

- Equifax: $99.95 per report

- Nav.com: $39.95 per report

- Creditsafe: One free report

Step 4 – Conduct a Personal Credit Check

While it’s important to run a business credit check to better understand the company’s financials, you can also benefit from conducting a personal credit check of the business owner. Personal credit checks produce scores between 300 and 850. Ideally, you should consider tenants with a personal credit score of at least 700.

Obtain a personal credit score from one of the three major credit reporting bureaus: Transunion, Experian, or Equifax.

Please ensure you have the business owner’s permission and follow all procedures and regulations of the Fair Credit Reporting Act and the credit reporting agencies.

Step 5 – Contact References

As the landlord, you can verify the information a potential tenant provides by contacting the references they give. Consider contacting them by phone instead of via email for added legitimacy.

If you have to contact a bank to verify financial information, the bank may request the applicant’s consent before it provides sensitive financial information.

Step 6 – Obtain a Personal Guarantee

Confirm that the tenant will pay the lease regardless of whether their business succeeds by requiring them to provide a personal guarantee. This statement affirms that the tenant will keep paying the lease until the agreed-upon termination date, even if the business’s operations can no longer persist.

Step 7 – Decide on the Tenant

Use the information from the previous steps to select a final tenant who is likely to pay rent on time for the entire lease and adhere to the other lease terms. Notify the tenant with a rental application approval letter. Then, you can start negotiating a lease with your tenant. Have the tenant complete a real estate non-disclosure agreement if you share sensitive information about the property with them.

Send a rejection letter with the reasons for the denial to all applicants you decline. You must also tell the tenant if you take an adverse action due to the applicant’s credit check [1] . Examples of adverse action include declining the applicant, requesting a higher deposit amount, raising the rent amount, and adding a deposit that isn’t required for other applicants.

Warning Signs

Be aware of the following warning signs when reviewing a commercial lease application:

- Unwillingness to sign a long-term lease: A tenant unwilling to sign a long-term (at least five years) lease may anticipate fast business growth and require relocation, expect an unstable financial future for the company, or foresee the space unsuitable for their needs.

- No financial backing: If a tenant doesn’t provide guarantors, you should be wary of their ability to meet their lease payments. There may be exceptions if the tenant is exceptionally wealthy, but you should ensure the tenant has a guarantor in most cases. You can also seek proof of the tenant’s personal finances for further confirmation.

- Low credit score: A credit score lower than 600 should raise some doubts in your mind that a tenant will be able to pay. It may signal they have a history of debt, failure to pay their bills on time, or bankruptcy.

Commercial Lease Application Sample

Download a commercial lease application form in PDF or Word Format below:

Frequently Asked Questions

What can I not ask on a business lease application form?

According to 42 US Code § 3604, landlords cannot ask any questions on a business lease application that discriminate based on the following:

- Race

- National origin

- Color

- Age

- Sex or gender

- Sexual orientation

- Familial status

- Military or veteran status

- Disability

- Religion

Furthermore, property owners must adhere to applicable state and federal laws regarding applications and credit reports.

What is the usable square footage?

The usable square footage is where a business can conduct operations, accommodate customers and employees, and set up equipment. It’s the functional and practical space available for specific pursuits. It excludes space that’s unusable due to building features or architectural limitations.

Can I reject a commercial lease application?

Yes. You may reject a commercial lease application if you conclude the tenant doesn’t meet your leasing criteria or if you have concerns about their compatibility with existing tenants or their ability to fulfill their leasing obligations.

Should I charge a fee to process a lease application?

While the choice is up to you, it’s wise to collect a non-refundable application fee to cover the cost and time of processing this application. Disclose the fee to applicants upfront and ensure it’s reasonable compared to commercial lease application fees in your area.

What should I do after approving a commercial lease application?

Once you approve a commercial lease application, you can proceed with the next steps in leasing a commercial space. First, draft and execute the lease agreement using a commercial lease application glossary to guide the writing process.

Collect any required security deposit and advance rent as the agreement specifies. Then, conduct a walkthrough inspection of the facility to note its condition, hand out keys and access information, and communicate important contacts if the tenant encounters issues.

What are the types of commercial leases?

Landlords can write different types of leases to meet their rental needs:

- Full-service lease: A full-service lease includes all anticipated costs, including utilities, maintenance fees, repairs, and taxes. While the tenant will incur a higher monthly cost with this type of lease, they can avoid surprise costs later in their lease.

- Net lease: A net lease has the tenant cover some costs associated with a lease. For example, they may pay for costs relating to maintenance, insurance, and property taxes plus the base rent. The amount they pay each month may fluctuate depending on the expenses that arise.

- Modified-gross lease: A modified-gross lease combines a full-service and a net lease. The tenant may pay some expenses while the landlord is responsible for others.